Wisconsin Paycheck Tax Guide: Standard Deduction Phaseout and Take-Home Pay (2026)

Wisconsin paycheck tax: 3.5% to 7.65% brackets with a sliding standard deduction that phases out by $106K income. Take-home pay at $50K to $100K.

Wisconsin's income tax brackets look similar to other Midwestern states on paper: four tiers, rates from 3.5% to 7.65%, and a standard deduction. What most guides and competitors leave out is that the standard deduction is not fixed. Wisconsin's standard deduction starts at $12,760 for single filers and phases down as income rises, reaching $0 somewhere around $106,000. That phaseout functions as a hidden rate increase during the middle of the income range, pushing the effective marginal rate above the stated bracket rate for workers in that band.

The Wisconsin Paycheck Calculator applies the correct deduction for your income level automatically. This guide explains how the phaseout works, what it costs in real dollars, and how Wisconsin's overall tax burden compares to Minnesota and Illinois.

Wisconsin Income Tax Brackets for 2025

Wisconsin taxes income on four brackets for single filers. The rates and thresholds for 2025:

| Taxable Income | Rate |

|---|---|

| $0 to $14,320 | 3.50% |

| $14,321 to $28,640 | 4.40% |

| $28,641 to $315,310 | 5.30% |

| Over $315,310 | 7.65% |

For married filing jointly, the thresholds are approximately double:

| Taxable Income | Rate |

|---|---|

| $0 to $19,090 | 3.50% |

| $19,091 to $38,190 | 4.40% |

| $38,191 to $420,420 | 5.30% |

| Over $420,420 | 7.65% |

The 7.65% top bracket is notably high, but it only kicks in above $315,310 for single filers. For most Wisconsin employees earning between $30,000 and $150,000, the relevant rate is 5.30%.

Wisconsin does not have a local income tax. No city, county, or municipality in the state adds a local withholding line. Every Wisconsin employee pays the same state rate regardless of whether they live in Milwaukee, Madison, Green Bay, or a rural town.

What Wisconsin does not tax:

Social Security income is exempt from Wisconsin state income tax. Federal and state pension income receives a partial exclusion. Military retirement income and certain railroad retirement benefits are also excluded. Most W-2 workers below age 62 are unaffected by these exemptions.

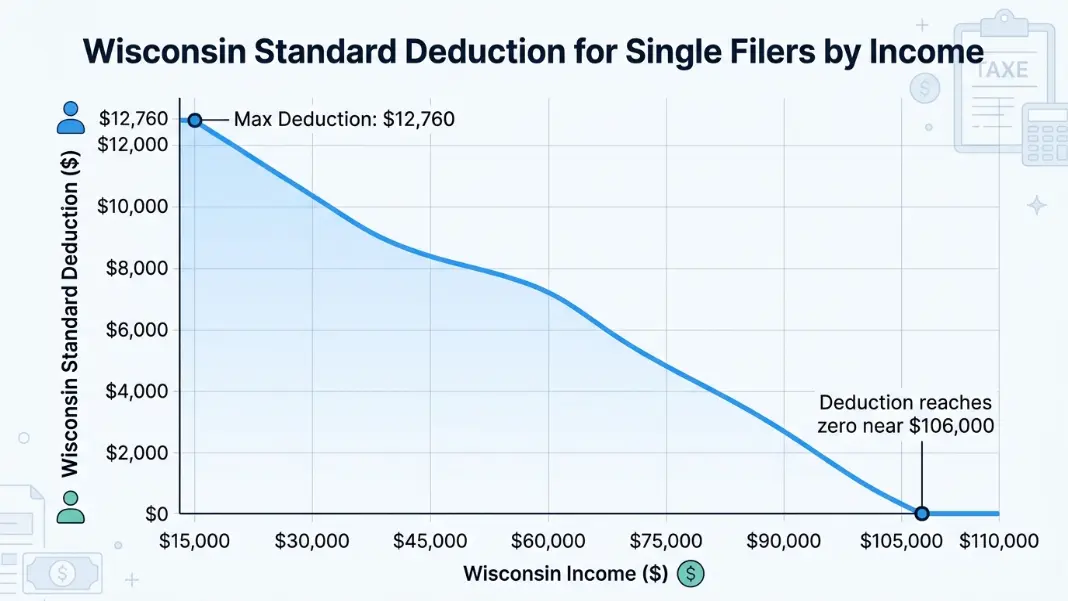

The Sliding Standard Deduction: Wisconsin's Hidden Effective Rate Increase

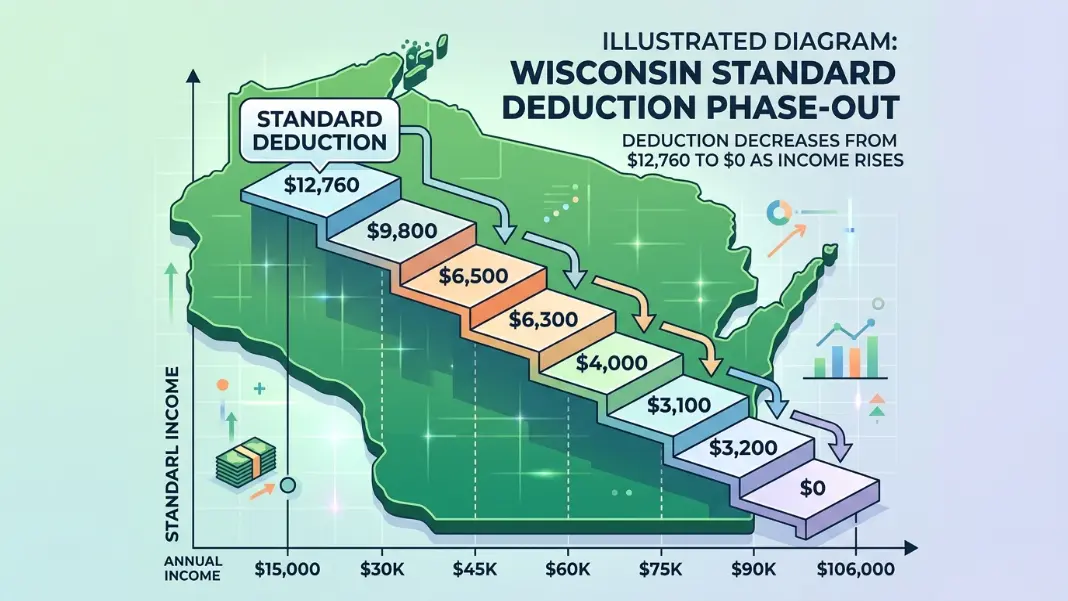

This is the part most guides miss. Wisconsin's standard deduction for single filers has a maximum of $12,760, but that full amount only applies to lower incomes. As income rises, the deduction shrinks and eventually disappears.

The deduction phases out beginning around $15,840 of adjusted gross income for single filers. For every dollar earned above that threshold, the deduction reduces by roughly 12.5 cents, until it reaches $0 at approximately $106,160.

Standard deduction at different income levels (single filer, approximate):

| Gross Income | Approx. Standard Deduction | Taxable Income |

|---|---|---|

| $30,000 | $11,150 | $18,850 |

| $50,000 | $8,700 | $41,300 |

| $75,000 | $5,600 | $69,400 |

| $90,000 | $3,700 | $86,300 |

| $106,000 | $0 | $106,000 |

| $130,000 | $0 | $130,000 |

The deduction phaseout creates a situation where an employee earning $50,000 and one earning $51,000 are not just one bracket step apart. The higher earner also loses a portion of their deduction, which increases their taxable income by more than just the $1,000 salary difference.

Effective marginal rate during the phaseout (5.30% bracket):

When the standard deduction is phasing out at 12.5 cents per additional dollar earned, each extra dollar of gross income produces more than one dollar of taxable income. An additional $1.00 of gross income generates $1.125 of taxable income (the $1.00 itself plus $0.125 of lost deduction). At the 5.30% rate:

Effective marginal rate during phaseout = 5.30% x 1.125 = 5.96%

A Wisconsin single filer in the $30,000 to $106,000 income range faces an effective marginal rate about 0.66 percentage points higher than the stated 5.30% bracket rate during the phaseout period. That is not huge, but it means the deduction phases out in a way that affects every worker in that band, which covers the large majority of Wisconsin's labor force.

Married filing jointly phaseout:

The MFJ standard deduction starts at $23,620 and phases out beginning around $23,510. The phaseout rate is also approximately 12.5 cents per dollar, reaching $0 at roughly $155,350. The same effective rate calculation applies.

Federal Withholding on a Wisconsin Paycheck

Federal taxes represent the largest share of withholding for most Wisconsin employees. The federal calculation uses the same W-4 elections and graduated brackets as every other state.

2025 federal income tax brackets for single filers:

| Taxable Income | Rate |

|---|---|

| Up to $11,925 | 10% |

| $11,926 to $48,475 | 12% |

| $48,476 to $103,350 | 22% |

| $103,351 to $197,300 | 24% |

| Over $197,300 | 32%+ |

FICA withholding applies to all wages:

- Social Security: 6.2% on wages up to $176,100 (2025 wage base)

- Medicare: 1.45% on all wages, plus 0.9% on wages over $200,000

Federal vs Wisconsin breakdown at $75,000 (single):

Federal income tax (approximate): $10,294

Social Security ($75,000 x 6.2%): $4,650

Medicare ($75,000 x 1.45%): $1,088

Total federal: $16,032

Wisconsin state income tax (at $75,000, deduction ~$5,600):

Taxable income: $69,400

Tax on $69,400 using brackets: approximately $2,952

Effective Wisconsin rate on $75,000: 3.94%

Total all withholding: $18,984

Take-home: $56,016

The W-4 controls federal withholding but has no effect on Wisconsin state withholding. Wisconsin uses its own withholding tables for state income tax, applied automatically based on filing status. Employees who had a large federal refund or balance due should update their W-4. Wisconsin state withholding adjustments require updating with the employer directly.

The Massachusetts Paycheck Tax Guide covers a comparable flat-rate state where the deduction structure works very differently: Massachusetts applies a fixed personal exemption rather than a phasing deduction, which means the effective rate does not change with income the way Wisconsin's does.

Wisconsin Take-Home Pay at $50K, $75K, and $100K

Three scenarios for a single Wisconsin filer, no pre-tax deductions, standard W-4 settings, biweekly payroll:

| Gross Salary | Federal Tax | FICA | WI State Tax | Take-Home | Effective Total Rate |

|---|---|---|---|---|---|

| $50,000 | $5,294 | $3,825 | $1,734 | $39,147 | 21.7% |

| $75,000 | $10,294 | $5,738 | $2,952 | $56,016 | 25.3% |

| $100,000 | $16,244 | $7,650 | $4,409 | $71,697 | 28.3% |

Wisconsin state tax calculations account for the sliding deduction at each income level: the $50K filer retains most of the $12,760 deduction, while the $100K filer has lost most of it, which is why the state tax column does not increase linearly with income.

Effect of pre-tax 401k contributions:

A $6,000 annual 401k contribution at the $75,000 income level:

- Reduces federal taxable income, saving approximately $1,320 (22% bracket)

- Reduces Wisconsin taxable income, saving approximately $318 (5.30% effective rate)

- Also reduces the deduction phaseout impact slightly, since lower AGI means a larger standard deduction is preserved

- Total annual savings: approximately $1,700

The deduction phaseout interaction is a legitimate reason to maximize pre-tax contributions in Wisconsin: each dollar contributed not only saves at the marginal rate but also slows the deduction reduction, creating a slight compounding effect.

Wisconsin vs Minnesota and Illinois

Wisconsin sits between two states with notably different tax structures.

| State | Structure | Top Rate | Effective Rate at $75K | Local Tax |

|---|---|---|---|---|

| Wisconsin | Progressive, 4 brackets | 7.65% | ~3.94% | None |

| Minnesota | Progressive, 4 brackets | 9.85% | ~5.5% | None |

| Illinois | Flat rate | 4.95% | 4.95% | None |

| Iowa | Progressive, reduced | 5.70% top (2025) | ~4.2% | None |

| Michigan | Flat rate | 4.25% | 4.25% | Some city taxes |

Minnesota's top rate of 9.85% is among the highest in the country, but the threshold is high: single filers do not hit the top bracket until income exceeds about $183,340. Wisconsin's 7.65% top rate also applies only at very high incomes. For a worker at $75,000, Wisconsin's effective rate of approximately 3.94% is lower than Illinois's flat 4.95% and well below Minnesota's effective rate at the same income.

The comparison with Illinois is the one most Wisconsin workers encounter. Illinois has no standard deduction at the state level (a flat rate on all income), while Wisconsin's deduction system means lower effective rates for workers below the phaseout range. Above $106,000 where Wisconsin's deduction has fully phased out, Wisconsin's 5.30% effective rate exceeds Illinois's 4.95% flat rate. That crossover point is at roughly $100,000 to $110,000 in gross income for single filers.

The Minnesota Paycheck Tax Guide covers Minnesota's full bracket structure and explains why the 9.85% top rate affects far fewer workers than the headline suggests. For more on why Illinois's flat rate is constitutionally locked and how it compares to states with sliding deductions, the Illinois Paycheck Tax Guide covers that in full.

For Wisconsin workers contributing to a 529 college savings plan, contributions to the Wisconsin EdVest plan are deductible from Wisconsin income up to $3,860 per beneficiary per year (2025 limit). That deduction reduces Wisconsin taxable income in a state where the marginal rate during the phaseout range runs approximately 5.96% effective. The Roth IRA Contribution Calculator is the complementary tool for workers who have maximized pre-tax options and are weighing Roth contributions for 2026.

Wisconsin state income tax uses four brackets: 3.5% up to $14,320, 4.4% up to $28,640, 5.3% up to $315,310, and 7.65% above that for single filers. A standard deduction of up to $12,760 reduces taxable income, but phases out as income increases, reaching $0 at around $106,000. At a $75,000 salary, Wisconsin state income tax is approximately $2,952 after applying the partial deduction, an effective rate of about 3.94% on gross income.

Wisconsin's standard deduction for single filers starts at $12,760 but decreases by roughly 12.5 cents for every dollar of income above approximately $15,840. By around $106,160, the deduction has fully phased out to $0. Married filers have a higher maximum deduction of $23,620 with a different phaseout range. The phaseout creates an effective marginal rate slightly above the stated 5.3% bracket rate during the phase-out band, since each additional dollar earned triggers both the bracket rate and a small loss of deduction.

No. Wisconsin does not allow cities, counties, or municipalities to levy local income taxes. Every Wisconsin employee pays only the state income tax rate regardless of whether they work in Milwaukee, Madison, Green Bay, Kenosha, or anywhere else in the state. This is a significant structural difference from neighboring states like Michigan, where Detroit adds a 2.4% city income tax, or Illinois, where Chicago does not add a city tax but some other surrounding jurisdictions in neighboring states do.

Wisconsin's top rate of 7.65% is lower than Minnesota's 9.85%, but both apply only at high incomes. At $75,000 for a single filer, Wisconsin's effective state rate is approximately 3.94% after the standard deduction, while Minnesota's effective rate is closer to 5.5%. Wisconsin has a lower effective rate than Minnesota at every income level below about $315,000. For workers near the Wisconsin-Minnesota border choosing where to live, Wisconsin's lower effective rate at middle incomes represents a real take-home pay difference.

Social Security benefits are fully exempt from Wisconsin state income tax. Federal and state pension income receives exclusions that vary by age and amount. Military retirement pay and railroad retirement benefits are also exempt or partially excluded. Investment income from capital gains in Wisconsin is taxed at the ordinary income rate with no separate capital gains rate. Unlike some states, Wisconsin does not provide a general exemption for retirement income from private pensions, though the pension exclusion for federal retirees partially fills that gap.

Not particularly. At $75,000 for a single filer, Wisconsin's effective state income tax rate is approximately 3.94%, which is lower than Illinois (4.95% flat), Minnesota (~5.5%), or Iowa (~4.2%). Wisconsin's progressive structure combined with the standard deduction keeps effective rates below surrounding states at middle incomes. The state becomes comparatively expensive only above the $106,000 income level where the standard deduction has fully phased out and the 5.3% rate applies to the full taxable income, at which point it exceeds Illinois's flat rate.

Written by

Hassaan Rasheed

Web Developer & Content Researcher

Hassaan builds calculators and writes research-backed guides on finance, math, payroll, and construction topics. Every number in his articles is sourced from official data and worked through by hand.

View LinkedIn Profile