Minnesota Paycheck Tax Guide: Brackets, No Local Tax, and Take-Home Pay (2026)

Minnesota income tax: 4 brackets from 5.35% to 9.85%, no local tax anywhere in the state. Take-home pay at $50K, $75K, and $100K for 2025.

Minnesota's 9.85% top income tax rate is the highest in the Midwest, and it gets used as a shorthand for the state being expensive. For a single filer earning $75,000, that top rate is completely irrelevant. The 9.85% bracket does not begin until $183,340 in taxable income. At $75,000, the effective Minnesota state rate is under 5%, which puts it in the same range as a flat-rate state like Massachusetts.

The Minnesota Paycheck Calculator runs the full calculation with your salary, filing status, and any pre-tax deductions. This guide walks through what each bracket actually costs at real income levels, what Minneapolis and St. Paul do not add to your bill, and how Minnesota compares to the states most residents actually compare against.

Minnesota's bracket structure is progressive in the genuine sense: only income above each threshold gets taxed at the higher rate. That distinction matters a lot at $75,000, where most of your income is sitting in the 5.35% and 6.80% brackets, not the ones that get the headlines.

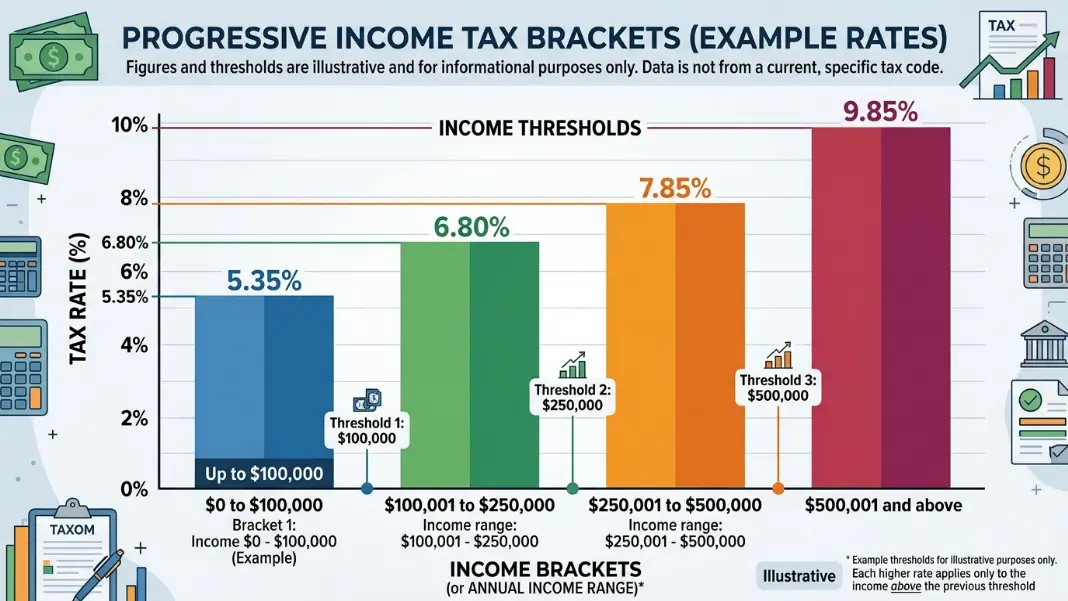

Minnesota Income Tax Brackets for 2025: Where the 9.85% Rate Actually Starts

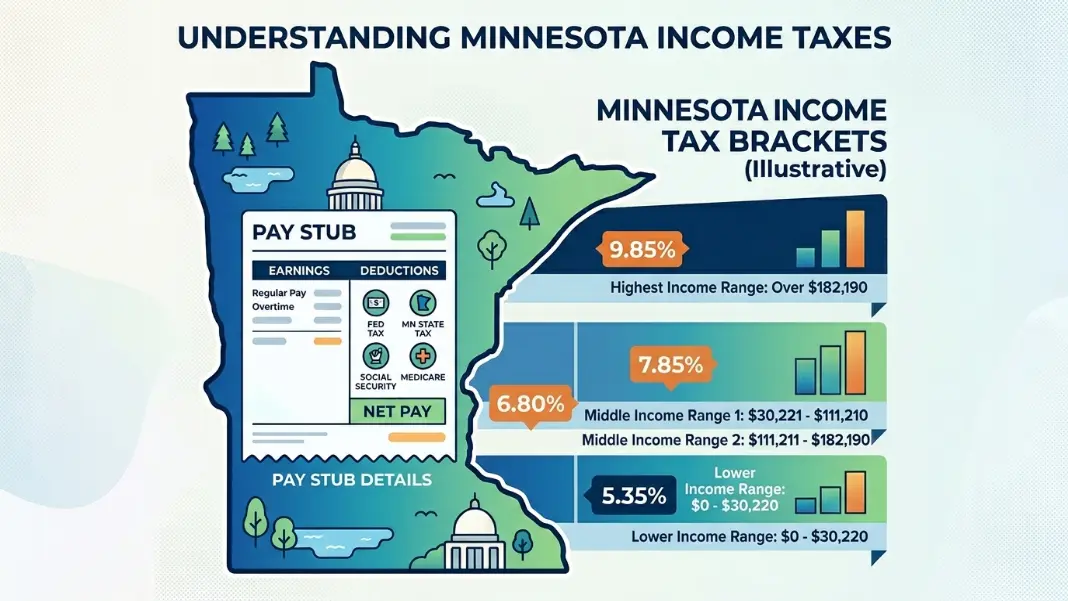

Minnesota taxes income on four brackets for single filers in 2025. The rates and thresholds:

| Taxable Income | Rate |

|---|---|

| Up to $31,690 | 5.35% |

| $31,691 to $104,090 | 6.80% |

| $104,091 to $183,340 | 7.85% |

| Over $183,340 | 9.85% |

For married filing jointly, the thresholds roughly double:

| Taxable Income | Rate |

|---|---|

| Up to $46,330 | 5.35% |

| $46,331 to $184,040 | 6.80% |

| $184,041 to $304,970 | 7.85% |

| Over $304,970 | 9.85% |

Minnesota also applies a standard deduction before calculating taxable income: $14,575 for single filers and $29,150 for married filing jointly in 2025. This is close to the federal standard deduction and works the same way: you subtract it from gross income before applying the brackets.

What this means at $75,000:

A single filer earning $75,000 gross subtracts the $14,575 standard deduction, leaving $60,425 in taxable income. That taxable income falls entirely within the first two brackets:

First $31,690 taxed at 5.35% = $1,695

Remaining $28,735 taxed at 6.80% = $1,954

Total MN state tax = $3,649

Effective rate on $75,000 gross = 4.87%

The 7.85% bracket does not touch this income at all. A single filer hits the 7.85% rate only when taxable income exceeds $104,090, which means gross income above roughly $118,665 after the standard deduction.

The 9.85% rate applies above $183,340 in taxable income, or roughly $197,915 in gross income. Most Minnesotans never interact with either the third or fourth bracket. The top rate applies to a small share of earners.

No Local Income Tax: Why Minneapolis and St. Paul Don't Add to Your Bill

Minnesota prohibits cities and counties from levying their own income taxes. Minneapolis, St. Paul, Duluth, Rochester: none of them add a local withholding line to your paycheck. Every Minnesota W-2 employee in the state pays exactly the same state tax rate regardless of where they work.

This is not trivially obvious. Neighboring states do not work this way.

Ohio allows cities to levy local income taxes, and most large Ohio cities do. Columbus, Cleveland, Cincinnati, and Akron all add 2% to 2.5% on top of Ohio state income tax. Michigan allows city income taxes; Detroit charges 2.4% for residents and 1.2% for nonresidents working in the city. If you have ever received a paycheck from an employer in one of those states, the local tax line on your stub is a real number.

In Minnesota, that line does not exist. A worker earning $75,000 in downtown Minneapolis pays the same state income tax as a worker at the same salary in a rural county. This is worth understanding clearly when comparing job offers across state lines, especially if you are weighing a Minnesota offer against one in an Ohio or Michigan metro where a city tax would apply.

Social Security and Retirement Income: What Minnesota Now Exempts

Minnesota passed a meaningful Social Security exemption that took effect in 2023. For single filers with adjusted gross income under $75,000, Social Security benefits are fully exempt from Minnesota income tax. For married filing jointly filers with AGI under $100,000, the same full exemption applies.

Above those thresholds, a partial exemption applies. The exemption phases out as income rises, and high earners with significant other income will have some portion of their Social Security benefits included in Minnesota taxable income.

For most retirees receiving Social Security, this exemption eliminates the state tax on those benefits entirely. A retired single filer with $40,000 in Social Security income and $25,000 in other retirement income (total AGI well under $75,000) pays no Minnesota income tax on the Social Security portion.

This was not always the case. Minnesota was one of a small number of states that continued to tax Social Security after the federal government began exempting lower-income recipients, and the 2023 change addressed a complaint that had been raised by retirees in the state for years.

Minnesota's treatment of retirement income beyond Social Security is less generous. Pension income from private employers, 401k withdrawals, and traditional IRA distributions are taxed as ordinary income at the standard Minnesota brackets. There is no general pension exclusion for most retirees. The Social Security exemption is meaningful, but it does not extend to all retirement income.

For workers building toward retirement and weighing pre-tax versus Roth contributions, the Roth IRA Contribution Calculator shows your maximum allowable contribution based on modified AGI, including the phase-out ranges for 2026.

Federal Withholding on a Minnesota Paycheck

Federal income tax and FICA represent the majority of withholding for most Minnesota employees. The federal calculation uses the same W-4 elections and graduated brackets as every other state.

2025 federal income tax brackets for single filers:

| Taxable Income | Rate |

|---|---|

| Up to $11,925 | 10% |

| $11,926 to $48,475 | 12% |

| $48,476 to $103,350 | 22% |

| $103,351 to $197,300 | 24% |

| Over $197,300 | 32%+ |

FICA withholding applies to all wages:

- Social Security: 6.2% on wages up to $176,100 (2025 wage base)

- Medicare: 1.45% on all wages, plus 0.9% on wages over $200,000

Federal vs Minnesota at $75,000 (single):

Federal income tax (approximate): $10,294

Social Security ($75,000 x 6.2%): $4,650

Medicare ($75,000 x 1.45%): $1,088

Total FICA: $5,738

Minnesota state income tax: $3,649

Total all withholding: $19,681

Take-home: $55,319

The federal withholding at $75,000 is nearly three times the Minnesota state withholding. That ratio is worth keeping in mind when people describe Minnesota as a high-tax state: the largest line on the stub is federal, not state, and federal withholding is identical regardless of which state you work in.

Pre-tax 401k contributions, health insurance premiums, and HSA contributions all reduce both federal and Minnesota taxable income. A worker contributing $6,000 per year to a 401k at the $75,000 income level saves approximately $1,320 in federal taxes (22% bracket) plus approximately $408 in Minnesota taxes (6.80% marginal rate), for a combined $1,728 in annual savings.

Minnesota Take-Home Pay at $50K, $75K, and $100K

Three scenarios for a single Minnesota filer, no pre-tax deductions, standard W-4 settings, biweekly payroll. Minnesota state tax is calculated after the $14,575 standard deduction.

| Gross Salary | Federal Tax | FICA | MN State Tax | Take-Home | Effective Total Rate |

|---|---|---|---|---|---|

| $50,000 | $5,294 | $3,825 | $1,949 | $38,932 | 22.1% |

| $75,000 | $10,294 | $5,738 | $3,649 | $55,319 | 26.2% |

| $100,000 | $16,244 | $7,650 | $5,349 | $70,757 | 29.2% |

Minnesota state tax detail at each income level:

At $50,000: taxable income after standard deduction is $35,425. First $31,690 taxed at 5.35% = $1,695. Remaining $3,735 taxed at 6.80% = $254. Total: $1,949.

At $75,000: taxable income is $60,425. First $31,690 at 5.35% = $1,695. Remaining $28,735 at 6.80% = $1,954. Total: $3,649.

At $100,000: taxable income is $85,425. First $31,690 at 5.35% = $1,695. Remaining $53,735 at 6.80% = $3,654. Total: $5,349. Note: even at $100,000 gross, the 7.85% bracket is not reached, because taxable income of $85,425 is still below the $104,090 threshold for the third bracket.

The effective Minnesota rate rises from 3.9% at $50,000 to 5.35% at $100,000, reflecting the progressive bracket structure. The jump in total take-home reduction between $75,000 and $100,000 is driven more by the federal withholding increase (from 22% to 24% bracket exposure) than by the Minnesota state rate change.

For workers considering pre-tax contributions, the four-state comparison at the NE, MN, UT, MT Paycheck Guide shows how Minnesota's higher marginal rates make pre-tax 401k contributions more valuable in dollar terms than in lower-rate states: each dollar contributed saves more in state tax when the marginal rate is 6.80% versus Utah's flat 4.55%.

Minnesota vs Wisconsin, Iowa, and North Dakota

Minnesota sits at the high end of the Midwest in terms of state income tax rates, but the comparison looks different at different income levels.

| State | Structure | Effective Rate at $75K | Local Tax |

|---|---|---|---|

| Minnesota | Progressive, 4 brackets | ~4.87% | None |

| Wisconsin | Progressive, sliding deduction | ~3.94% | None |

| Iowa | Progressive, reduced (5.70% top, 2025) | ~4.2% | None |

| North Dakota | Progressive, low rates | ~1.4% | None |

Wisconsin is the most direct comparison for Minnesota, since both use four-bracket progressive systems and neither has local income taxes. At $75,000 for a single filer, Wisconsin's effective state rate of approximately 3.94% is about one percentage point lower than Minnesota's 4.87%. That difference is roughly $693 per year at $75,000.

Wisconsin's advantage at middle incomes comes from its sliding standard deduction, which can be as high as $12,760 for lower earners and reduces taxable income before the brackets apply. At $75,000, Wisconsin's deduction has partially phased out, but it still reduces taxable income more than Minnesota's fixed $14,575 deduction might at certain incomes. The Wisconsin Paycheck Calculator Guide covers the deduction phaseout in detail for workers comparing the two states.

Iowa is reducing its tax burden systematically. The 2025 top rate of 5.70% continues a multi-year phase-down, and Iowa is on a trajectory toward a flat rate below 4% within a few years under current law. At $75,000 today, Iowa's effective rate of roughly 4.2% sits between Wisconsin and Minnesota.

North Dakota is the outlier. Its income tax rates are the lowest in the Midwest by a wide margin: the top rate is 2.50% for single filers, and the effective rate at $75,000 is roughly 1.4%. The gap between North Dakota and Minnesota is substantial. A worker at $75,000 pays roughly $5,338 less in state taxes in North Dakota than in Minnesota each year. For workers near the border, this is a real factor, though it has to be weighed against cost of living, employer location, and other considerations that do not fit neatly into a tax rate comparison.

Minnesota has no plans to reduce its top rate or simplify its bracket structure under current legislative conditions. Workers in higher Minnesota brackets who have not reviewed their pre-tax contribution strategy are leaving meaningful savings on the table. Every dollar in a traditional 401k or HSA reduces income that would otherwise hit the 7.85% or 9.85% Minnesota brackets at higher salaries.

A single filer earning $75,000 in Minnesota owes approximately $3,649 in state income tax in 2025. After subtracting the $14,575 standard deduction, taxable income is $60,425. The first $31,690 is taxed at 5.35% ($1,695) and the remaining $28,735 is taxed at 6.80% ($1,954). The effective Minnesota rate on $75,000 gross is about 4.87%. The Minnesota Paycheck Calculator shows the exact per-paycheck withholding for your specific salary and filing status.

No. Minnesota does not permit cities or counties to levy local income taxes. Minneapolis, St. Paul, Duluth, and every other city in the state add nothing to your paycheck beyond the state withholding. This is a meaningful contrast to states like Ohio and Michigan, where cities such as Columbus, Cleveland, and Detroit charge 2% to 2.5% on top of state income tax. Every Minnesota employee at the same salary pays the same state tax regardless of where in the state they work.

The 9.85% rate applies to taxable income above $183,340 for single filers in 2025. Taxable income means gross income after subtracting the $14,575 standard deduction and any pre-tax deductions. That puts the gross income threshold for the 9.85% bracket at roughly $197,915 for a single filer with no pre-tax deductions. The 7.85% bracket below it starts at $104,091 in taxable income. For most Minnesota workers, the relevant rates are the 5.35% and 6.80% brackets in the lower two tiers.

As of 2023, Minnesota fully exempts Social Security benefits for single filers with adjusted gross income under $75,000, and for married filing jointly filers with AGI under $100,000. Above those thresholds, a partial exemption applies that phases out as income rises. Prior to 2023, Minnesota taxed Social Security benefits more broadly than most states. For retirees with modest other income, the 2023 change eliminates most or all Minnesota state tax on their Social Security benefits.

Minnesota's standard deduction for 2025 is $14,575 for single filers and $29,150 for married filing jointly. This amount reduces gross income before the state tax brackets are applied. Unlike Wisconsin's standard deduction, Minnesota's does not phase out at higher incomes; it remains the same fixed amount regardless of your salary. A single filer earning $200,000 subtracts the same $14,575 as a single filer earning $50,000.

At $75,000 for a single filer, Minnesota's effective state income tax rate is approximately 4.87% versus Wisconsin's approximately 3.94%. That gap of about $693 per year reflects Wisconsin's sliding standard deduction, which reduces taxable income significantly at middle incomes. Both states have four progressive brackets and no local income taxes. The gap narrows at lower incomes and widens at higher incomes where Minnesota's steeper upper brackets take more. Wisconsin's top rate of 7.65% is lower than Minnesota's 9.85%, but both apply only at very high income levels.

Pre-tax 401k contributions reduce both federal and Minnesota taxable income dollar for dollar. At $75,000 gross, the marginal Minnesota rate is 6.80%. A $6,000 401k contribution saves approximately $408 in Minnesota state taxes on top of roughly $1,320 in federal tax savings. At higher incomes where the 7.85% bracket applies, the Minnesota savings increase. Workers in the 9.85% bracket save $591 in Minnesota tax per $6,000 contributed. Minnesota's higher marginal rates make pre-tax retirement contributions more valuable in dollar terms than in most neighboring states.

Written by

Hassaan Rasheed

Web Developer & Content Researcher

Hassaan builds calculators and writes research-backed guides on finance, math, payroll, and construction topics. Every number in his articles is sourced from official data and worked through by hand.

View LinkedIn Profile