IRR Calculator: How to Calculate Internal Rate of Return (2026)

IRR formula, rental property worked example, MIRR correction, and when IRR produces misleading results.

11 min readRead →

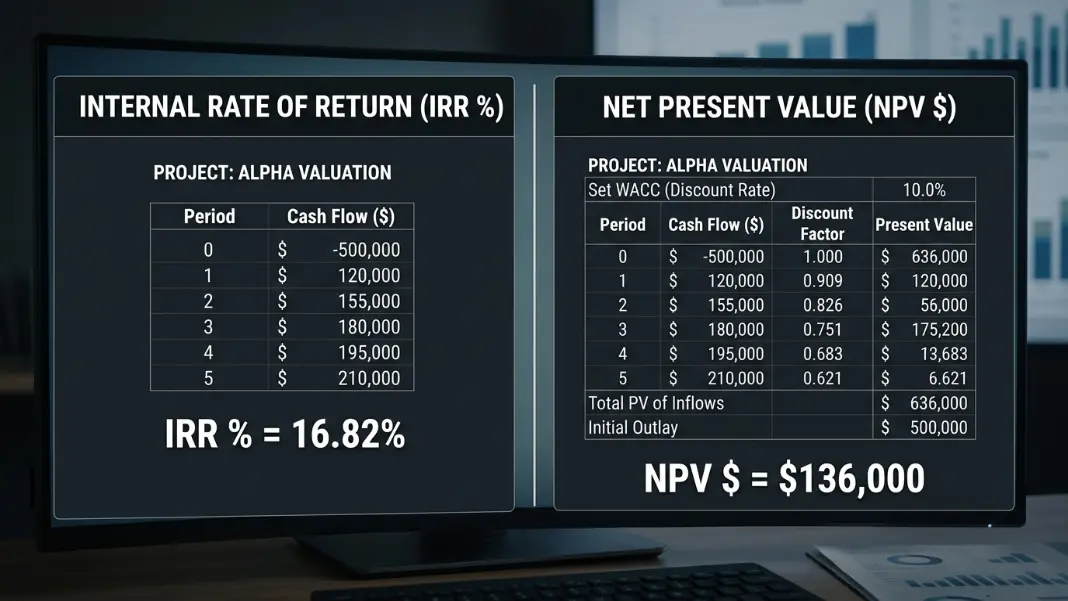

Internal Rate of Return is the discount rate that makes Net Present Value equal to zero across all cash flows. There is no closed-form algebraic solution for most cash flow series, so IRR is solved iteratively. This calculator uses the Newton-Raphson method, which converges to 8 decimal places in most cases.

For a quick estimate without a computer, use the interpolation method:

You buy a rental property for $500,000. It generates $80K-$110K in annual cash flows over 5 years and you sell for $650,000 in Year 6 (included in the Year 6 cash flow).

Accept a project if IRR exceeds your required rate of return (hurdle rate). If your cost of capital is 10% and the IRR is 18.4%, the investment adds value. NPV at 10% is positive. If IRR falls below your hurdle rate, NPV is negative and the project destroys value relative to alternatives.

Excel offers three IRR functions. Choosing the right one matters more than most people realize, particularly for real estate and private equity deals where cash flows do not fall cleanly at year-end.

MIRR corrects a known flaw in standard IRR: the assumption that interim cash flows are reinvested at the same IRR rate. A deal returning 25% IRR does not mean you will reinvest those distributions at 25%. MIRR uses a realistic reinvestment rate (typically 5-8%) and is more conservative. Use MIRR when comparing projects with very different cash flow timing or when early distributions are large.

For most residential real estate models, =IRR works fine. For commercial deals with irregular closing dates and capital calls, =XIRR is the right choice.

The table below shows how NPV changes as the discount rate increases for the default example ($500K investment, $80K-$110K annual cash flows, $650K exit in Year 6). IRR is the rate where NPV crosses zero.

| Discount Rate | NPV | Decision |

|---|---|---|

| 5% | +$390,000 | Accept |

| 10% | +$189,000 | Accept |

| 15% | +$48,000 | Accept |

| 18.4% (IRR) | $0 | Breakeven |

| 20% | -$27,000 | Reject |

| 25% | -$130,000 | Reject |

Building this table by hand is exactly how manual IRR interpolation works: find two rates that straddle zero NPV, then interpolate. At 15%, NPV is +$48K. At 20%, NPV is -$27K. Interpolated IRR = 15% + [48/(48+27)] x 5% = 18.2%, close to the exact 18.4%.

Real estate IRR models have three components: the initial acquisition cost (Year 0 outflow), annual net operating income minus debt service (Years 1+), and sale proceeds minus selling costs in the exit year. Getting the annual cash flows right requires accurate NOI. Use the Cap Rate Calculator to determine your property's income before running the IRR model.

| Strategy | Target IRR | Typical Hold |

|---|---|---|

| Core (stabilized, low risk) | 8-12% | 7-10 years |

| Core-Plus | 10-14% | 5-7 years |

| Value-Add | 15-18% | 3-5 years |

| Opportunistic / Development | 18-25%+ | 2-4 years |

| Single-Family Rental (SFR) | 10-16% | 5-10 years |

IRR models equity return after debt service, not property-level return. Subtract your annual mortgage payments from NOI to get each year's cash flow. Use the Commercial Mortgage Calculator to find annual debt service, then subtract it from each year's NOI before entering it above. For deals where lenders require income coverage analysis, the DSCR Loan Calculator shows whether your NOI is sufficient to qualify for the loan.

IRR and NPV answer different questions. IRR tells you the annualized return rate, which is easy to compare to a hurdle rate or benchmark. NPV tells you the total dollar value added at a specific cost of capital. They often agree on whether to accept or reject a project, but they can conflict when comparing investments of different sizes or cash flow timing.

| Question | Use IRR | Use NPV |

|---|---|---|

| Does this beat my hurdle rate? | Yes, compare directly | Indirectly (positive NPV = yes) |

| Which investment creates more wealth? | Can mislead on different sizes | NPV is the right metric |

| Comparing investments of unequal size? | Use with caution | More reliable |

| Communicating return to investors? | Standard for fund reporting | Less intuitive for most |

| Irregular cash flow timing? | Use XIRR variant | Discount at any rate |

A 25% IRR on a $50,000 investment produces $12,500 in Year 1 profit. A 15% IRR on a $500,000 investment produces $75,000. The larger deal creates six times the wealth despite the lower percentage return. When capital allocation matters, always run NPV alongside IRR before making a final decision.

Researches and verifies the formulas, methodology, and source data behind each calculator on CalculatorFlux. All tools are built and checked against the cited references before publication.

In-depth guides related to this calculator.