Commercial mortgage payments use standard amortization: each payment covers the monthly interest due plus a portion of the principal. The interest share is highest at the start and shrinks over time as the balance falls. The formula is identical to residential mortgages; what differs is the typical term structure, rate, and underwriting criteria.

The Commercial Mortgage Payment Formula

Monthly Payment = P × [r(1+r)^n] / [(1+r)^n - 1]

P = loan amount · r = monthly rate (annual / 12) · n = months

Example: $1,000,000 at 7.25% for 25 years = $7,230/mo

Total interest paid: $1,169,000 over 25 years

The monthly payment calculated here is principal and interest only. To determine whether the property income actually covers the loan, use the DSCR Loan Calculator, which tells you whether your NOI meets the lender's minimum debt service coverage ratio.

Example Calculation

You are buying a $1,250,000 retail building. You put 20% down ($250,000), borrowing $1,000,000 at 7.25% amortized over 25 years.

Loan: $1,000,000

Rate: 7.25% (0.6042% monthly)

Term: 25 years (300 months)

Monthly P&I: $7,230

Total paid: $2,169,000

Total interest: $1,169,000

If this property generates $96,000/year in NOI ($8,000/month), your annual debt service is $86,760, giving a DSCR of 1.11. Most lenders require 1.25 DSCR, so you would need higher NOI or a lower purchase price. To model the property return before adding debt, run the Cap Rate Calculator first to confirm the NOI justifies the purchase price at current market cap rates.

25-Year vs 30-Year Commercial Mortgage

Most commercial lenders offer amortization periods of 15, 20, 25, or 30 years. The choice has a significant impact on both monthly payment and total interest paid. On a $1,000,000 loan at 7.25%:

Term

Monthly Payment

Total Interest

vs 25-Year

15 years

$9,122/mo

$641,000

Save $528,000

20 years

$7,846/mo

$883,000

Save $286,000

25 years

$7,230/mo

$1,169,000

Baseline

30 years

$6,824/mo

$1,456,000

+$287,000 more

Commercial Mortgage Amortization Schedule

A longer amortization lowers your monthly payment and improves cash flow, but you pay significantly more interest over the life of the loan. Most investment property lenders cap amortization at 25 years. Owner-occupied SBA 504 loans can go to 25 years on real estate.

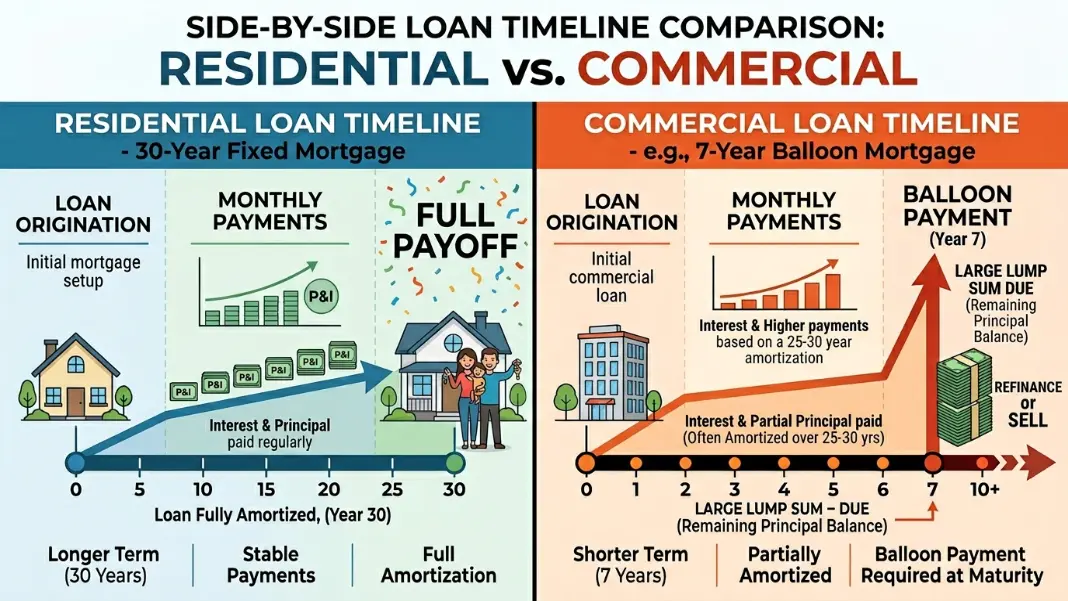

Remember that commercial loans often have balloon payments: you may amortize over 25 years but owe the full remaining balance after a 7 or 10-year term. For a complete investment return analysis that accounts for hold period, exit, and cash flows, the IRR Calculator puts the total picture in perspective.

Common Commercial Mortgage Mistakes

Ignoring balloon payment risk

Many commercial loans amortize over 25 to 30 years but carry a 5 or 7-year term with a balloon. Borrowers who do not plan for refinancing or sale at maturity can face forced liquidation at unfavorable market conditions.

Comparing LTV limits to residential mortgages

Residential loans allow 80 to 97% LTV. Most commercial lenders cap at 65 to 75% LTV. Underestimating the equity requirement is the most common reason commercial loan applications fall through at the last stage.

Overlooking DSCR requirements in the pre-approval phase

Lenders require a minimum debt service coverage ratio, typically 1.20 to 1.25x. A property with thin cash flow may appraise at the expected value but still fail to qualify because its income does not cover the debt service comfortably.

Not accounting for prepayment penalties

Commercial loans commonly include yield maintenance or defeasance clauses. Selling or refinancing before the penalty window closes can cost 2 to 5% of the remaining balance, materially changing the deal economics.

Forgetting capital reserve requirements

Many lenders require escrow or reserve accounts for roof, HVAC, and major system replacements. These reserves can add $100 to $500 per unit annually to effective carrying costs that do not appear in the stated payment amount.

Mortgage Bankers Association: annual report on commercial mortgage origination volume and market conditions

HR

Hassaan Rasheed

Developer and Researcher, CalculatorFlux

Researches and verifies the formulas, methodology, and source data behind each calculator on CalculatorFlux. All tools are built and checked against the cited references before publication.

Last updated: June 2026

Frequently Asked Questions

Monthly Payment = P × [r(1+r)^n] / [(1+r)^n - 1], where P is the loan amount, r is the monthly interest rate (annual rate / 12), and n is the total number of months. For a $1,000,000 loan at 7.25% over 25 years: r = 0.0725/12 = 0.006042, n = 300, monthly payment = $7,230. Most lenders use this same formula.

Approximate ranges. Verify current rates with lenders.

Pro Tip

A 25-year amortization vs 20-year on a $1M loan at 7.25% saves $616/month but costs an extra $286,000 in total interest. If the monthly savings are what you need to qualify or maintain cash flow, the trade-off can be worth it.