How to Calculate Your Coast FIRE Number

Find the portfolio balance where your money grows to your FIRE number without new contributions.

7 min readRead →

Free Coast FIRE calculator to find your coast fire number: the amount you need invested today so compound growth alone reaches your retirement goal. Works for couples, supports pension and Social Security adjustments, and shows the exact age you coast.

To find your coast fire number, the calculator works backward from your retirement goal. First it finds the retirement corpus you need: annual expenses divided by your withdrawal rate. Then it discounts that corpus back to today at your expected return rate. The result is the savings balance at which compound growth alone handles the rest. Maximizing a Roth IRA in your 20s and 30s is one of the most efficient ways to hit that number, since contributions compound tax-free for decades.

Priya is 34, plans to retire at 60, wants $65,000/year in retirement, has $110,000 saved, and assumes 7% growth with the 4% withdrawal rule.

Once Priya hits Coast FIRE at 40, she can stop retirement contributions entirely. Her $277,400 grows to $1.625M by age 60 through compound returns alone. For many households, clearing high-interest debt with a debt snowball plan frees up the cash flow needed to reach that coast number faster.

The earlier you start, the smaller your coast fire number is. Compound growth does more work when it has more years. At 25 with 35 years to a retirement at 60, you need less than $100,000 to coast to a $1 million corpus. By 40, that same target requires over $250,000. The table below assumes a 7% annual return, a 4% withdrawal rate, and retirement at age 60.

| Current Age | Years to 60 | $40k/yr expenses | $60k/yr expenses | $80k/yr expenses |

|---|---|---|---|---|

| 25 | 35 | $94,000 | $141,000 | $188,000 |

| 30 | 30 | $131,000 | $197,000 | $263,000 |

| 35 | 25 | $184,000 | $276,000 | $368,000 |

| 40 | 20 | $258,000 | $388,000 | $517,000 |

| 45 | 15 | $362,000 | $544,000 | $725,000 |

| 50 | 10 | $508,000 | $763,000 | $1,017,000 |

Assumes 7% annual return, 4% withdrawal rate, retirement at age 60. Coast FIRE number = (annual expenses x 25) / (1.07^years to retirement).

These numbers drop considerably if you use a 3.5% withdrawal rate (more conservative) or a later retirement age. Run the calculator above with your specific assumptions to get a precise number for your situation.

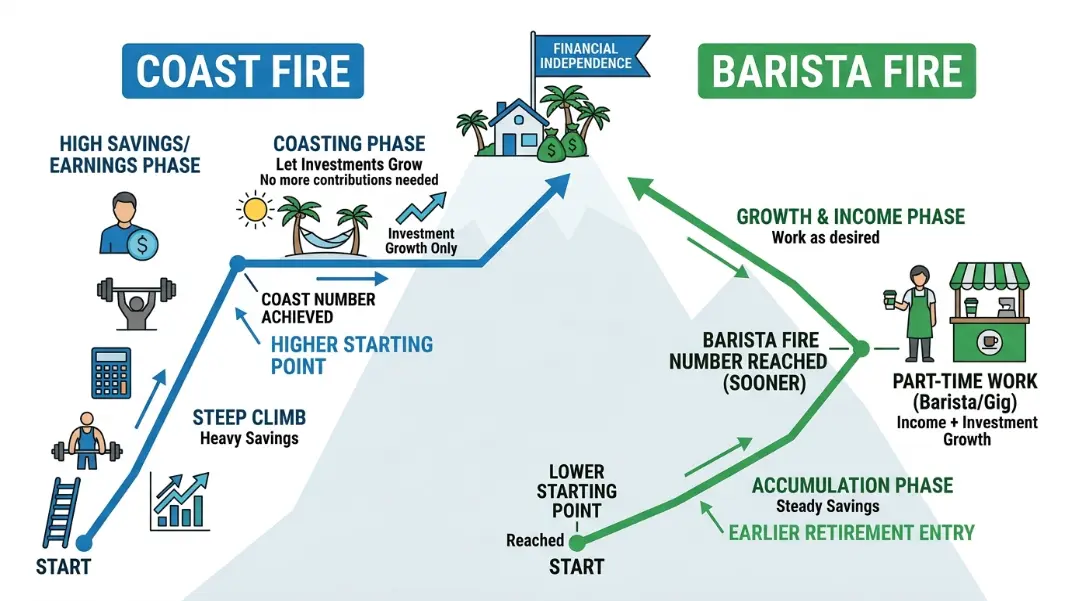

Both strategies let you stop saving aggressively for retirement before traditional retirement age, but they get there through different mechanics. Coast FIRE uses portfolio size alone. Barista FIRE relies on a combination of a smaller portfolio and ongoing part-time income. Which one gets you there faster depends on your current balance, your savings rate, and whether you are willing to keep working part-time.

| Attribute | Coast FIRE | Barista FIRE |

|---|---|---|

| Portfolio required | Larger (covers full corpus growth) | Smaller (only covers expense gap) |

| Earned income after milestone | Not required | Required, part-time ongoing |

| Stop making contributions? | Yes | Yes |

| Reach milestone sooner? | Requires more saved first | Yes, due to income offset |

| Health insurance source | ACA or out of pocket | Employer (20+ hrs) or ACA |

| Key risk | Market growth falls short | Part-time income disappears |

| Best fits | Those who want full freedom sooner | Those comfortable with part-time work |

Some people reach Coast FIRE first, then transition to part-time work while the portfolio grows toward full FIRE. That layered approach combines the strengths of both strategies. Use the Barista FIRE Calculator to see how much part-time income would reduce your required portfolio, and compare that timeline to your coast number above.

Your coast fire number is a portfolio balance, not a net worth figure. What you include in "current savings" matters significantly, and not every asset belongs in the calculation.

Home equity, emergency fund cash, 529 college savings, and illiquid assets like rental property equity do not belong in your coast FIRE balance. The coast number assumes liquid, market-invested assets growing at your expected return rate.

Both reduce what your portfolio must fund. Subtract expected annual income from your annual expenses input before running the calculation. If you plan to spend $70,000 per year and your pension pays $22,000 annually, enter $48,000 as annual expenses. Your coast number drops from $471,000 to $325,000 at age 35 with a 25-year runway (7% return, 4% withdrawal).

Federal employees with FERS benefits can estimate their pension using the FERS Retirement Calculator before entering their adjusted expense figure here.

Researches and verifies the formulas, methodology, and source data behind each calculator on CalculatorFlux. All tools are built and checked against the cited references before publication.

In-depth guides related to this calculator.