How to Calculate Your Coast FIRE Number

Find the portfolio balance where your money grows to your FIRE number without new contributions.

7 min readRead →

Your Barista FIRE number is smaller than full FIRE because your portfolio only needs to fund the portion of expenses that part-time income does not cover. Two inputs drive the math: the annual expense gap and your chosen withdrawal rate.

With a 4% withdrawal rate, every $1,000/month in part-time income reduces your Barista FIRE number by $300,000. Even a modest income stream has an outsized impact. Jordan spends $60,000/year and plans to work part-time earning $2,500/month ($30,000/year) as a freelance consultant, with $180,000 saved and $22,000/year in contributions at 7% return:

Jordan needs only half the portfolio that full FIRE would require, potentially shaving a decade off the timeline to leaving full-time work. For the full FIRE equivalent, see the Coast FIRE Calculator to see how long your portfolio can grow on its own.

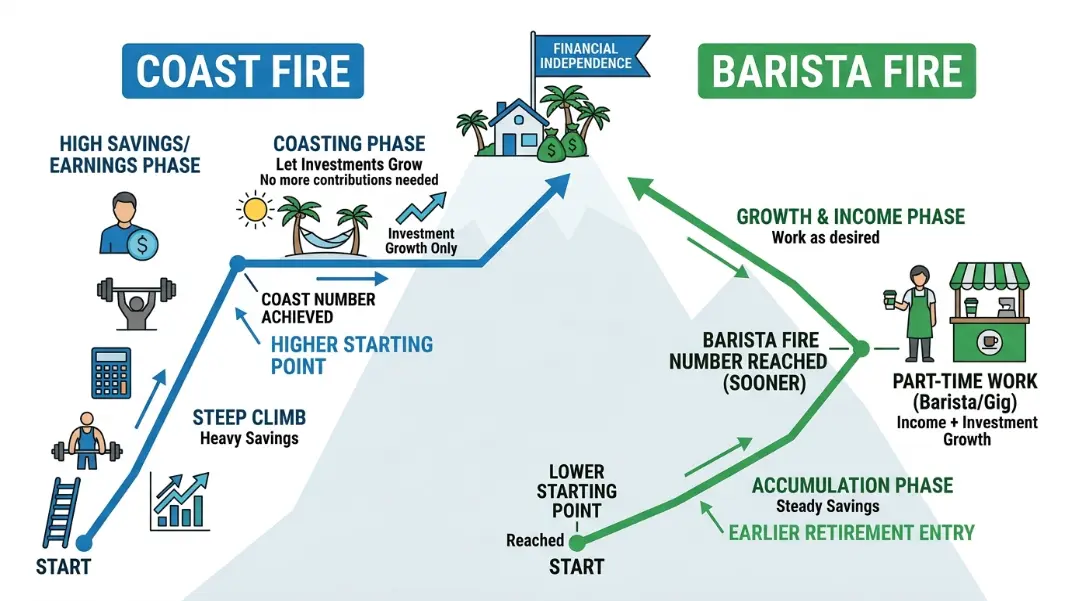

Barista FIRE is a form of semi-retirement where you leave a high-stress full-time career and replace it with part-time work at a lower-pressure job. Your investment portfolio covers the remaining gap between your earnings and expenses. The concept originated in the FIRE community from the idea of working at a Starbucks or similar employer that offers health insurance to part-time staff, solving the health coverage problem that stops many early retirees.

The portfolio reduction effect of part-time income is substantial. The table below shows how much your Barista FIRE number drops at 4% withdrawal for every $1,000/month in earned income, versus the baseline full FIRE number at $60,000/year expenses:

| Monthly Part-Time Income | Annual Income | FIRE Number (4%) | Reduction vs Full FIRE |

|---|---|---|---|

| $0 (Full FIRE) | $0 | $1,500,000 | -- |

| $1,000/mo | $12,000 | $1,200,000 | -$300,000 |

| $2,000/mo | $24,000 | $900,000 | -$600,000 |

| $3,000/mo | $36,000 | $600,000 | -$900,000 |

| $4,000/mo | $48,000 | $300,000 | -$1,200,000 |

| $5,000/mo | $60,000 | $0 | -$1,500,000 |

Both Barista FIRE and Coast FIRE let you stop full-time work before traditional retirement age, but the mechanics differ. Barista FIRE relies on ongoing part-time income to reduce the portfolio requirement now. Coast FIRE relies on portfolio growth over time, with no earned income required. The right choice depends on whether you want to stop working entirely sooner, or transition to part-time work sooner. Use the Savings Duration Calculator to model how long a given portfolio balance would last at various withdrawal rates.

| Attribute | Barista FIRE | Coast FIRE |

|---|---|---|

| Part-time work required | Yes, ongoing | No (optional) |

| Portfolio must cover | Expense gap after income | Full FIRE number eventually |

| Stop making contributions | Yes | Yes (earlier) |

| Health insurance source | Employer or ACA | ACA or out of pocket |

| Key risk | Income loss or reduction | Market growth shortfall |

| Best fits | Those who enjoy lower-stress work | Those who want to stop saving now |

The original Barista FIRE concept centered on jobs that offer employer health insurance at part-time hours. Today the model is broader: any reliable part-time income source reduces your required portfolio. The table below covers common choices with approximate income ranges and health benefit eligibility:

| Job | Hours | Health Insurance | Monthly Pay Range |

|---|---|---|---|

| Starbucks barista | 20+ hrs/wk | Yes (20+ hrs) | $1,400-$2,200 |

| Costco warehouse | 24+ hrs/wk | Yes (24+ hrs) | $1,800-$2,800 |

| REI retail | 20+ hrs/wk | Yes (20+ hrs) | $1,400-$2,000 |

| UPS package handler | Part-time | Yes | $1,600-$2,400 |

| Library assistant | Part-time | Public sector | $1,600-$2,400 |

| Adjunct instructor | Per course | Usually no | $2,000-$4,500 |

| Remote customer service | Flexible | Sometimes | $1,400-$2,000 |

| Freelance consulting | Project-based | No | Varies widely |

Workers whose reduced part-time income brings them below ACA subsidy thresholds ($21,870 for an individual in 2025) may qualify for significant premium tax credits, making employer health insurance unnecessary.

Researches and verifies the formulas, methodology, and source data behind each calculator on CalculatorFlux. All tools are built and checked against the cited references before publication.

In-depth guides related to this calculator.