Coast FIRE vs Barista FIRE: Which Strategy Reaches FI Faster? (2026)

Coast FIRE needs a larger portfolio but no part-time income. Barista FIRE gets you there sooner with less saved. Compare numbers and timelines.

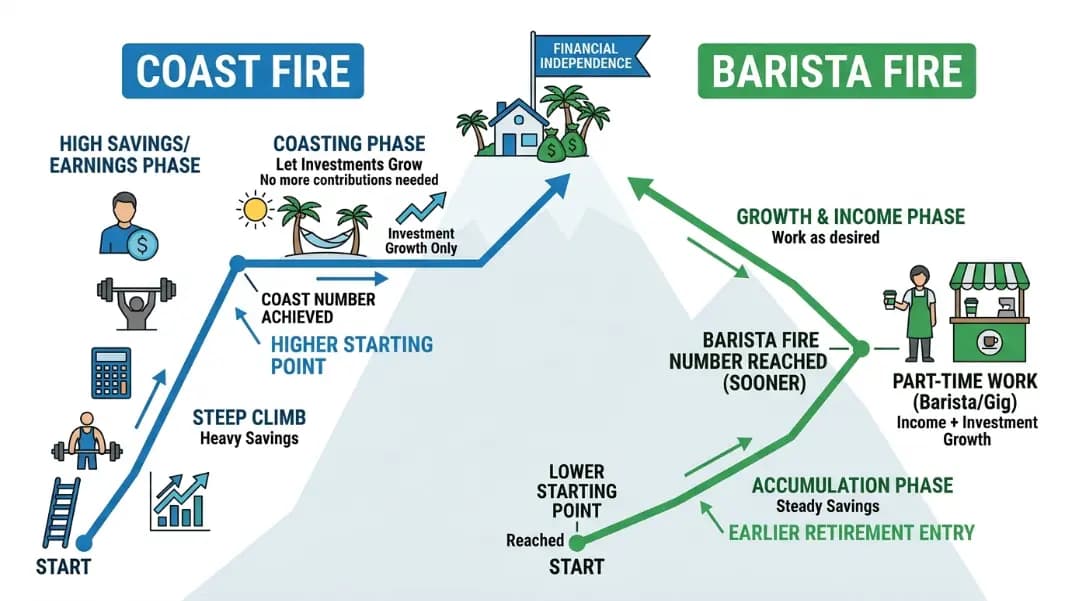

Both Coast FIRE and Barista FIRE let you stop aggressive saving before traditional retirement age. The strategies split on one question: how much ongoing income do you need after crossing the milestone?

Coast FIRE means your portfolio is large enough that compound growth alone, with no further contributions and no earned income required, will reach your full retirement number by your target retirement age. Barista FIRE means you work part-time to cover current living expenses while a smaller portfolio grows in the background. Coast FIRE sets a higher savings bar upfront but requires nothing from you afterward. Barista FIRE gets you to semi-retirement faster but keeps you tied to some form of earned income.

The Coast FIRE Calculator and the Barista FIRE Calculator run the exact numbers for each path. This article explains how the two strategies compare, which one you reach first, and how to calculate both thresholds given your own expenses and timeline.

What Each Strategy Actually Requires

Coast FIRE is a portfolio milestone. Once your invested balance reaches the Coast FIRE number, you stop contributing entirely. Your portfolio grows without any additional input. You still work to cover current living expenses, but the retirement problem is solved. The portfolio handles the long-term compounding. You just need to earn enough to live on month to month.

Barista FIRE sets a lower portfolio threshold. The strategy assumes you shift to part-time or low-stress work that covers your current living expenses, and sometimes health insurance through an employer. Your portfolio, though smaller, grows passively alongside that earned income. The name comes from the idea of taking a job at a large retailer or coffee chain that offers benefits to part-time employees, but in practice it applies to any sustainable part-time income situation.

The critical difference is what you need from work after crossing the milestone.

At Coast FIRE: you need earned income only to cover current expenses. No contributions. Work is optional above the bare survival level.

At Barista FIRE: you need earned income to cover current expenses AND that income is a structural part of the plan. Your portfolio is not large enough to coast on its own unless your expenses are being partially subsidized by work.

Both strategies eventually reach the same destination: full financial independence where the portfolio funds everything. The path and timeline to get there differ significantly.

The Numbers Compared Directly

Working from a concrete example makes the difference obvious. Assume: $60,000 in annual retirement expenses, 4% withdrawal rate (full FIRE number = $1,500,000), current age 35, target retirement at 60, and a 7% real annual return.

Coast FIRE number at age 35:

Coast FIRE Number = Full FIRE Number / (1 + return)^years to retirement

Coast FIRE Number = $1,500,000 / (1.07)^25

= $1,500,000 / 5.427

= $276,500

With $276,500 invested at 35, the portfolio reaches $1,500,000 by age 60 with zero additional contributions.

Barista FIRE number at age 35:

Suppose your part-time job covers $30,000 of your $60,000 annual expenses. Your portfolio only needs to fund the remaining $30,000.

Adjusted FIRE number = $30,000 / 0.04 = $750,000

Barista FIRE threshold = $750,000 / (1.07)^25

= $750,000 / 5.427

= $138,200

With $138,200 invested at 35 and part-time income covering $30,000/year in expenses, the portfolio grows to $750,000 by 60, fully funding the remaining expenses at the 4% withdrawal rate.

The numbers look like this side by side:

| Metric | Coast FIRE | Barista FIRE |

|---|---|---|

| Portfolio needed at 35 | $276,500 | $138,200 |

| Ongoing earned income required | No | Yes (covers $30k/yr) |

| Contributions after milestone | None | None |

| Full financial independence | At retirement (60) | At retirement (60) |

| Semi-retirement begins | When $276,500 is reached | When $138,200 is reached |

The Barista FIRE threshold is 50% lower in this scenario. That gap is smaller or larger depending on how much part-time income covers. The more expenses part-time income absorbs, the lower the Barista FIRE portfolio threshold, and the faster you reach it.

Which Strategy Lets You Leave Full-Time Work Sooner

Barista FIRE wins on speed to semi-retirement, in most cases by a significant margin.

A person saving $2,000/month from a starting balance of $50,000 reaches:

- $138,200 (Barista FIRE threshold in this example) in roughly 4 months

- $276,500 (Coast FIRE threshold) in roughly 4.5 years

Starting from zero with the same $2,000/month:

- $138,200 in approximately 5 years

- $276,500 in approximately 9 to 10 years

That 4 to 5-year gap is real, and it represents years of full-time demanding work that Barista FIRE avoids. If the goal is to exit high-stress full-time employment as fast as possible, and you are comfortable with part-time work long term, Barista FIRE reaches that exit point substantially sooner.

The trade-off is ongoing income dependency. Barista FIRE assumes part-time work remains available, sustainable, and adequate to cover expenses. If part-time income drops, if expenses rise, or if health makes sustained work difficult, the smaller portfolio may not be sufficient to absorb the gap. Coast FIRE eliminates that dependency entirely. Once you hit the Coast FIRE number, your retirement is secure regardless of whether you ever earn another dollar.

For households where one partner works full-time and the other wants to step back, Barista FIRE is a practical framework. The part-time income assumption is already built into the household's income structure. Coast FIRE is more appropriate for single-income households or couples where both partners want to eventually go work-optional.

How to Calculate Your Own Numbers

Step 1: Determine your annual retirement expenses Start with current annual spending. Remove work-specific costs (commuting, lunches, business wardrobe) since those disappear in retirement. Add healthcare costs if you plan to retire before Medicare eligibility at 65. Most planners use 80% to 100% of current spending as the baseline.

Step 2: Calculate your full FIRE number Multiply retirement expenses by 25 (the 4% rule). If expenses are $55,000, the full FIRE number is $1,375,000.

Step 3: Set your target retirement age and current age The gap between these two is the compounding period. Longer gaps produce smaller required balances today. Moving the retirement age from 60 to 65 at a 7% real return reduces the required portfolio by roughly 30%.

Step 4: Coast FIRE calculation

Coast FIRE = Full FIRE Number / (1 + real return)^years to retirement

Use a real (after inflation) return. 5% to 6% is conservative. 7% is common for heavily equity-weighted portfolios. Using real returns keeps the Coast FIRE number and the FIRE target in the same dollar terms (today's dollars).

Step 5: Barista FIRE calculation Estimate reliable annual part-time income. Subtract it from annual retirement expenses to find the portfolio's required coverage. Apply the 25x multiplier to the reduced figure. Apply the same coast formula to find the Barista threshold.

The Coast FIRE Calculator handles the coast formula. For the Barista version, enter your reduced (post-part-time-income) expense figure rather than your full expenses.

If you contribute to a Roth IRA or 401(k), reaching either milestone faster depends on maximizing those accounts. The Roth IRA Contribution Calculator shows how much you can add each year based on your income and filing status.

Choosing Between Coast FIRE and Barista FIRE Based on Your Situation

The right choice depends on your financial situation, your tolerance for ongoing work, and your confidence in part-time income.

Coast FIRE is the better fit when:

- Your current full-time income is high enough that a few more years of saving gets you to the coast number before burnout

- You want complete work optionality after crossing the milestone (no income required for any purpose)

- Your expenses are variable or rising (children, housing costs) and part-time income cannot reliably cover them

- You plan to retire internationally and want income-independent security

Barista FIRE is the better fit when:

- Burnout is immediate and part-time work in the near term is genuinely sustainable

- You have a specific low-stress job or freelance arrangement that already covers your expenses

- Health insurance through a part-time employer is a meaningful benefit (Barista FIRE originated partly as a solution to the pre-Medicare coverage gap)

- Your full-time income is moderate and reaching the Coast FIRE threshold would take 10 or more years

A hybrid approach works well for many households: reach the Barista FIRE threshold, shift to low-stress part-time work, and continue making modest contributions until the portfolio crosses the Coast FIRE number. At that point, contributions stop entirely. The part-time income covers expenses while the portfolio coasts the rest of the way to full FIRE.

Neither path requires sacrificing full financial independence. Both arrive at the same destination. The difference is the size of the initial portfolio required, the speed of reaching semi-retirement, and the amount of ongoing income you need from work during the transition years.

Coast FIRE requires more. For a $1,500,000 FIRE target at age 35 retiring at 60, Coast FIRE needs roughly $276,500 invested at a 7% real return. Barista FIRE's threshold depends on part-time income, but if part-time work covers half your expenses, the required portfolio at 35 drops to about $138,200. The gap shrinks as returns increase or the retirement horizon extends.

Yes. A common approach is to reach Barista FIRE first, shift to part-time work that covers expenses, and continue small contributions until you hit the Coast FIRE number. At that point, contributions stop entirely and the portfolio coasts without any earned income requirement. Using both as sequential checkpoints gives you an early exit from demanding work and a clear endpoint for contributions.

$20,000 to $40,000 per year is the common range depending on hours and role. The income needs to reliably cover living expenses, not just supplement savings. If annual expenses are $55,000 and part-time income is $30,000, the portfolio only needs to fund $25,000 annually at retirement, reducing the FIRE target to $625,000 and cutting the required portfolio today in half.

Use a real (after inflation) return rather than a nominal one. If your portfolio earns 9% nominally and inflation runs 3%, your real return is approximately 6%. Using 5% to 6% real is conservative for a diversified equity portfolio. Using 7% reflects historical US stock market data more closely. Run both to understand the range: the difference between a 5% and 7% real return over 25 years changes the required balance by about 35%.

No. The retail framing is just the origin of the name. Barista FIRE applies to any part-time or reduced-effort income situation: freelancing 15 hours a week, consulting in your former field at reduced capacity, seasonal work, or a 3-day-a-week salaried role. The only requirement is that earned income covers current living expenses so the portfolio grows without withdrawals.

The portfolio has to absorb the gap. If the portfolio has not yet grown to the full FIRE number, drawing it down early can derail the timeline significantly. This is the main risk of Barista FIRE versus Coast FIRE. A Coast FIRE household can stop working entirely at any time without affecting the retirement projection. A Barista FIRE household that loses part-time income before the portfolio is large enough faces a real shortfall. Building a 12-month expense reserve alongside the Barista FIRE portfolio reduces this risk.

Written by

Hassaan Rasheed

Web Developer & Content Researcher

Hassaan builds calculators and writes research-backed guides on finance, math, payroll, and construction topics. Every number in his articles is sourced from official data and worked through by hand.

View LinkedIn Profile