Commercial Mortgage Calculator: How Lenders Size Payments (2026)

Commercial mortgage payments depend on rate, amortization, and balloon term. DSCR determines approval. Worked examples with real numbers.

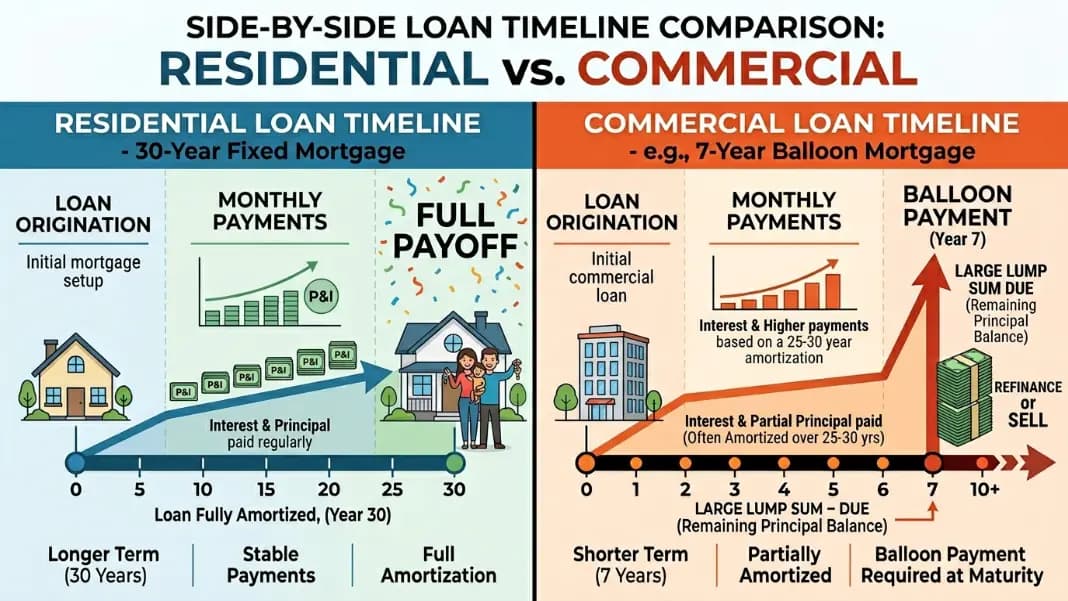

Commercial mortgages work differently from home loans in ways that catch buyers off guard. The payment formula is the same, but the loan structure, approval criteria, and exit terms are distinct. Most commercial loans have a balloon payment: a 20- or 25-year amortization schedule, but a 5- or 10-year term that forces the full remaining balance to come due years before the loan would be paid off.

The Commercial Mortgage Calculator handles payment, amortization, and balloon calculations. This guide explains how the numbers work, what lenders look at before approving, and how to use DSCR to determine whether a property can carry the debt.

How Commercial Mortgage Payments Are Calculated

The monthly payment formula is identical to a residential mortgage:

M = P x [r(1+r)^n] / [(1+r)^n - 1]

Where:

- M = monthly payment

- P = loan principal

- r = monthly interest rate (annual rate divided by 12)

- n = total number of payments (amortization period in months)

Worked example:

- Loan: $1,200,000

- Rate: 7.50% per year

- Amortization: 25 years (300 months)

- Monthly rate: 7.50% / 12 = 0.625% = 0.00625

M = 1,200,000 x [0.00625 x (1.00625)^300] / [(1.00625)^300 - 1]

(1.00625)^300 = 6.484

M = 1,200,000 x [0.04053] / [5.484] = 1,200,000 x 0.007391 = $8,869 per month

Annual debt service: $8,869 x 12 = $106,428

This annual debt service figure is used directly in the DSCR calculation that determines whether the lender approves the loan.

Balloon Payments: The Critical Difference from Residential

A 30-year residential mortgage has a 30-year term and 30-year amortization. The loan is fully paid off at month 360.

A commercial mortgage typically has a 25-year amortization but a 7-year term. You make payments calculated on a 25-year payoff schedule, but after 7 years the remaining principal balance is due in full. That lump sum is the balloon payment.

Calculating the balloon balance:

Using the loan above ($1,200,000 at 7.50%, 25-year amortization, 7-year balloon):

After 84 payments (7 years), the remaining balance is:

Remaining Balance = P x [(1+r)^n - (1+r)^p] / [(1+r)^n - 1]

Where p = 84 (payments made). Result: approximately $1,074,400 still owed.

That $1,074,400 becomes due at the end of year 7. The borrower must refinance, sell, or pay it off from other funds. This is standard practice in commercial real estate and is not a distress scenario for a creditworthy borrower with a performing asset.

Common commercial loan structures:

| Loan Type | Amortization | Term / Balloon |

|---|---|---|

| SBA 7(a) | 25 years | Fully amortizing (no balloon) |

| SBA 504 | 25 years | Fully amortizing (no balloon) |

| Conventional CRE | 20-25 years | 5, 7, or 10-year balloon |

| Bridge / construction | Interest only | 1-3 years |

| CMBS (conduit) | 25-30 years | 10-year balloon |

SBA loans are among the few commercial products that fully amortize with no balloon, which is why small business owner-occupants often prefer them despite stricter eligibility requirements.

DSCR: The Number That Drives Approval

Debt Service Coverage Ratio (DSCR) is the primary underwriting metric for income-producing commercial properties. Lenders calculate it before reviewing the borrower's personal financial statement.

DSCR = Net Operating Income / Annual Debt Service

Net Operating Income (NOI) = gross potential rental income minus vacancy allowance minus operating expenses. Operating expenses include property taxes, insurance, maintenance, management fees, and reserves. They do not include mortgage payments or income taxes.

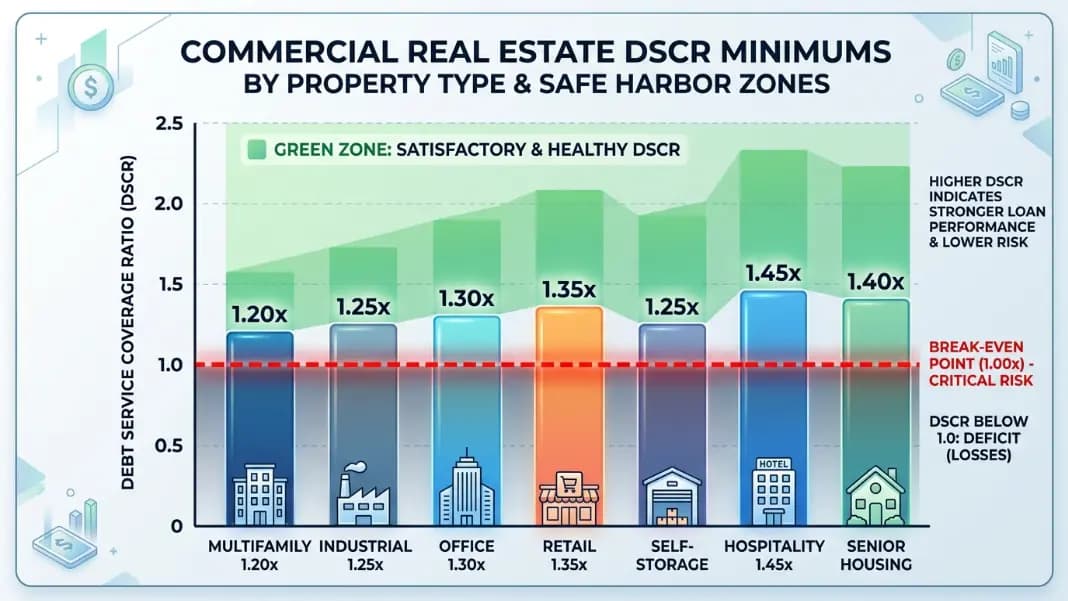

Minimum DSCR by property type:

| Property Type | Minimum DSCR |

|---|---|

| Multifamily (5+ units) | 1.20-1.25 |

| Office / Retail | 1.25-1.30 |

| Industrial / Warehouse | 1.20-1.25 |

| Hotel / Hospitality | 1.35-1.50 |

| Special purpose | 1.40-1.60 |

A DSCR of 1.25 means the property generates 25% more income than needed to cover debt payments. This cushion protects the lender against vacancy increases, unexpected repairs, and rate changes at refinance.

Worked example:

- NOI: $128,000 per year

- Annual debt service: $106,428 (from the example above)

- DSCR: $128,000 / $106,428 = 1.203

This barely clears the 1.20 minimum for a multifamily property. For a retail building requiring 1.30, this loan would be declined. The borrower could qualify by reducing the loan amount (larger down payment), negotiating a lower rate, or demonstrating higher stabilized NOI.

Use the DSCR Loan Calculator to check coverage at different loan scenarios before approaching lenders.

Commercial Mortgage Rates vs Residential

Commercial rates are consistently higher than residential rates for equivalent loan amounts. The spread varies by product, property class, and market conditions.

Approximate rate ranges for 2025-2026:

| Loan Type | Rate Range |

|---|---|

| SBA 7(a) variable | Prime + 2.25-2.75% |

| SBA 504 fixed | 6.0-7.5% |

| Conventional CRE (5-year fixed) | 7.0-8.5% |

| Conventional CRE (10-year fixed) | 7.25-8.75% |

| Bridge loan | 8.5-12.0% |

Why commercial rates are higher:

- No secondary market comparable to Fannie Mae and Freddie Mac for residential loans, so lenders hold more of the risk on their balance sheets

- Higher default risk: commercial properties depend on business performance and tenant health, not just the borrower's personal income

- Lower maximum LTVs (65-75% versus 80-97% for residential), which reflects higher lender risk tolerance thresholds

- Prepayment penalties are standard and substantial

Prepayment penalties are built into almost all commercial loans. A step-down structure (5-4-3-2-1%) means paying off the loan in Year 1 costs 5% of the outstanding balance, Year 2 costs 4%, and so on. Yield maintenance requires paying the difference between your locked rate and current Treasury yields for the remaining term. These provisions can cost tens of thousands of dollars if you sell or refinance before the balloon date.

LTV and Down Payment Requirements

Loan-to-value ratio determines the maximum loan size relative to appraised value. Commercial LTV maximums are lower than residential, requiring larger down payments.

Typical LTV maximums:

| Property Type | Conventional LTV | SBA LTV |

|---|---|---|

| Multifamily (5+ units) | 75-80% | 85-90% |

| Retail / Office | 65-70% | 85-90% |

| Industrial / Warehouse | 70-75% | 85-90% |

| Special purpose | 55-65% | 85-90% |

At 70% LTV on a $1,500,000 property: maximum loan = $1,050,000, required down payment = $450,000. Adding closing costs (1-2% of purchase price) and required operating reserves (3-6 months of debt service), the cash required at closing often reaches 30-35% of the purchase price.

This is a primary reason commercial real estate investors rely on equity partners, bridge loans, or SBA programs for acquisitions where their cash is limited relative to property value.

Commercial mortgage payments use the standard amortization formula: M = P x [r(1+r)^n] / [(1+r)^n - 1], where P is the loan amount, r is the monthly interest rate, and n is the amortization period in months. A $1,200,000 loan at 7.50% with 25-year amortization produces a monthly payment of $8,869. The Commercial Mortgage Calculator runs this for any loan amount, rate, and amortization period.

A balloon payment is the remaining principal balance due at the end of the loan term, which is shorter than the amortization period. Most commercial mortgages amortize over 20-25 years but have a 5- or 10-year term. After making 7 years of payments on a 25-year amortization schedule, roughly 90% of the original balance remains. That amount becomes due as a lump sum. Borrowers typically refinance or sell before the balloon date rather than paying it in cash.

Most commercial lenders require a minimum DSCR of 1.20 to 1.30 depending on property type. Multifamily and industrial typically need 1.20-1.25. Office and retail require 1.25-1.30. Hospitality properties often need 1.35-1.50 due to higher income variability. DSCR is net operating income divided by annual debt service. A property below the minimum can qualify by reducing the loan amount (larger down payment) to lower debt service, or by demonstrating higher NOI.

Conventional commercial lenders generally prefer a personal credit score above 680. SBA 7(a) loans also typically require 680 minimum. However, DSCR and property income performance carry more weight in commercial underwriting than personal credit. A property with strong cash flow and substantial equity can sometimes qualify with a lower credit score, particularly through portfolio lenders who keep loans on their own books rather than selling them.

Rates depend on loan type and term. SBA 504 fixed-rate loans run approximately 6.0-7.5%. Conventional 5-year fixed CRE loans run 7.0-8.5%. Ten-year fixed conventional loans are typically 7.25-8.75%. Bridge loans range 8.5-12%. Commercial rates are generally 150-250 basis points above comparable residential rates due to lower secondary market liquidity and higher lender exposure per transaction.

Key differences: loan term (commercial typically has 5-10 year terms with balloon payments versus 30 years for residential), LTV (65-75% commercial versus 80-97% residential), underwriting basis (property income and DSCR for commercial versus borrower income and DTI for residential), prepayment penalties (standard in commercial, uncommon in residential), and interest rates (100-250 basis points higher for commercial). Commercial loans are also exempt from most consumer protection regulations that govern residential mortgage lending.

Written by

Hassaan Rasheed

Web Developer & Content Researcher

Hassaan builds calculators and writes research-backed guides on finance, math, payroll, and construction topics. Every number in his articles is sourced from official data and worked through by hand.

View LinkedIn Profile