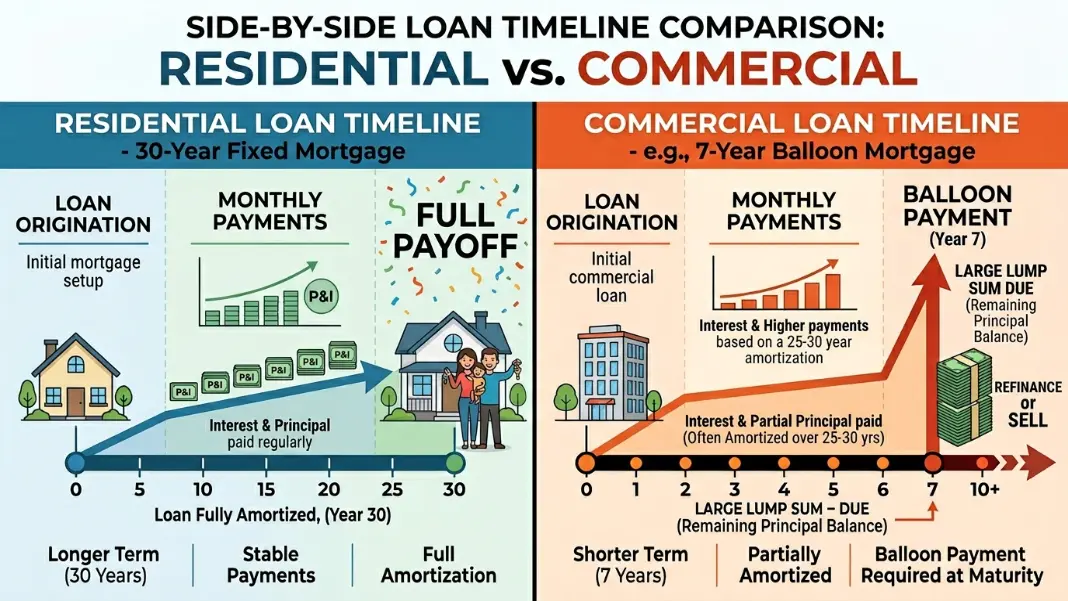

CRE loans separate two time frames: the amortization period, which sets the monthly payment, and the loan term, which is when the balloon payment is due. Monthly payments are calculated as if the loan runs the full amortization period, but at the end of the shorter term you must pay the remaining balance. Use the Cap Rate Calculator to verify a property's yield before modeling the debt structure.

Balloon = remaining principal after loan term months

$2M at 7.0%, 25yr amort, 10yr term: $14,126/mo, ~$1.62M balloon

Commercial Real Estate Loan Down Payment Requirements

Down payment requirements vary by property type, loan program, and borrower profile. Investment properties require more equity than owner-occupied. The table below reflects typical bank and insurance company lender minimums as of 2026.

Property Type

Max LTV

Min Down Payment

Multifamily (5+ units)

80%

20%

Industrial / Warehouse

75%

25%

Office (stabilized)

70%

30%

Retail (anchored)

70%

30%

Hotel / Hospitality

65%

35%

SBA 504 (owner-occupied)

90%

10%

Types of Commercial Real Estate Loans

Each loan type targets a different situation. Permanent loans are for stabilized, income-producing properties. Bridge loans cover transitions. Construction loans fund new builds. Use the Commercial Mortgage Calculator to model standard permanent loan scenarios.

Loan Type

Term

Max LTV

Best For

Permanent / Conventional

5-10 yr term, 25-30 yr amort

75%

Stabilized income properties

Bridge Loan

6-36 months

70%

Renovation, lease-up, repositioning

Construction Loan

12-36 months

70%

Ground-up development

SBA 504

20-25 years

90%

Owner-occupied only

CMBS Loan

10 years fixed

75%

Non-recourse, large assets

Hard Money

12-24 months

65%

Fast close, distressed assets

Commercial Real Estate Loan Requirements

Lenders underwrite both the borrower and the property. The property must generate enough income to service the debt. The borrower must show creditworthiness and liquidity. Use the DSCR Loan Calculator to verify your property meets the debt service coverage threshold before applying.

DSCR

Minimum 1.20x to 1.25x. Property NOI divided by annual debt service. A DSCR below 1.0 means the property cannot cover its own loan payments.

LTV

Maximum 65 to 80 percent depending on property type. Higher LTV means more risk for the lender and typically a higher interest rate.

Credit Score

Most banks require a minimum 680 personal credit score. Life companies and CMBS lenders may require 700 or above. Hard money lenders are more flexible.

Net Worth

Many lenders require the borrower's net worth to equal or exceed the loan amount. This demonstrates financial depth beyond the property itself.

Liquidity / Reserves

6 to 12 months of debt service in liquid reserves, typically in bank or brokerage accounts. Some lenders require this in escrow at closing.

Operating History

2 years of property operating statements for investment properties. New construction requires a detailed pro forma with market rent comparables.

Example Calculation

You are financing a $2.5M office building with a $2M loan at 7.0 percent interest, amortized over 25 years with a 10-year balloon. Before applying, verify the property meets DSCR requirements with the DSCR Loan Calculator.

Loan: $2,000,000 at 7.0%

Amortization: 25 years (300 months)

Monthly payment: $14,126

After 10 years: $1,623,000 balloon due

You must refinance or sell before year 10.

Common CRE Loan Mistakes

Not planning for the balloon payment at maturity

Commercial real estate loans typically amortize over 25 to 30 years but carry 5 to 10-year terms. At maturity, the full remaining principal is due. Borrowers who do not plan for refinancing or sale at term end face forced liquidation, often at unfavorable market conditions.

Underestimating the equity required

Most CRE lenders cap LTV at 65 to 75%, compared to 80 to 97% in residential markets. Assuming residential-style financing is the most common reason commercial loan applications fall apart in the late stages after significant time has been invested.

Applying without first checking DSCR

Most CRE lenders require a minimum debt service coverage ratio of 1.20 to 1.25x. A property can appraise at a strong value and still fail to qualify if the income does not cover the debt payments with enough cushion. Calculate DSCR before approaching any lender.

Ignoring prepayment penalty structures

CRE loans commonly include yield maintenance or defeasance clauses. Selling or refinancing before the prepayment window closes can cost 2 to 5% of the remaining loan balance, turning what looks like a profitable exit into a costly one.

Applying personal credit standards to commercial underwriting

CRE lenders weigh property cash flow and asset quality more heavily than personal credit scores. A 750 credit score does not guarantee approval if the property's NOI is marginal. Conversely, strong property cash flow can offset a lower personal credit profile.

Commercial Real Estate Finance Council: establishes underwriting, reporting, and documentation standards for CRE debt markets

HR

Hassaan Rasheed

Developer and Researcher, CalculatorFlux

Researches and verifies the formulas, methodology, and source data behind each calculator on CalculatorFlux. All tools are built and checked against the cited references before publication.

Last updated: June 2026

Frequently Asked Questions

Most CRE loans have a 5, 7, or 10-year term with a balloon payment, while amortization runs 20 to 30 years. A common structure is 25-year amortization with a 10-year term. Monthly payments are calculated as if the loan runs 25 years, but the remaining balance is due at year 10, typically 75 to 85 percent of the original loan amount.

Match your loan term to your planned hold period. If you plan to sell in 7 years, use a 7-year term to avoid prepayment penalties. If you want to hold long-term, negotiate for a 10-year term to reduce refinancing risk.