What Is a Good IRR? Benchmarks by Asset Class (2026)

A good IRR means different things for real estate, private equity, and stocks. Hurdle rates, benchmarks by strategy, and when a high IRR misleads.

"Is 15% a good IRR?" depends entirely on what you are comparing it to. A 15% IRR on a stabilized apartment complex in a growing market is exceptional. A 15% IRR on an early-stage startup is a failure. The same number means something completely different depending on the risk profile, asset class, and what else you could do with that capital.

The IRR Calculator computes the exact IRR for any set of cash flows. This post covers what makes a specific IRR figure "good," the benchmarks that experienced investors actually use across real estate, private equity, and other asset classes, and the two situations where a high IRR is not what it appears to be.

What "Good" Actually Means: The Hurdle Rate Framework

The correct way to evaluate any IRR is against the hurdle rate, which is the minimum acceptable return given the risk of that specific investment.

The hurdle rate is your opportunity cost. If you can earn 10% in a comparable investment with similar risk, any project returning less than 10% is destroying value relative to your alternatives, regardless of whether 10% sounds high or low in isolation.

IRR > Hurdle Rate = Accept (investment adds value)

IRR = Hurdle Rate = Break-even (no net value created or destroyed)

IRR < Hurdle Rate = Reject (better alternatives exist)

The hurdle rate is not a universal fixed number. It shifts based on:

- Asset type: Core real estate carries lower risk than development, so it commands a lower hurdle rate

- Leverage: More debt amplifies equity IRR but also amplifies downside risk

- Liquidity: Illiquid investments like private equity and real estate demand a premium over liquid alternatives

- Market conditions: Base rates rising from 0.5% to 5.5% between 2021 and 2023 pushed hurdle rates across every asset class upward

This explains why the same investor might set different minimums for different deals in the same portfolio. A 14% hurdle for value-add multifamily and an 8% hurdle for a core office building are not contradictory; they reflect different risk levels requiring different compensation.

The question is never "is this IRR high?" It is: "does this IRR clear the hurdle for this specific risk profile?"

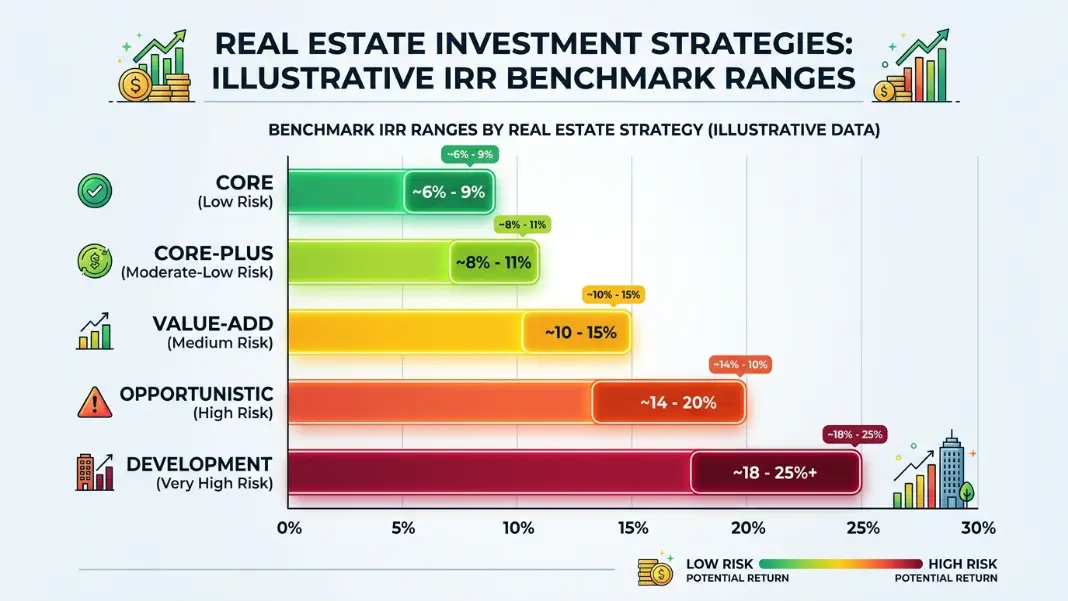

IRR Benchmarks for Real Estate by Strategy

Real estate IRR benchmarks vary significantly by investment strategy. The figures below represent general market expectations in 2026, using levered equity returns on equity deployed.

The table below shows target IRR ranges by real estate strategy and holding period.

| Strategy | Target IRR (Levered) | Typical Hold | Risk Level |

|---|---|---|---|

| Core (stabilized, Class A) | 8-12% | 7-10 years | Low |

| Core-Plus | 10-14% | 5-7 years | Low-Medium |

| Value-Add | 14-18% | 3-5 years | Medium |

| Opportunistic | 18-25%+ | 2-4 years | High |

| Ground-Up Development | 20-30%+ | 2-5 years | Very High |

| Single-Family Rental (SFR) | 10-16% | 5-10 years | Low-Medium |

A 12% IRR on a value-add apartment deal is not a success. The same 12% on a Class A stabilized office building in a primary market might be the best return available in that category. The strategy sets the expectation, not the number alone.

Why levered vs unlevered matters: Debt amplifies equity returns. A property generating a 6% unlevered return can produce a 14% levered IRR with the right financing structure. The Cap Rate vs IRR Guide covers how cap rate and IRR interact in a full deal model, including worked examples with debt service.

Rising interest rates between 2022 and 2024 compressed real estate IRRs significantly. Debt service costs rose while income yields stayed relatively flat, squeezing the spread that creates equity returns. Deals underwritten at 5% debt cost in 2021 have been remodeled at 7-8% in 2025-2026, raising the required income growth and exit assumptions to hit the same IRR target.

Private Equity and Venture Capital IRR Targets

Private equity funds set IRR targets before deploying capital, and these targets vary widely by fund type.

The figures below are gross IRR targets at the portfolio company level. Net IRR to limited partners, after management fees (typically 2%) and carried interest (typically 20%), runs 300 to 500 basis points lower. A fund targeting 25% gross IRR is delivering roughly 18-21% net to its LPs in a standard fee structure.

The table below shows gross and net IRR targets by PE strategy.

| Fund Type | Gross IRR Target | Net IRR Target | Fund Life |

|---|---|---|---|

| Large-Cap Buyout | 20-25% | 15-20% | 10-12 years |

| Mid-Market Buyout | 22-28% | 17-22% | 8-10 years |

| Growth Equity | 22-30% | 17-25% | 8-10 years |

| Venture Capital (early stage) | 30-40%+ | 25-35%+ | 10-15 years |

| Venture Capital (late stage) | 20-30% | 15-25% | 8-12 years |

| Infrastructure PE | 12-18% | 9-14% | 12-20 years |

Venture capital targets are higher because the expected loss rate is also higher. Early-stage VC funds anticipate that 50-60% of their portfolio companies return little or nothing. The few that work need to produce 10x-30x returns to drive a fund-level IRR in the 25-35% range.

Buyout funds work differently. They rely on financial engineering (debt), operational improvement, and multiple expansion across a diversified portfolio of established businesses. The return distribution is tighter and total losses are less common, which justifies lower targets compared to VC.

For a detailed breakdown of how gross and net IRR differ at the fund level, how the J-curve affects early performance reporting, and what DPI and TVPI mean alongside IRR, the Private Equity IRR Guide covers fund-level mechanics in full.

IRR Benchmarks Across Other Asset Classes

IRR is most useful for investments with defined cash flows over a specific period. For publicly traded assets, annualized total return serves the same function, and the S&P 500 long-run average is a useful baseline for every private investment comparison.

Public equities: The long-run historical average annual return from the S&P 500 is approximately 10% nominal, roughly 7% real after inflation. This is the relevant opportunity cost benchmark for any illiquid investment. An investment that returns 11% IRR over 10 years with your capital locked up is only marginally better than the public market on a percentage basis, without accounting for the illiquidity premium.

Investment-grade bonds: Current yields in 2026 range from 4-6% depending on duration and credit quality. High-yield bonds yield 6-9%. Fixed income IRR is essentially locked at issuance; there is no capital appreciation component unless you are trading interest rate duration.

Real assets (infrastructure, farmland, timberland): Core infrastructure targets 8-12% levered. Farmland typically delivers 5-8% unlevered with income plus appreciation, depending on commodity cycles.

Angel investing and early-stage startups: Target returns of 25-40%+ to account for the high failure rate. Cambridge Associates data suggests top-quartile venture funds deliver 15-25% net IRR over a 10-year fund life, though individual investment outcomes are extremely wide.

The S&P 500 baseline is the most practically useful benchmark for most situations. If a 15-year real estate hold produces a 10.5% IRR, and the public market delivered 11% over the same period with daily liquidity, the real estate deal barely compensated for its illiquidity risk. The illiquidity premium needs to be positive and meaningful, typically 200-400 basis points above liquid alternatives for the same risk level.

When a High IRR Is Not What It Seems

Two situations consistently produce IRR figures that look better than the underlying wealth creation warrants.

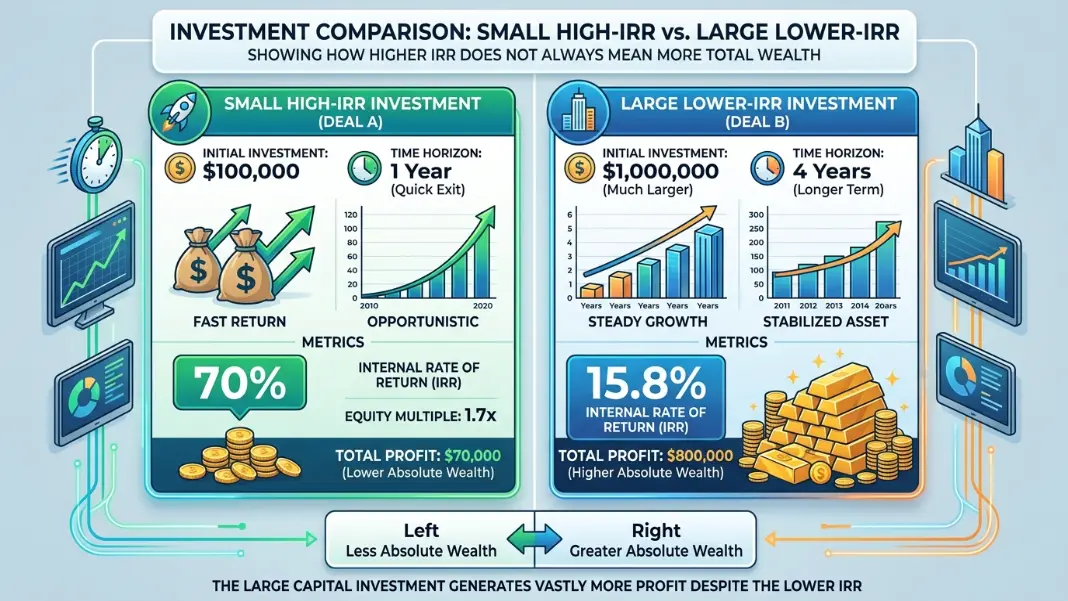

Short holding periods: IRR is sensitive to how quickly cash flows arrive. A deal that returns capital and profit in 18 months can produce a very high annualized IRR even if the absolute profit is small. A $100,000 investment that returns $115,000 in 12 months has an IRR of 15%. A $1,000,000 investment that returns $1,500,000 in 5 years has an IRR of 8.45%. The second deal created $400,000 more in actual wealth.

Small investment scale: A $20,000 investment at 40% IRR produces $8,000 in profit in one year. A $500,000 investment at 15% IRR produces $75,000. IRR ranks the small investment higher; your actual portfolio balance cares about the $75,000.

Comparing scale and time:

Example A: $20,000 invested, $28,000 returned in 1 year

IRR = 40%, Equity Multiple = 1.40x, Profit = $8,000

Example B: $500,000 invested, $750,000 returned over 5 years

IRR = 8.45%, Equity Multiple = 1.50x, Profit = $250,000

The equity multiple, which is total cash received divided by capital invested, tells you how many times over you got your money back independent of timing. A 2.5x equity multiple over 5 years means you received $2.50 for every dollar invested. That number does not fluctuate based on whether one distribution arrived in year 2 versus year 4.

When comparing investments, always check equity multiple alongside IRR. High IRR with a low equity multiple (like 1.2x over 2 years) indicates a short hold with limited absolute profit. Low IRR with a high equity multiple (like 2.8x over 8 years) indicates a long hold with substantial total wealth creation.

The IRR Calculator outputs IRR, equity multiple, and MIRR simultaneously on any cash flow series, so you can run all three checks without switching between tools.

A good real estate IRR depends on the strategy. Core stabilized properties target 8-12% levered, value-add projects target 14-18%, and opportunistic or development deals target 18-25% or higher. In each case, "good" means the IRR exceeds the hurdle rate for that specific risk level. A 12% IRR on a core deal is strong; a 12% IRR on a ground-up development project falls short of market expectations for that risk.

Buyout funds target 20-25% gross IRR, delivering 15-20% net to limited partners after fees. Venture capital targets 30-40%+ gross at the early stage to account for high failure rates across the portfolio. Infrastructure PE targets 12-18% gross. These are fund-level targets, not individual deal expectations. Net IRR, after management fees and carried interest, runs 300-500 basis points below gross IRR depending on fund performance.

A 20% IRR is strong in most contexts. It exceeds the long-run S&P 500 average of about 10%, covers a typical private equity hurdle rate, and represents solid performance in value-add real estate. Whether 20% is sufficient depends on the risk profile. A 20% IRR on a ground-up development in an uncertain market may not compensate for the risk. A 20% IRR on a well-underwritten, cash-flowing asset with stable tenants is excellent by any standard.

IRR is the actual return rate embedded in an investment's cash flows. Hurdle rate is the minimum acceptable return you require for that investment given its risk. If IRR exceeds the hurdle rate, the investment adds value and should be accepted. If IRR falls below the hurdle rate, better alternatives exist for that capital. The hurdle rate is your benchmark; IRR is what the deal actually delivers. The comparison between the two drives the accept-or-reject decision.

For a buy-and-hold single-family rental, 10-16% levered IRR is the target range in most markets. For stabilized multifamily, 8-12% is typical. These benchmarks assume standard leverage (25-30% down payment), a 5-10 year hold, and realistic exit cap rate assumptions. The relevant comparison is not just the target percentage but also the entry cap rate relative to your financing cost. The IRR and Cap Rate calculators used together model this relationship.

Yes. Two situations produce inflated IRR figures. First, short holding periods: returning capital quickly produces high annualized rates even when absolute profit is small. A 40% IRR on a $50,000 investment returned in one year creates $20,000. Second, small investment scale: the same 40% IRR on $50,000 creates far less wealth than a 15% IRR on $1,000,000. Always check equity multiple (total return divided by capital invested) alongside IRR to confirm the percentage is translating into meaningful absolute returns.

Written by

Hassaan Rasheed

Web Developer & Content Researcher

Hassaan builds calculators and writes research-backed guides on finance, math, payroll, and construction topics. Every number in his articles is sourced from official data and worked through by hand.

View LinkedIn Profile