How to Calculate Internal Rate of Return: IRR Formula and Examples (2026)

IRR is the discount rate that makes an investment's NPV equal zero. Formula, worked examples, MIRR correction, and when IRR misleads.

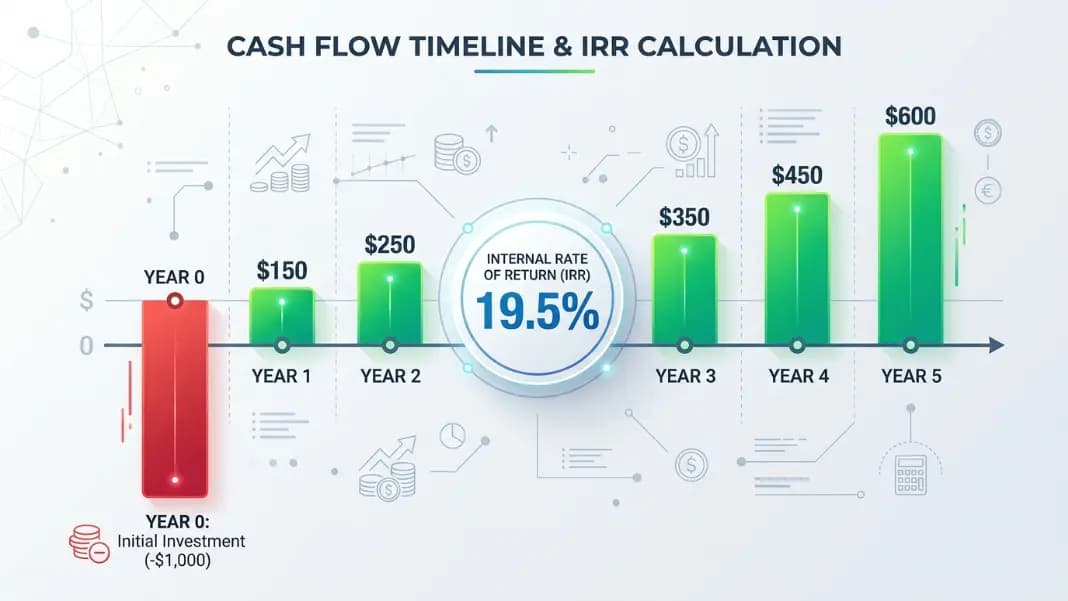

IRR answers one question: what annualized return are you getting on the cash you actually put in, accounting for every cash flow and its timing? It does not require an assumed discount rate as an input. The calculation finds the rate automatically, which is why it appears on every investor's checklist and why financial calculators have a dedicated key for it.

The IRR Calculator runs this calculation for you. This guide explains the formula, works through a real estate example, covers where IRR produces misleading results, and explains when Modified IRR (MIRR) gives a more honest number.

How to Calculate IRR

IRR is the discount rate (r) that satisfies this equation:

0 = CF0 + CF1/(1+r)^1 + CF2/(1+r)^2 + ... + CFn/(1+r)^n

CF0 is typically a negative number (your initial investment). The remaining cash flows are what you receive over time.

There is no algebraic closed-form solution for r. You solve it iteratively: try a rate, see if the equation sums to zero, adjust, repeat. Financial calculators and spreadsheets (Excel's =IRR() function) do this automatically using Newton-Raphson iteration.

Worked example: rental property purchase

- Year 0: -$250,000 (down payment plus closing costs)

- Year 1: +$18,000 (net rental income after all expenses, no debt service)

- Year 2: +$18,500

- Year 3: +$19,000

- Year 4: +$19,500

- Year 5: +$19,500 operating income plus $310,000 sale proceeds = +$329,500

Plugging into the formula and solving iteratively:

- At 12%: NPV = +$9,241 (rate too low, need to try higher)

- At 15%: NPV = -$8,114 (rate too high)

- At 13.4%: NPV is approximately $0

IRR = 13.4%

That is the annualized return on $250,000 over 5 years, inclusive of all cash flows and the exit proceeds.

IRR vs NPV: Which One to Trust

IRR and NPV come from the same discounted cash flow framework but answer different questions.

NPV asks: if my required return is X%, how much value does this investment create in today's dollars? It produces a dollar amount.

IRR asks: what return does this investment actually produce? It produces a percentage, which makes it easy to compare investments of different sizes.

| NPV | IRR | |

|---|---|---|

| Output | Dollar value | Percentage return |

| Requires assumed discount rate | Yes | No |

| Easy to compare across different sizes | Less intuitive | Yes |

| Handles unconventional cash flows | Always works | Sometimes breaks |

| Best use case | Go/no-go capital decisions | Ranking competing investments |

For a single investment decision, both methods agree. If NPV is positive at your required return, IRR will be above that required return.

Where they disagree: when comparing a $100K investment at 20% IRR versus a $1M investment at 15% IRR. IRR says the first is better. NPV shows the second creates more total value (assuming you have the capital). Always check the absolute NPV alongside IRR when comparing investments of different scales.

The Cap Rate Calculator handles the unleveraged income yield side of the same analysis.

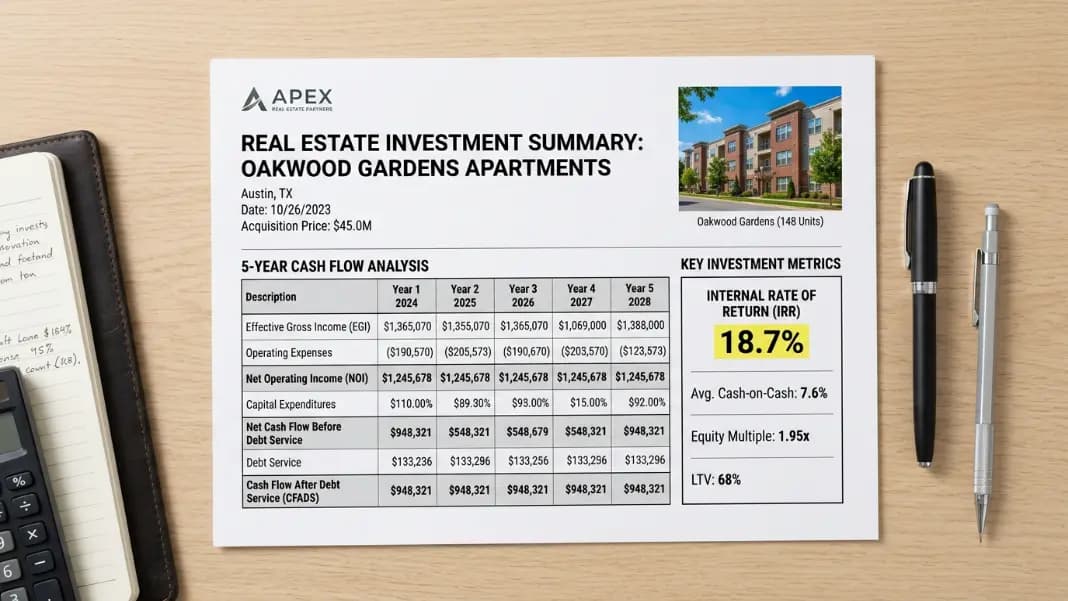

IRR for Rental Property: A Realistic Example

Real estate IRR calculations include debt service, appreciation, and a sale event, which is where the return story gets interesting.

Assumptions:

- Purchase price: $500,000

- Down payment (25%): $125,000

- Loan: $375,000 at 7.25%, 25-year amortization

- Monthly rental income: $3,800 in Year 1, growing 2.5% per year

- Operating expenses: 35% of gross income

- Holding period: 7 years

- Exit cap rate at sale: 6.5%

Simplified year-by-year cash flows:

| Year | NOI | Debt Service | Cash Flow |

|---|---|---|---|

| 0 | -$125,000 | ||

| 1 | $29,640 | $32,484 | -$2,844 |

| 2 | $30,381 | $32,484 | -$2,103 |

| 3 | $31,141 | $32,484 | -$1,343 |

| 4 | $31,919 | $32,484 | -$565 |

| 5 | $32,717 | $32,484 | +$233 |

| 6 | $33,535 | $32,484 | +$1,051 |

| 7 | $34,373 + sale | $32,484 | +$190,700 |

NOI in Year 7: $34,373. At a 6.5% exit cap rate, sale price = $34,373 / 0.065 = $528,815. Remaining loan balance after 7 years: approximately $325,000. Net to equity after $15,000 closing costs: $188,815. Year 7 total cash flow: roughly $190,700.

IRR on the $125,000 equity invested: approximately 11.2%

The equity return is meaningfully higher than the unleveraged cap rate (5.9%) because the loan amplifies the equity return while appreciation builds equity over 7 years. This is the core case for leverage in real estate investing.

When IRR Gives Misleading Results

IRR breaks down in two specific situations worth knowing.

Multiple IRRs: If the cash flow stream changes sign more than once (negative, then positive, then negative again), the IRR equation can have multiple valid mathematical solutions. A project with a large cleanup or remediation cost in a final year after years of positive income might produce two IRRs: 8% and 22%. Neither is definitively correct. In this case, use NPV with a specified discount rate instead.

Scale differences: IRR ignores the size of the investment. A $10,000 investment at 40% IRR generates $4,000 in profit. A $1,000,000 investment at 15% IRR generates $150,000. IRR ranks the first project higher; actual wealth creation says the second is better. Always check absolute NPV alongside IRR when project sizes differ significantly.

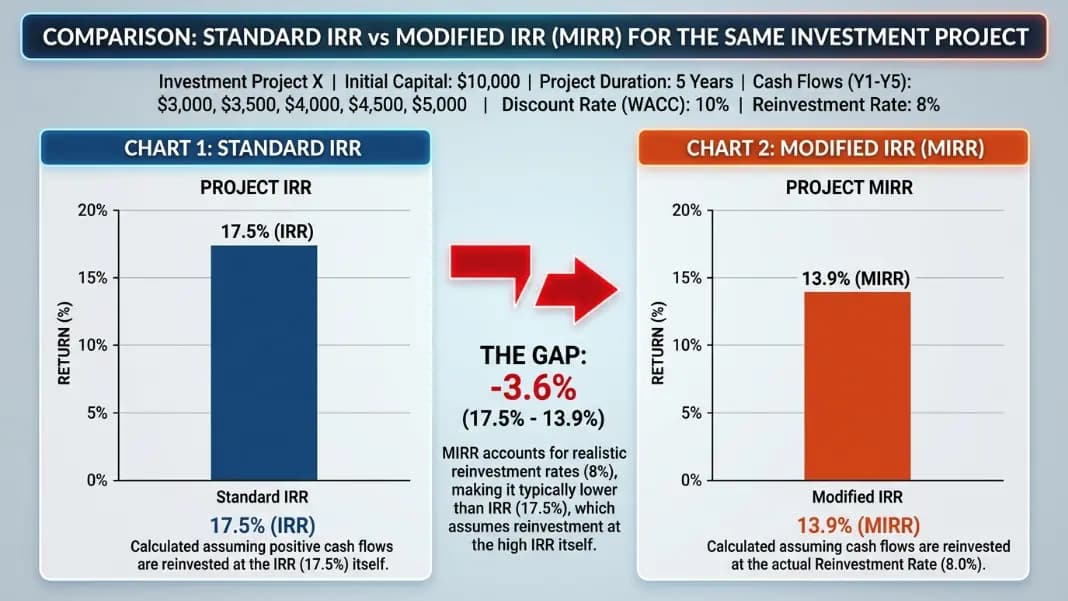

The reinvestment rate assumption: Standard IRR implicitly assumes every intermediate cash flow is reinvested at the IRR rate itself. If your IRR is 20%, the formula assumes you can reinvest annual distributions at 20% indefinitely. In most markets, that assumption is too optimistic. This inflates the apparent IRR compared to what the investment actually delivers.

Modified IRR: A More Realistic Measure

MIRR fixes the reinvestment assumption by letting you specify two separate rates: a finance rate for negative cash flows (your cost of capital) and a reinvestment rate for positive cash flows (where you realistically deploy the returns).

MIRR = (FV of positive cash flows at reinvestment rate /

PV of negative cash flows at finance rate)^(1/n) - 1

Example using the rental property above:

- Finance rate (cost of capital): 7%

- Reinvestment rate (expected return on reinvested proceeds): 5%

- n = 7 years

With these conservative assumptions, MIRR comes out to approximately 9.4% versus the standard IRR of 11.2%.

The difference matters for investment decisions. If your hurdle rate is 10%, standard IRR clears it and the project looks acceptable. MIRR at 9.4% falls below the hurdle. The two metrics lead to different conclusions for the same investment.

Excel's =MIRR() function takes three arguments: the cash flow range, the finance rate, and the reinvestment rate. Use it when comparing projects with large intermediate cash flows or when your standard IRR is well above realistic reinvestment opportunities.

For the benchmarks that define what a calculated IRR should clear by asset class and strategy, the What Is a Good IRR Guide covers targets from core real estate through venture capital, with the hurdle rate framework for evaluating any specific number.

IRR is the discount rate r that makes the sum of discounted cash flows equal zero: 0 = CF0 + CF1/(1+r)^1 + CF2/(1+r)^2 + ... + CFn/(1+r)^n. There is no closed-form solution, so it requires iterative numerical methods. Excel's =IRR() function handles this automatically given a range of cash flows. On a financial calculator, enter your cash flows into the CF register and press the IRR key.

Hurdle rates vary by property type and risk, but common benchmarks are: 7-10% for core (stabilized, low-risk) real estate; 12-18% for value-add projects; 18-25% or higher for opportunistic and development deals. These are levered returns on equity. An unlevered IRR 200-300 basis points below the levered target is normal when financing is used. IRR expectations have shifted upward since 2022 as base rates rose.

On an HP 12C: enter your initial investment as a negative CF0 using the g CFo key, then enter each subsequent cash flow using g CFj. Press f IRR to compute. On a BA II Plus: use the CF worksheet, enter CF0, then C01, F01 for each cash flow and frequency. Press IRR then CPT. Make sure the initial investment is entered as a negative number. If it is entered as positive, the calculator returns no valid solution.

NPV gives a dollar value: how much wealth an investment creates in today's dollars given an assumed discount rate. IRR gives a percentage: the actual return rate embedded in the cash flows without any assumed rate. NPV requires you to specify your discount rate first. Both agree on whether a single investment should be accepted or rejected, but they can rank competing investments differently when those investments differ in size or cash flow timing.

IRR has a unique solution only when the cash flow stream changes sign once, typically negative at the start and positive after. When cash flows change sign more than once (a large negative cash flow late in the project after years of positive flows), the IRR equation can have multiple mathematical roots. When this happens, standard IRR is unreliable. NPV with a stated discount rate, or MIRR, are the correct alternatives.

Modified IRR (MIRR) corrects the standard IRR assumption that intermediate cash flows are reinvested at the IRR rate itself. MIRR lets you specify a realistic reinvestment rate (typically 5-8%, matching expected market returns) and a separate finance rate (your cost of capital). MIRR is almost always lower than standard IRR for the same cash flow stream. Use it when comparing projects with significant intermediate distributions, or whenever your standard IRR is well above realistic reinvestment rates.

Written by

Hassaan Rasheed

Web Developer & Content Researcher

Hassaan builds calculators and writes research-backed guides on finance, math, payroll, and construction topics. Every number in his articles is sourced from official data and worked through by hand.

View LinkedIn Profile