NE, MN, UT, MT Paycheck Tax Guide 2025-26

Side-by-side take-home pay at $50K, $75K, $100K plus Montana's 2024 reform and Utah's credit advantage.

11 min readRead →

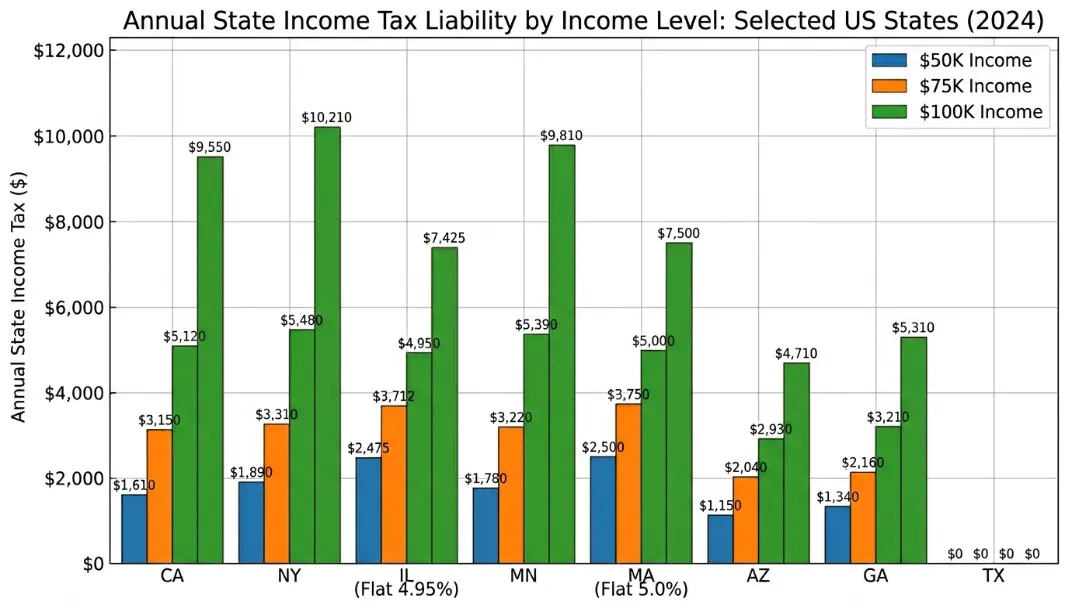

Minnesota has the highest state income tax rate in the Midwest at 9.85%on income above $183,340 (single). Even in the lower brackets, Minnesota tax runs higher than neighboring states. Ohio's effective tax on a $100,000 salary is just $2,034, Minnesota's is $5,371. The gap widens as income rises, with a $200,000 earner paying roughly $12,700 more per year in Minnesota than in Ohio.

| Annual Salary | MN State Tax | Ohio State Tax | Colorado (4.40%) | MN Eff. Rate | MN vs OH Extra |

|---|---|---|---|---|---|

| $50,000 | $1,971 | $676 | $1,518 | 3.9% | +$1,295/yr |

| $65,000 | $2,991 | $1,071 | $2,218 | 4.6% | +$1,920/yr |

| $85,000 | $4,351 | $1,621 | $3,098 | 5.1% | +$2,730/yr |

| $100,000 | $5,371 | $2,034 | $3,758 | 5.4% | +$3,337/yr |

| $150,000 | $9,156 | $3,784 | $5,958 | 6.1% | +$5,372/yr |

| $200,000 | $14,082 | $5,284 | $8,158 | 7.0% | +$8,798/yr |

Single filers, no pre-tax deductions. Ohio applies its rate to gross wages; Minnesota and Colorado apply to income after the $14,600 standard deduction. Ohio effective rate at $200K includes 2.75% + 3.50% brackets.

Minnesota follows federal 401(k) treatment, traditional pre-tax contributions lower your Minnesota taxable income. Ohio does not give this benefit; Ohio taxes gross wages regardless of 401(k) contributions. In Minnesota, every dollar in a pre-tax 401(k) saves you both federal income tax and Minnesota state tax simultaneously. At the 6.80% Minnesota bracket, a $5,000 contribution saves $340 in state tax alone. At the top 9.85% bracket, the same $5,000 saves $493.

| Annual Salary | 6% Contribution | MN Bracket Hit | MN Tax Saved | Federal Tax Saved | Total Annual Savings |

|---|---|---|---|---|---|

| $50,000 | $3,000 | 6.80% | $204 | $360 | $564 |

| $65,000 | $3,900 | 6.80% | $265 | $468 | $733 |

| $100,000 | $6,000 | 6.80% | $408 | $1,320 | $1,728 |

| $120,000 | $7,200 | 7.85% | $559 | $1,584 | $2,143 |

| $150,000 | $9,000 | 7.85% | $707 | $2,160 | $2,867 |

| $200,000 | $12,000 | 9.85% | $1,182 | $2,880 | $4,062 |

Single filers. Federal savings based on marginal federal bracket at each income level. MN savings calculated at the marginal MN bracket the contribution falls into. Contribution capped at $23,500 (2025 IRS limit).

Minnesota taxes income progressively, meaning only the portion of your taxable income that falls within each bracket gets taxed at that rate. No one pays 9.85% on their entire salary. At $100,000 single, the effective Minnesota rate is just 5.4% because the first $30,070 of taxable income is taxed at only 5.35%. The brackets apply after subtracting the $14,600 standard deduction for single filers.

| Bracket | Taxable Income Range (Single) | Rate | Who It Hits |

|---|---|---|---|

| 1st | $0–$30,070 | 5.35% | Salaries up to ~$44,670 gross |

| 2nd | $30,071–$98,760 | 6.80% | Most full-time workers |

| 3rd | $98,761–$183,340 | 7.85% | Gross above ~$113,360 |

| 4th | Above $183,340 | 9.85% | Gross above ~$197,940 |

Married filers have wider brackets: 5.35% extends to $43,950 and 6.80% to $174,610, which substantially lowers the tax bill for dual-income households compared to filing separately. Pre-tax 401(k) contributions reduce your taxable income, pushing you into a lower bracket. Use the 401(k) calculator to see exactly how contributions change your bracket position.

At $60,000, a single Minnesota filer keeps about $47,550 after all taxes, or $3,963 per month. Federal income tax takes the largest chunk at $5,209 (8.7% of gross). Minnesota state tax adds $2,651 at a 4.4% effective rate, and FICA (Social Security plus Medicare) accounts for another 7.65%. The table below shows take-home at common salary levels.

| Annual Salary | Federal Tax | MN State Tax | Social Security | Medicare | Annual Take-Home | Monthly Take-Home |

|---|---|---|---|---|---|---|

| $50,000 | $4,010 | $1,971 | $3,100 | $725 | $40,194 | $3,349 |

| $60,000 | $5,209 | $2,651 | $3,720 | $870 | $47,550 | $3,963 |

| $65,000 | $5,810 | $2,991 | $4,030 | $943 | $51,226 | $4,269 |

| $75,000 | $8,202 | $3,671 | $4,650 | $1,088 | $57,389 | $4,782 |

| $100,000 | $13,703 | $5,371 | $6,200 | $1,450 | $73,276 | $6,106 |

Single filers, no pre-tax deductions. Uses 2025 federal brackets and $14,600 standard deduction. MN state tax based on 2025 progressive brackets. Highlighted row is the $60,000 reference. Figures rounded to the nearest dollar.

Minnesota is one of only nine states that taxes Social Security benefits at the state level, but it provides a subtraction that shields most retirees. Single filers with adjusted gross income below roughly $105,380 can subtract most or all Social Security income from Minnesota taxable income. Married filers have a higher threshold of approximately $134,500. For working-age residents receiving only W-2 wages, this subtraction has no effect on your paycheck calculations.

Above those thresholds, the subtraction phases out. A Minnesotan with $120,000 in combined income (Social Security plus pension or investment income) would owe state tax on a portion of their benefits. This makes late-career income planning more complex in Minnesota than in states like Illinois, which fully exempts retirement income from state tax.

For overtime pay and supplemental wages, Minnesota applies the same progressive brackets, not a flat withholding rate. This is different from how some states handle bonuses. If you earn overtime regularly, the time and a half calculator can help estimate your gross before entering it here.

Most Minnesota workers earning under $113,000 single ($128,000 married) never hit the 7.85% or 9.85% bracket. The majority of your taxable income falls into the 5.35% and 6.80% ranges. Enter your 401(k) contribution to see how pre-tax savings shift you to a lower effective rate.

In-depth guides related to this calculator.