Massachusetts Paycheck Calculator: Flat Tax, PFML, and Take-Home Pay (2026)

Massachusetts paycheck calculator: 5% flat state income tax, mandatory PFML withholding, and no city tax. Take-home at $60K, $80K, $120K. Free, no signup.

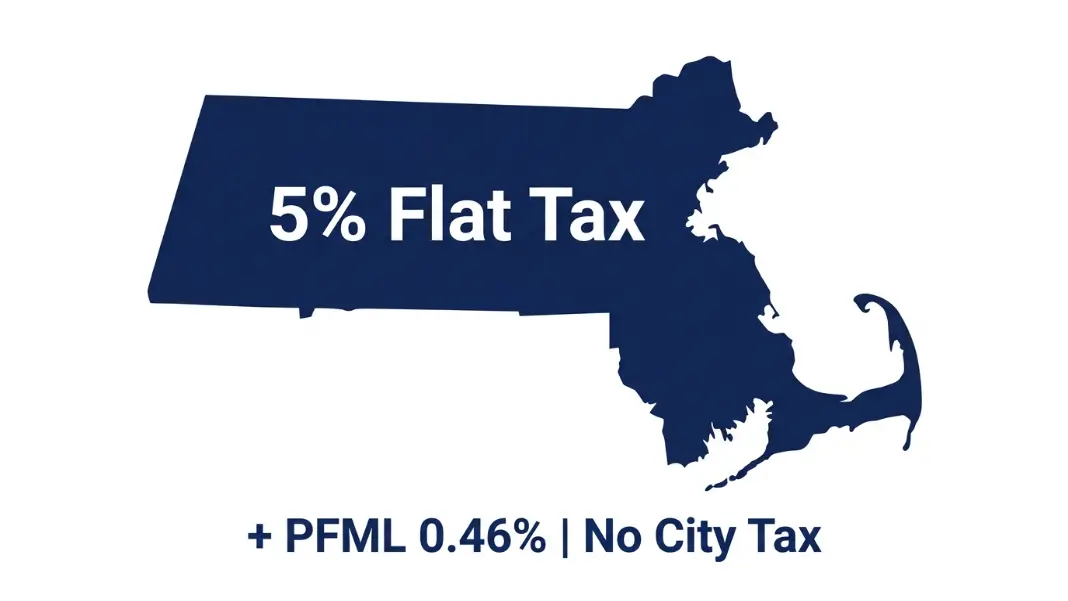

Massachusetts has a reputation as a high-tax state, but the nickname does not hold up at the paycheck level for most W-2 earners. The 5% flat income tax rate is lower than Connecticut's top rate, lower than New York's middle brackets, and far below what residents in California or New Jersey pay. The surprise on a Massachusetts pay stub is not the income tax line. It is the PFML deduction: a mandatory contribution most new employees do not recognize when they see it for the first time.

The Massachusetts Paycheck Calculator computes take-home for any salary with the correct PFML rate, personal exemption, and the Millionaires' Tax surcharge where applicable. This guide explains what each deduction line represents and what actually drives the difference between gross pay and net pay for Massachusetts workers.

Massachusetts Income Tax: Flat Rate, Personal Exemption, and the Millionaires' Tax

Massachusetts taxes most earned income at a flat 5% rate. Unlike progressive states where the rate increases with each bracket, every dollar of wages above the personal exemption is taxed at the same 5% in Massachusetts.

Before applying the rate, a personal exemption reduces your taxable income. This is not a deduction in the federal sense; it is a fixed amount that reduces the income subject to state tax.

| Filing Status | Personal Exemption |

|---|---|

| Single | $4,400 |

| Married Filing Jointly | $8,800 |

| Head of Household | $6,800 |

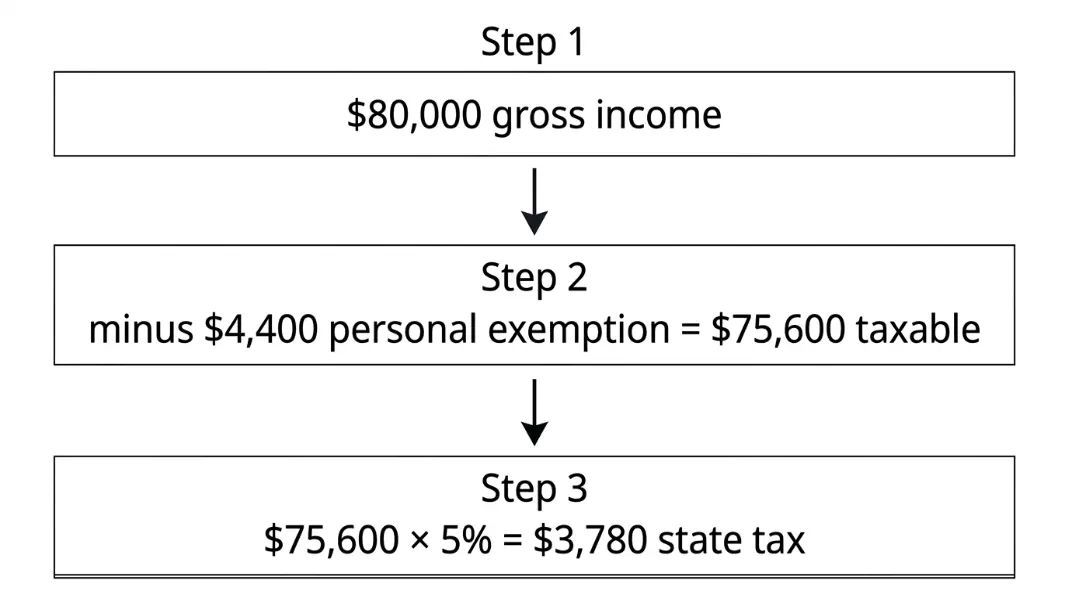

Massachusetts income tax on an $80,000 salary (single):

Gross income: $80,000

Less personal exemption: -$4,400

Massachusetts taxable income: $75,600

Tax at 5%: $75,600 × 0.05 = $3,780

The Millionaires' Tax:

Effective January 1, 2023, Massachusetts added a 4% surcharge on income above $1,000,000 under the Fair Share Amendment. This makes the effective Massachusetts rate 9% on income above that threshold. For the large majority of W-2 workers, the 5% flat rate applies to all income. The surcharge primarily affects high-compensation executives, physicians, and financial professionals in Boston whose cash compensation crosses seven figures.

What Massachusetts does not tax:

Social Security income is exempt from Massachusetts income tax. Pension income from the Massachusetts teachers' retirement system and state employee pension system is also exempt. Most W-2 workers are not affected by these exemptions, but they are significant for older employees drawing pension income alongside wages.

PFML Contributions: The Deduction Most New Employees Do Not Recognize

Paid Family and Medical Leave (PFML) is a Massachusetts state program that funds paid leave for qualifying life events: bonding with a newborn or newly adopted child, caring for a seriously ill family member, or recovering from a personal serious health condition.

Every Massachusetts employee contributes to PFML through payroll withholding. This is mandatory and appears as a separate line item on the pay stub, usually labeled "MA PFML" or "Massachusetts Paid Leave."

2025 PFML contribution rates:

The total PFML program rate in 2025 is 0.88% of wages, split between family leave and medical leave.

For employers with 25 or more employees, the employer is required to pay a portion. The employee's share is 0.46% of gross wages.

For employers with fewer than 25 employees, the employer is exempt from contributing, but the employee still pays 0.46%.

PFML on an $80,000 salary:

Annual PFML contribution: $80,000 × 0.46% = $368

Per biweekly paycheck: $368 / 26 = $14.15

PFML contributions stop once wages cross the Social Security wage base ($176,100 in 2025). High earners stop having PFML withheld once their year-to-date wages cross that threshold mid-year, which slightly increases take-home in the back half of the calendar year.

Why it looks unfamiliar:

PFML is not a tax; it is a social insurance contribution, similar to FICA in structure. Unlike state income tax, it does not appear on the W-2 in the state tax box. It appears in Box 14 as a separate labeled item. This placement causes confusion at tax filing time: PFML contributions are not deductible on the federal return in most cases, and they are not a credit against Massachusetts income tax.

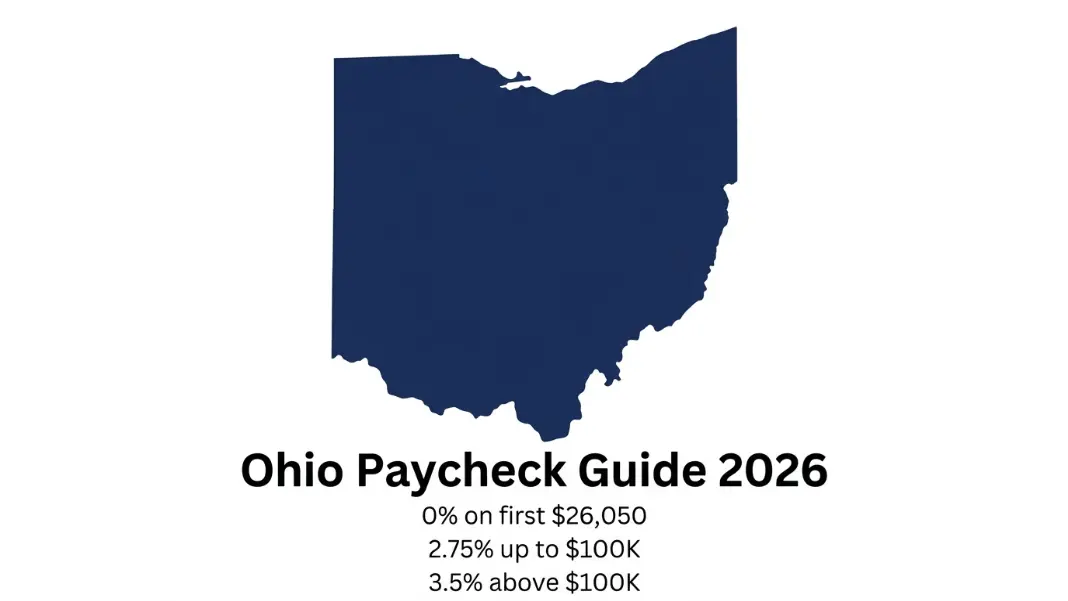

For a comparison of how payroll deductions work in a state with no PFML equivalent, the Ohio Paycheck Calculator Guide shows how Ohio handles state, school district, and municipal withholding without any paid leave program contribution.

Massachusetts Take-Home Pay at $60K, $80K, and $120K

Three scenarios for a single filer, one exemption, employer with 25 or more employees, biweekly payroll:

| Gross Salary | Federal Tax | FICA | MA State Tax | MA PFML | Take-Home | Effective Rate |

|---|---|---|---|---|---|---|

| $60,000 | $6,294 | $4,590 | $2,780 | $276 | $46,060 | 23.2% |

| $80,000 | $10,294 | $6,120 | $3,780 | $368 | $59,438 | 25.7% |

| $120,000 | $19,094 | $9,180 | $5,780 | $552 | $85,394 | 28.8% |

Note: federal tax is approximate and assumes standard W-4 with no pre-tax deductions. Actual take-home increases with 401k contributions, health insurance premiums, FSA contributions, or commuter benefit elections, all of which reduce federal and Massachusetts taxable income.

The New York Paycheck Calculator shows how New York state's progressive brackets and New York City's local tax add up by comparison. At $80,000 in New York City, state and city taxes combined approach $8,000 versus Massachusetts's $3,780 at the same income.

Does Your City or Town Affect Your Massachusetts Paycheck?

Massachusetts does not allow cities or towns to levy their own income tax. Boston, Worcester, Cambridge, Springfield: none of them add a local tax line to your paycheck. This is a significant difference from Ohio, Pennsylvania, and New York, where city income taxes add 1% to 3.8% depending on the municipality.

Every Massachusetts W-2 employee in the state pays the same state income tax rate and the same PFML rate regardless of where they work. The only location variable that affects your take-home pay is whether your employer has 25 or more employees, which affects the PFML share but not the income tax.

The exception for nonresidents:

If you live outside Massachusetts but work within the state, you owe Massachusetts income tax on wages earned in Massachusetts. New Hampshire residents who commute to Boston represent the largest group affected. New Hampshire has no income tax on wages, so every dollar earned in Massachusetts is taxed only in Massachusetts at 5%. Rhode Island and Connecticut residents working in Massachusetts owe Massachusetts tax on those wages and typically receive a credit in their home state to avoid double taxation, depending on reciprocity agreements.

Massachusetts vs Connecticut and New York: Where the Rates Land

Massachusetts sits in the lower-middle range of New England and Northeast state income tax rates.

| State | Top Rate | Rate Structure | Local Income Tax |

|---|---|---|---|

| Massachusetts | 5% (9% over $1M) | Flat below $1M | None |

| Connecticut | 6.99% | Progressive, 7 brackets | None |

| Rhode Island | 5.99% | Progressive, 3 brackets | None |

| New York | 10.9% | Progressive, 9 brackets | NYC adds up to 3.876% |

| New Hampshire | 0% on wages | No wage income tax | None |

| Vermont | 8.75% | Progressive, 4 brackets | None |

| Maine | 7.15% | Progressive, 3 brackets | None |

Connecticut has no city income tax, like Massachusetts, but its top marginal rate of 6.99% kicks in at much lower income levels. At $150,000 for a single filer, Connecticut's effective state rate is approximately 5.8% versus Massachusetts's 5% flat. The gap widens above $500,000 where Connecticut's top bracket applies.

New Hampshire's 0% rate on wages is the reason for the significant commuter population along the Massachusetts-New Hampshire border. Manchester and Nashua residents who work in Boston keep their Massachusetts wages but pay no income tax on them to New Hampshire. The offset is New Hampshire's property tax, which is among the highest in the country.

For Massachusetts residents building toward retirement, the Roth IRA Contribution Calculator shows your maximum allowable contribution for 2026 based on MAGI. The phase-out for single filers starts at $150,000, which is relevant for Massachusetts professionals in Boston's finance and life sciences sectors who may find their Roth eligibility reduced or eliminated.

Massachusetts applies a flat 5% income tax rate to taxable income. Single filers reduce gross income by a $4,400 personal exemption before applying the rate. On an $80,000 salary, that gives taxable income of $75,600 and annual state tax of $3,780. An additional 4% surcharge applies to income over $1,000,000 under the Millionaires' Tax. The Massachusetts Paycheck Calculator shows exact per-paycheck withholding for any salary and filing status.

Massachusetts PFML (Paid Family and Medical Leave) is a mandatory payroll contribution funding the state's paid leave program. In 2025, employees at companies with 25 or more employees pay 0.46% of gross wages. On a $60,000 salary, that is $276 per year, or about $10.62 per biweekly paycheck. It appears as a separate line on the pay stub labeled "MA PFML" or similar. Contributions stop once wages exceed the Social Security wage base. PFML is not a tax and appears in Box 14 of the W-2, not the state tax box.

No. Massachusetts does not allow cities or towns to impose local income taxes. Every Massachusetts employee pays the same 5% flat state rate regardless of whether they work in Boston, Worcester, Springfield, or a small town. This is a meaningful difference from states like Ohio, Pennsylvania, and New York, where city income taxes add 1.8% to 3.876% on top of state withholding. Boston has no additional local payroll tax beyond what the state requires.

Massachusetts allows a personal exemption of $4,400 for single filers, $8,800 for married filing jointly, and $6,800 for head of household. This amount reduces your gross income before the 5% state tax rate is applied. A single filer earning $80,000 subtracts $4,400 and pays tax on $75,600. The exemption is a fixed dollar amount and does not phase out at higher incomes, unlike the federal personal exemption. Massachusetts uses the exemption system rather than a standard deduction in the federal sense.

Massachusetts taxes most income at a flat 5%. Connecticut uses 7 progressive brackets from 2% to 6.99%. For W-2 earners between $60,000 and $200,000, the effective rates are close: a Connecticut single filer at $100,000 owes approximately $4,500 in state tax, while a Massachusetts single filer at the same income owes approximately $4,780 (after personal exemption). Above $250,000, Connecticut's rate structure accelerates faster than Massachusetts's flat 5%, making Massachusetts comparatively less expensive at higher incomes.

Yes, if they earn wages in Massachusetts. Massachusetts taxes income earned within its borders regardless of where the employee lives. New Hampshire residents commuting to work in Massachusetts owe Massachusetts income tax at 5% on those wages. New Hampshire has no income tax on wages, so there is no home-state credit to offset the Massachusetts tax. The same principle applies to Connecticut, Rhode Island, and Vermont residents working in Massachusetts, though those states typically provide a credit for taxes paid to Massachusetts to avoid double taxation.

Written by

Hassaan Rasheed

Web Developer & Content Researcher

Hassaan builds calculators and writes research-backed guides on finance, math, payroll, and construction topics. Every number in his articles is sourced from official data and worked through by hand.

View LinkedIn Profile