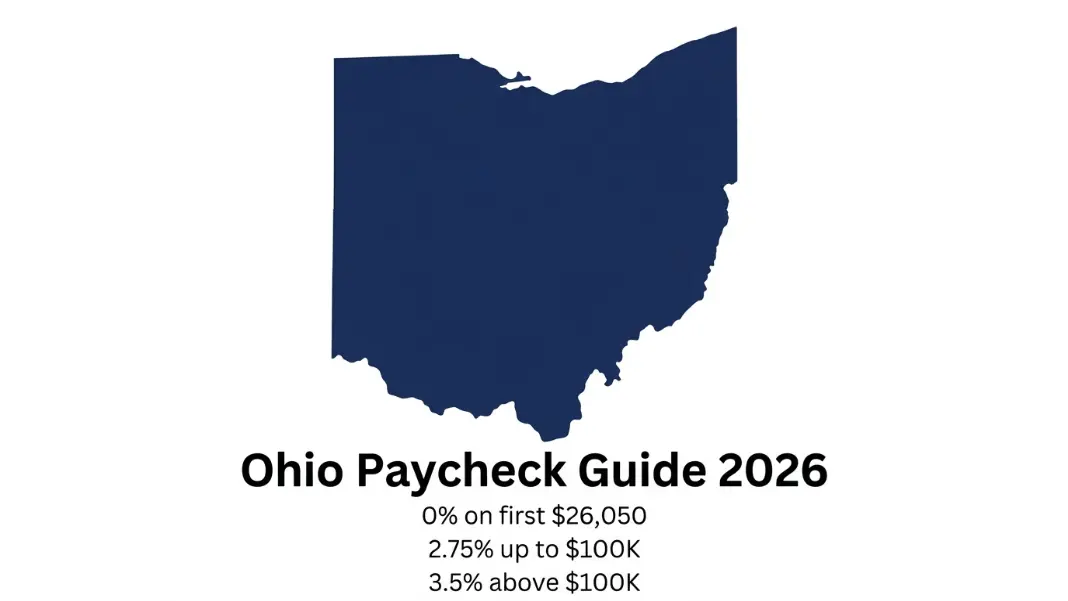

Ohio Paycheck Calculator: Tax Rates, SDIT, and Take-Home Pay (2026)

Ohio paycheck calculator: 0% state tax on first $26,050, then 2.75% to 3.5%. School district income tax and city tax explained. Take-home at $50K-$100K.

Ohio employees often notice their state income tax withholding is the lowest among Midwest colleagues earning similar salaries. That is not a payroll error. Ohio applies a 0% rate to the first $26,050 of taxable income, which means a significant portion of most workers' wages is untouched by state income tax entirely. The brackets above that floor top out at 3.5%, well below the 4.95% flat rate in Illinois or the 4.25% flat rate in Michigan.

The Ohio Paycheck Calculator shows your exact take-home for any salary and filing status, including municipal and school district taxes. This guide covers how Ohio's two-tier rate structure works, the school district income tax that surprises new residents, and how city taxes in Columbus, Cleveland, and Cincinnati affect take-home differently depending on where you live and work.

Ohio's Tax Structure: The Zero-Rate Floor and What Comes After

Ohio's state income tax for 2025-26 has a zero-rate bracket that makes it structurally different from most states.

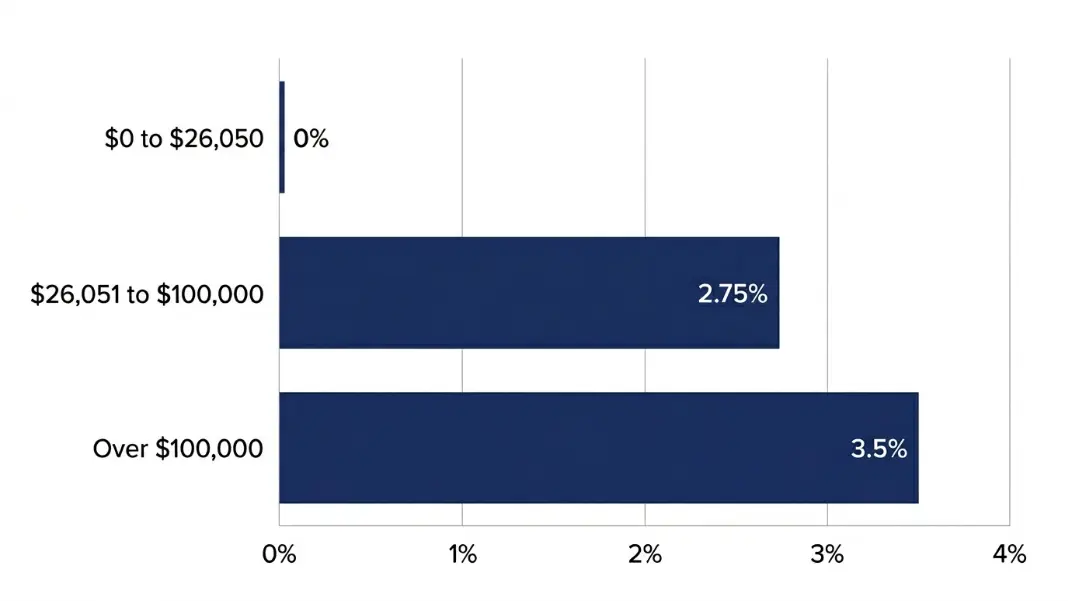

Ohio 2025-26 state income tax brackets (single filer):

| Taxable Income | Rate |

|---|---|

| Up to $26,050 | 0% |

| $26,051 to $100,000 | 2.75% |

| Over $100,000 | 3.5% |

Ohio also provides a personal exemption credit of $20 per taxpayer and each dependent. This reduces the tax owed directly, not taxable income, and applies after the brackets are calculated.

Tax at different income levels for a single filer with no dependents:

For $75,000 gross:

Tax on $0 to $26,050: $0

Tax on $26,050 to $75,000 = $48,950 × 2.75%: $1,346

Less personal exemption credit: -$20

Ohio state income tax: $1,326

Effective Ohio rate on $75,000: 1.77%

For $120,000 gross:

Tax on $0 to $26,050: $0

Tax on $26,050 to $100,000 = $73,950 × 2.75%: $2,034

Tax on $100,001 to $120,000 = $20,000 × 3.5%: $700

Less personal exemption credit: -$20

Ohio state income tax: $2,714

Effective Ohio rate on $120,000: 2.26%

The low effective rate is the result of the zero floor combined with relatively modest rates in the middle bracket. Ohio's effective rate compares favorably to every neighboring state for W-2 earners in the $50,000 to $150,000 range.

Ohio-specific deductions worth knowing:

Ohio allows a deduction for contributions to Ohio 529 college savings plans, which reduces Ohio taxable income dollar for dollar. Social Security benefits are fully exempt from Ohio income tax, which is relevant for retirees drawing Social Security alongside W-2 income from part-time work.

Ohio School District Income Tax: The Withholding Most Employees Miss

Ohio is one of only a handful of states that allows individual school districts to levy their own income tax on residents. This school district income tax (SDIT) is separate from state income tax, separate from municipal tax, and appears as its own line on the pay stub.

As of 2025, more than 200 Ohio school districts levy a SDIT. Rates range from 0.5% to 3.0%, with most districts charging between 0.75% and 2.0%. The key distinction: SDIT is based on where you live, not where you work.

Rules that catch new Ohio residents off guard:

- SDIT applies to all taxable income, including wages, interest, and dividends

- Employers withhold SDIT if the employee provides their school district number on the Ohio IT-4 form

- If an employer does not withhold, the employee still owes the tax when filing their Ohio state return

- Moving to a new address within Ohio may change your school district number, requiring an updated IT-4

Combined tax impact in Columbus:

Columbus charges a municipal income tax of 2.5% on wages earned within city limits. A Columbus resident in a school district charging 2.0% SDIT faces:

Ohio state income tax on $75,000: $1,326 (1.77%)

Columbus municipal tax: $75,000 × 2.5% = $1,875 (2.5%)

School district income tax: $75,000 × 2.0% = $1,500 (2.0%)

Total state/local: $4,701

Combined effective rate: 6.27%

That combined rate is still below what residents in New York City, California, or Maryland typically pay. But it is meaningfully higher than Ohio's state rate alone suggests, and new employees often underestimate their total tax burden by ignoring the SDIT line.

Federal Withholding on an Ohio Paycheck: The Larger Piece

For most Ohio workers, federal withholding takes more from each paycheck than state and local taxes combined. Federal income tax is withheld based on W-4 elections and the IRS graduated brackets.

2025 federal income tax brackets for single filers (for withholding reference):

| Taxable Income | Rate |

|---|---|

| Up to $11,925 | 10% |

| $11,926 to $48,475 | 12% |

| $48,476 to $103,350 | 22% |

| $103,351 to $197,300 | 24% |

| Over $197,300 | 32% |

FICA withholding applies to all W-2 wages:

- Social Security: 6.2% on wages up to $176,100 (2025 wage base)

- Medicare: 1.45% on all wages, plus an additional 0.9% on wages over $200,000

Federal vs Ohio state share at $75,000 (single, no pre-tax deductions):

Federal income tax (approximate): $10,294

Social Security: $75,000 × 6.2% = $4,650

Medicare: $75,000 × 1.45% = $1,088

Total federal: $16,032

Ohio state income tax: $1,326

State share of total tax burden: 7.6%

Federal share: 92.4%

The W-4 controls the largest single variable. Ohio workers who want more accurate withholding rather than a large refund or unexpected balance due should update their W-4 using the IRS Tax Withholding Estimator after any major life change: new job, marriage, new dependent, or significant side income.

The Nebraska, Minnesota, Utah, and Montana Paycheck Guide shows how Ohio's federal-dominated tax burden compares to states with significantly higher state income tax rates, where the federal/state split looks very different.

Ohio Take-Home Pay at $50K, $75K, and $100K

Three scenarios for a single Ohio filer, no dependents, no SDIT, no municipal tax, biweekly payroll, standard W-4 settings:

| Gross Salary | Federal Tax | FICA | Ohio State Tax | Take-Home | Effective Total Rate |

|---|---|---|---|---|---|

| $50,000 | $5,294 | $3,825 | $655 | $40,226 | 19.5% |

| $75,000 | $10,294 | $5,738 | $1,326 | $57,643 | 23.1% |

| $100,000 | $16,244 | $7,650 | $2,034 | $74,072 | 25.9% |

Adding Columbus city tax (2.5%) and a 1.5% SDIT to the $100,000 scenario:

Municipal tax: $100,000 × 2.5% = $2,500

SDIT: $100,000 × 1.5% = $1,500

Adjusted take-home: $74,072 - $4,000 = $70,072

Effective total rate: 29.9%

The municipal + SDIT addition of $4,000 per year is equivalent to about $154 per biweekly paycheck at $100,000. It is real money, and it is easy to underestimate when comparing job offers or budgeting a move to Ohio from a state with no local income tax structure.

Ohio vs Indiana, Pennsylvania, and Michigan

Ohio's neighbors put its rate structure in context.

| State | Structure | Rate on $75K (effective state) | Notable Feature |

|---|---|---|---|

| Ohio | Tiered, 0% floor | 1.77% | Zero-rate bracket on first $26,050 |

| Indiana | Flat + county tax | 3.05% + county | County tax adds 0.5% to 2.9% |

| Pennsylvania | Flat | 3.07% | No standard deduction, flat from dollar one |

| Michigan | Flat + city | 4.25% + Detroit 2.4% | Detroit has highest city rate in state |

| Kentucky | Flat | 4.0% | Simple, uniform statewide |

| West Virginia | Progressive | ~4.5% effective | Top bracket at 6.5% |

Ohio's 1.77% effective rate at $75,000 is the lowest of this group by a wide margin. Indiana and Pennsylvania both apply their flat rates from dollar one, making them more expensive for lower incomes. Michigan and Kentucky are both higher at every point in the $50,000 to $150,000 range.

Ohio's advantage narrows in cities with municipal tax. A Columbus worker effectively pays a similar total state/local rate to an Indianapolis worker once the Columbus 2.5% city tax is factored in alongside the SDIT, even though Ohio's state rate is far lower.

For Ohio employees looking to reduce their overall tax burden, the most effective lever is pre-tax 401k contributions. Each dollar of pre-tax retirement contribution reduces federal taxable income (saving at the marginal federal rate) and also reduces Ohio taxable income (saving at 2.75% or 3.5%). The Roth IRA Contribution Calculator shows how Roth contributions fit alongside pre-tax deferrals, and whether your income puts you in the phase-out range for 2026.

Ohio taxes the first $26,050 of income at 0%, then 2.75% on income from $26,051 to $100,000, and 3.5% above that. A $20 personal exemption credit reduces the tax owed after brackets are applied. On a $75,000 salary for a single filer, Ohio state income tax is approximately $1,326 per year, an effective rate of 1.77%. This is one of the lowest effective state income tax rates among Midwest states. The Ohio Paycheck Calculator shows exact per-paycheck withholding for any salary.

Ohio school district income tax (SDIT) is a local tax levied by individual school districts on residents within their boundaries. More than 200 Ohio school districts charge SDIT in 2025, with rates from 0.5% to 3.0%. It applies based on where you live, not where you work, and is separate from both state and municipal income taxes. If your employer does not withhold SDIT, you still owe it when filing your Ohio return. Check your pay stub for a line labeled "School District" to confirm withholding is occurring.

Several Ohio cities levy municipal income tax on wages earned within city limits. Columbus charges 2.5%, Cleveland 2%, Cincinnati 1.8%, and Toledo 2.25%. The tax applies to both residents and nonresidents who work in those cities. Suburban residents may also owe their home municipality a tax if they work in a higher-rate city that does not offer a full credit for taxes paid to the work city. Not all Ohio cities impose a municipal tax; smaller cities and rural areas often have none.

Start with gross salary. Subtract pre-tax deductions such as 401k, health insurance, and FSA. Apply federal income tax withholding based on W-4 filing status and the IRS brackets. Subtract FICA: 6.2% Social Security on wages up to $176,100 and 1.45% Medicare on all wages. Apply Ohio state income tax: 0% on the first $26,050, 2.75% from $26,051 to $100,000, 3.5% above that, minus the $20 personal exemption credit. Subtract any municipal tax and SDIT if applicable. The Ohio Paycheck Calculator runs all of these simultaneously for hourly and salaried workers.

Ohio's effective state income tax rate is lower than the nominal bracket rates suggest because of the 0% zero-rate floor on the first $26,050 of taxable income. At a $50,000 salary, the effective Ohio rate is approximately 1.3%. At $75,000, it is 1.77%. At $100,000, it is about 2.03%. The effective rate rises slowly because the largest bracket increase only kicks in above $100,000, and the 3.5% top rate is still well below neighboring states like Michigan (4.25% flat) or Kentucky (4.0% flat).

Ohio has the lowest effective state income tax burden of the major Midwest states for W-2 earners between $50,000 and $150,000. Indiana and Pennsylvania apply flat rates from dollar one (3.05% and 3.07%), making them more expensive at lower incomes. Michigan's 4.25% flat rate and Illinois's 4.95% flat rate are both higher than Ohio's effective rate at every income level below about $250,000. Ohio's advantage narrows in cities with municipal income tax, where the combined state and local rate can reach 6% to 7% in Columbus or Cleveland.

Written by

Hassaan Rasheed

Web Developer & Content Researcher

Hassaan builds calculators and writes research-backed guides on finance, math, payroll, and construction topics. Every number in his articles is sourced from official data and worked through by hand.

View LinkedIn Profile