Utah Paycheck Tax Guide: Flat 4.55% Rate, Credit Mechanism, and Take-Home Pay (2026)

Utah income tax: flat 4.55% rate with a personal exemption credit that reduces your bill directly. Take-home pay at $50K, $75K, and $100K for 2025.

Utah is the only state in the Mountain West with a flat income tax rate. That sounds simpler than progressive brackets, and for the most part it is. But the personal exemption credit mechanism introduces a feature that most explanations skip, and it changes the math in ways that matter for comparing Utah to its neighbors.

The Utah Paycheck Calculator applies the correct credit and rate for your salary automatically. This guide explains how the credit works, why it makes Utah's tax structure effectively progressive despite the flat rate headline, and what take-home pay actually looks like at common salary levels.

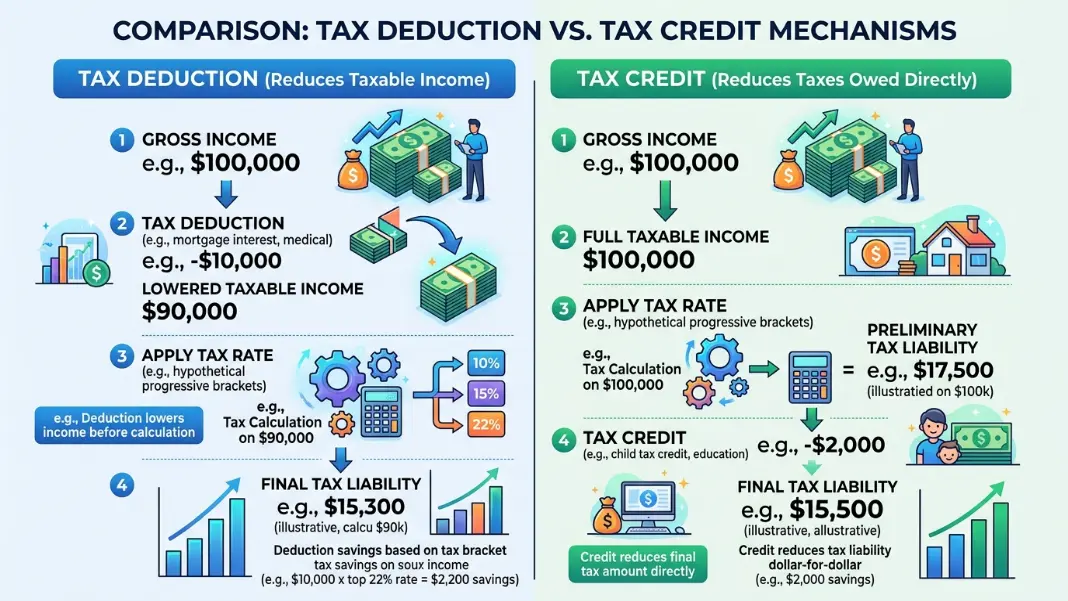

Most people see 4.55% and assume Utah income tax is simply 4.55% of wages. It is not quite that simple. Utah applies the flat rate first, then subtracts the personal exemption credit directly from the tax owed. That credit is a dollar-for-dollar reduction, not a deduction from income. The distinction matters.

Utah Income Tax: Flat 4.55% with a Credit, Not a Deduction

Utah applies a flat 4.55% rate to all taxable income. There are no brackets. A worker earning $40,000 and a worker earning $200,000 are both taxed at the same 4.55% rate on their taxable income. In that sense, the system is structurally simple.

The complication comes from the personal exemption credit. Single filers receive a credit of $878 that is subtracted directly from the computed tax. This is not a deduction that reduces income before the rate is applied. It reduces the tax bill itself, dollar for dollar.

The formula:

Utah Tax = (Taxable Income x 0.0455) - $878

At $50,000 gross income, taxable income is roughly $50,000 (Utah generally conforms to federal adjusted gross income, so pre-tax deductions like 401k reduce this figure). Applying the formula:

$50,000 x 0.0455 = $2,275

$2,275 - $878 = $1,397 Utah state tax

Effective rate on $50,000: 2.79%

At $100,000:

$100,000 x 0.0455 = $4,550

$4,550 - $878 = $3,672 Utah state tax

Effective rate on $100,000: 3.67%

The stated rate is 4.55% in both cases, but the effective rates are 2.79% and 3.67%. They are different because the $878 credit represents a larger percentage of the total tax bill at lower incomes. This is why Utah is sometimes described as "effectively progressive" despite having no progressive brackets.

Credit vs deduction: why the mechanics matter

Most states and the federal government use deductions to reduce taxable income before applying the rate. A $10,000 federal standard deduction at a 22% marginal rate saves $2,200 in federal tax. The deduction scales with your marginal rate, so higher earners benefit more from the same deduction in dollar terms.

Utah does the opposite. The credit does not scale with income or rate. Everyone gets the same $878 reduction regardless of whether they earn $30,000 or $300,000. That fixed dollar amount represents 63% of the tax owed at $50,000 gross but only 19% of the tax owed at $100,000 gross. The lower the income, the more meaningful the credit.

A rough equivalence: an $878 credit at 4.55% is mathematically equivalent to a $19,296 income deduction. At $50,000 gross, removing $19,296 from taxable income before applying the rate would produce the same result. At $150,000 gross, that same notional deduction amount is a much smaller proportion of total income, so its impact shrinks.

How the Personal Exemption Credit Works (and Why It Phases Out)

The $878 credit figure used here matches the amount applied in the existing four-state comparison guide and is the figure the Utah calculator uses. The statutory credit for single filers was set at $1,878 under Utah code, but it phases out for higher earners.

The phaseout begins at roughly $15,095 in Utah modified adjusted gross income for single filers. The credit reduces by approximately 1.3 cents for each dollar earned above that threshold. By approximately $159,000, the credit has fully phased out for single filers at higher incomes.

For practical purposes at common salary ranges:

- At $50,000: the full credit or close to it applies

- At $75,000: the credit is partially reduced

- At $100,000: the credit is further reduced

- At $160,000 and above: the credit may be eliminated

The $878 figure used in the take-home calculations below reflects a conservative mid-range estimate consistent with the existing Utah calculator. Higher-income workers should note their effective credit may be lower than $878, which would increase their effective state rate slightly above the figures shown here.

For married filing jointly filers, the credit doubles to $1,756 before phaseout, and the phaseout threshold is higher. A married household earning $75,000 keeps more of the credit than a single filer at the same income.

Utah has no local income taxes. No city or county adds a local line to your paycheck. Salt Lake City, Provo, Ogden, and every other municipality in the state applies no additional withholding.

Federal Withholding on a Utah Paycheck

Federal taxes are calculated identically across all states and represent the majority of withholding for most workers.

2025 federal income tax brackets for single filers:

| Taxable Income | Rate |

|---|---|

| Up to $11,925 | 10% |

| $11,926 to $48,475 | 12% |

| $48,476 to $103,350 | 22% |

| $103,351 to $197,300 | 24% |

| Over $197,300 | 32%+ |

FICA withholding on all W-2 wages:

- Social Security: 6.2% on wages up to $176,100 (2025 wage base)

- Medicare: 1.45% on all wages, plus 0.9% on wages over $200,000

Federal vs Utah breakdown at $75,000 (single):

Federal income tax (approximate): $10,294

Social Security ($75,000 x 6.2%): $4,650

Medicare ($75,000 x 1.45%): $1,088

Total FICA: $5,738

Utah state income tax: $2,535 (4.55% minus $878 credit)

Effective Utah rate on $75,000: 3.38%

Total withholding: $18,567

Take-home: $56,433

Federal taxes at $75,000 are four times the Utah state tax. When workers in other states hear that Utah has a 4.55% income tax, the effective rate they actually pay is well below that headline number once the credit is applied. At $75,000, the 3.38% effective Utah rate is competitive with states that promote flat rates as low as 4%.

Utah conforms to the federal definition of taxable income for most purposes. Pre-tax 401k contributions, health insurance premiums paid through an employer cafeteria plan, and HSA contributions all reduce both federal and Utah taxable income. A $6,000 annual 401k contribution saves approximately $1,320 in federal taxes (22% bracket) and approximately $273 in Utah state taxes (4.55% flat), for a combined $1,593 in annual savings.

Social Security and retirement income:

Utah does not provide a blanket Social Security exemption like Illinois or Nebraska. Most Social Security benefits received by Utah retirees are included in federal adjusted gross income (up to 85% under federal rules), and Utah taxes that amount at the 4.55% rate. Utah does offer a retirement credit that partially offsets state tax on retirement income for lower-income retirees, but it is not a full exemption and phases out at modest income levels. Retirees comparing Utah to states with full Social Security exemptions should factor this in.

Utah Take-Home Pay at $50K, $75K, and $100K

Three scenarios for a single Utah filer, $878 credit applied, no pre-tax deductions, standard W-4 settings, biweekly payroll:

| Gross Salary | Federal Tax | FICA | UT State Tax | Take-Home | Effective Total Rate |

|---|---|---|---|---|---|

| $50,000 | $5,294 | $3,825 | $1,397 | $39,484 | 21.1% |

| $75,000 | $10,294 | $5,738 | $2,535 | $56,433 | 24.8% |

| $100,000 | $16,244 | $7,650 | $3,672 | $72,434 | 27.6% |

Utah state tax calculations:

At $50,000: $50,000 x 4.55% = $2,275; minus $878 credit = $1,397. Effective state rate: 2.79%.

At $75,000: $75,000 x 4.55% = $3,413; minus $878 credit = $2,535. Effective state rate: 3.38%.

At $100,000: $100,000 x 4.55% = $4,550; minus $878 credit = $3,672. Effective state rate: 3.67%.

The Utah state tax line increases linearly once you see the formula. Every additional $10,000 in gross income adds exactly $455 in state tax (4.55% of $10,000), since the credit is a fixed deduction from the final number. This predictability is one practical advantage of the flat-rate structure: there are no bracket thresholds to plan around.

For workers comparing Utah to neighboring states more broadly, the four-state guide covering Nebraska, Minnesota, Utah, and Montana shows Utah's take-home side by side with progressive-rate states: NE, MN, UT, MT Paycheck Guide. At every income level in that comparison, Utah produces the lowest or second-lowest state tax burden.

Effect of pre-tax contributions at $100,000:

A worker at $100,000 contributing $10,000 per year to a traditional 401k:

- Reduces federal taxable income from approximately $85,000 to $75,000, saving about $2,200 in federal taxes

- Reduces Utah taxable income by $10,000, saving $455 in state taxes

- Total annual tax savings: approximately $2,655

- Net cost of $10,000 contribution after tax savings: approximately $7,345

Utah vs Colorado, Nevada, Arizona, and Idaho

Utah sits in a regional context where several states offer dramatically different income tax structures.

| State | Structure | Effective Rate at $75K | Local Tax |

|---|---|---|---|

| Utah | Flat 4.55% plus credit | ~3.38% | None |

| Colorado | Flat 4.40% | 4.40% | Denver: occupational privilege tax (threshold-based) |

| Nevada | No income tax | 0% | None |

| Arizona | Flat 2.5% | 2.50% | None |

| Idaho | Progressive | ~4.8% (5.695% max) | None |

Colorado is the closest structural comparison to Utah: both use flat rates with no progressive brackets on earned income. Colorado's 4.40% rate is lower than Utah's 4.55% stated rate, but Utah's credit produces a lower effective rate for most workers.

At $75,000, Colorado's 4.40% flat rate on taxable income produces roughly $2,640 in state tax (after the Colorado standard deduction), while Utah's credit-adjusted rate produces $2,535. Utah is about $105 per year cheaper at this income. The crossover where Colorado becomes cheaper than Utah depends on income level and how much of the Utah credit has phased out. Below about $100,000 in gross income, Utah typically wins on state tax burden. Above that level, the phasing credit narrows the gap.

Denver adds an occupational privilege tax that applies to workers earning above a certain income threshold within Denver. This is not a percentage-based income tax in the traditional sense, but it is a cost that does not exist for Utah workers.

Nevada deserves a clear statement: Nevada's 0% state income tax is the most favorable income tax environment in the Mountain West, but it is not meaningful for workers who need to compare job offers that require living in Utah versus Nevada specifically. If relocation is on the table, Nevada's lack of income tax is a real financial factor. For workers already employed in Utah comparing notes, it is not actionable.

Arizona at 2.5% flat is the lowest flat income tax rate in the Mountain West region by a significant margin. It beats Utah on state income taxes at every income level. A single filer at $75,000 pays approximately $1,875 in Arizona state income tax versus $2,535 in Utah, a difference of $660 per year. Workers near the Utah-Arizona border choosing where to live face a real tax difference, though Arizona has its own cost of living and property tax considerations.

Idaho uses progressive brackets with a top rate of 5.695% that kicks in at much lower income levels than, say, Minnesota's top bracket. At $75,000, Idaho's effective state rate is approximately 4.8%, higher than Utah's 3.38%. Idaho workers get no equivalent of Utah's exemption credit.

For workers building retirement savings from a Utah paycheck, the Roth IRA Contribution Calculator shows the 2026 phase-out thresholds for Roth contributions based on modified AGI, which is relevant for Utah workers in the $130,000 to $165,000 range where single-filer eligibility begins phasing out. Since Utah taxes traditional IRA distributions at 4.55%, the Roth versus traditional decision has state tax implications beyond just the federal rate difference.

For a look at how South Carolina structures its flat-rate system differently, with a two-tier rate and a zero-rate tier rather than a credit mechanism, the South Carolina Paycheck Calculator Guide covers how that approach changes the effective rate curve compared to Utah's credit system.

Utah applies a flat 4.55% rate to all taxable income, then subtracts a personal exemption credit of $878 for single filers directly from the tax owed. The result is an effective rate lower than the stated 4.55%. At $50,000 gross, the effective Utah rate is approximately 2.79%. At $75,000, it is approximately 3.38%. At $100,000, approximately 3.67%. The credit phases out at higher incomes, so very high earners approach but do not typically reach the full 4.55% effective rate. The Utah Paycheck Calculator applies the correct credit for your salary.

The Utah personal exemption credit is $878 for single filers (before phaseout) and reduces your computed state tax bill directly, not your taxable income. A deduction reduces income before the rate is applied, so its value scales with your marginal rate. A credit is a flat dollar reduction off the final tax number. The $878 credit is equivalent to roughly a $19,296 income deduction at 4.55%, but its proportional impact is much larger for lower-income earners and shrinks as income rises.

No. Utah does not allow cities or counties to levy local income taxes. Every Utah W-2 worker pays only the state flat rate regardless of whether they work in Salt Lake City, Provo, Ogden, or a rural area. This is consistent with most Mountain West states. Colorado's Denver has an occupational privilege tax, but Utah has no equivalent. Your Utah take-home pay is the same state tax calculation no matter where in the state your employer is located.

Both states use flat rates. Colorado's stated rate of 4.40% is lower than Utah's 4.55%, but Utah's $878 personal exemption credit means the effective rate in Utah is lower for most incomes. At $75,000, Utah's effective rate is approximately 3.38% versus Colorado's approximately 3.5% to 3.7% after the Colorado standard deduction. Utah is typically cheaper than Colorado in state income tax below about $100,000 gross income. Above that level, the Utah credit phases out and Colorado's lower flat rate can win, depending on individual deductions.

Utah does not provide a full Social Security exemption like Illinois or Nebraska. Social Security benefits are generally included in Utah taxable income following federal treatment (up to 85% of benefits depending on total income). Utah does offer a retirement credit for lower-income retirees that partially offsets state tax on retirement income, but it phases out at modest income levels and is not a blanket exemption. Retirees with significant Social Security income should factor in Utah's treatment compared to states with full SS exemptions when making relocation decisions.

Arizona applies a flat 2.5% state income tax rate, the lowest flat rate in the Mountain West. At $75,000, Arizona state tax is approximately $1,875 versus Utah's $2,535 after the credit, a difference of $660 per year. Nevada has no state income tax on wages, making it the most favorable in the region. For workers comparing job offers between Utah and Arizona, the state income tax difference is real and worth quantifying with your actual salary. Nevada's 0% is only relevant if relocation to Nevada is actually on the table.

Traditional 401k contributions reduce both federal and Utah taxable income, since Utah conforms to federal adjusted gross income definitions. At $75,000 gross, a $6,000 annual 401k contribution saves approximately $273 in Utah state taxes (4.55% of $6,000) on top of about $1,320 in federal savings. The state savings in Utah are smaller in dollar terms than in progressive high-rate states like Minnesota, where a 6.80% or 7.85% marginal rate produces larger state savings per dollar contributed. But the combined federal plus state benefit still makes pre-tax contributions the default right choice for most Utah workers.

Written by

Hassaan Rasheed

Web Developer & Content Researcher

Hassaan builds calculators and writes research-backed guides on finance, math, payroll, and construction topics. Every number in his articles is sourced from official data and worked through by hand.

View LinkedIn Profile