Roth IRA Contribution Limits 2026: Phase-Out Calculator

2026 Roth IRA limits: $7,000 ($8,000 if 50+). Phase-out begins at $150k single, $236k married. Calculate your exact allowed contribution. No signup.

The Roth IRA is the most tax-efficient retirement account available to most Americans: contributions go in after-tax, growth is tax-free, and qualified withdrawals in retirement are also tax-free. The catch is that contribution eligibility phases out at higher incomes and disappears entirely above a threshold. The Roth IRA Contribution Calculator calculates your exact allowed contribution based on your MAGI, filing status, and age. This article covers how the limits work, how phase-outs reduce your allowable contribution dollar-by-dollar, and what to do when your income exceeds the limit entirely.

2026 Roth IRA Contribution Limits by Age

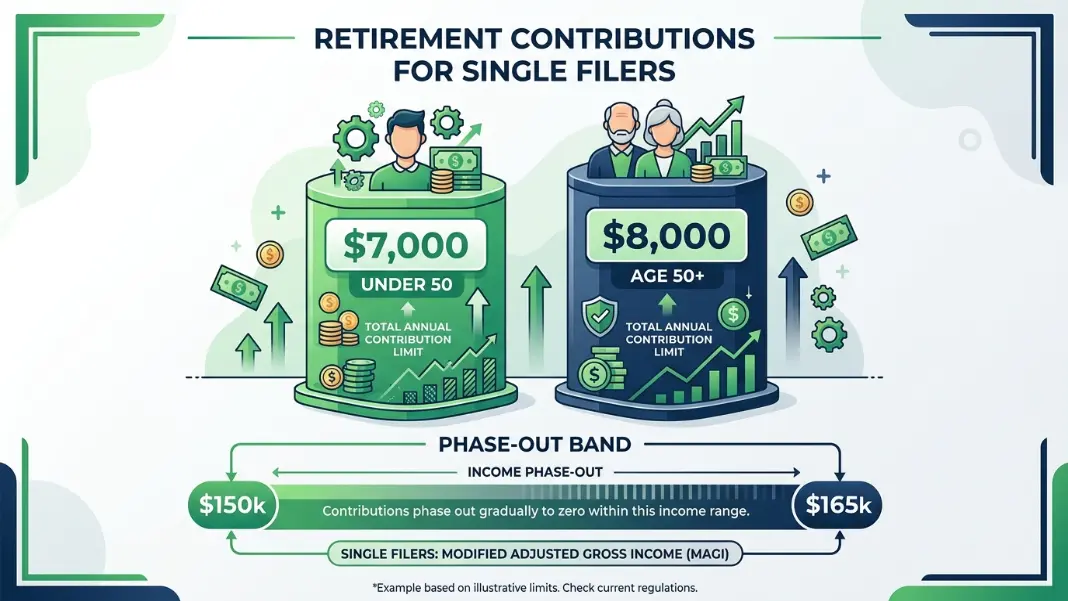

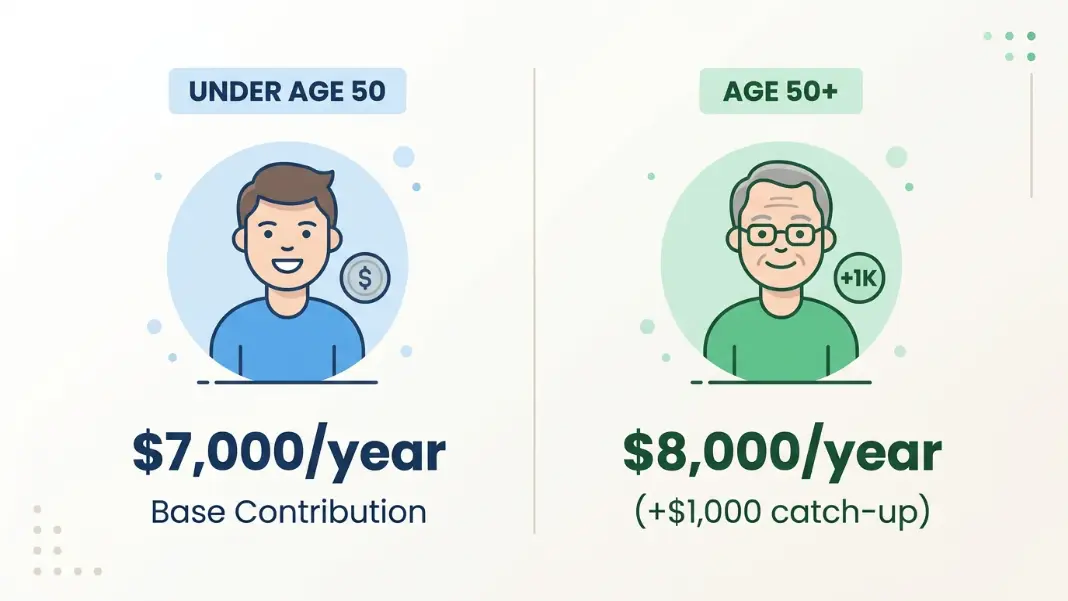

The base contribution limit for 2026 is $7,000 for anyone under 50. Taxpayers aged 50 and older can contribute $8,000 — the extra $1,000 is the IRS catch-up contribution, designed to help near-retirement savers accelerate tax-free accumulation.

Contribution limits at a glance:

| Age | 2026 Annual Limit |

|---|---|

| Under 50 | $7,000 |

| 50 and older | $8,000 |

| Any age with earned income below the limit | Equal to earned income |

Four rules govern the limit in practice:

- The $7,000/$8,000 cap applies to your total IRA contributions across all traditional and Roth IRAs combined. Contributing $3,000 to a traditional IRA leaves only $4,000 remaining for a Roth (or $5,000 if 50+).

- You cannot contribute more than your earned income for the year. If you earn $4,500, your maximum Roth IRA contribution is $4,500, not $7,000.

- The limit is per person, not per household. A married couple can each contribute the full amount, up to $14,000 combined ($16,000 if both are 50+).

- The contribution deadline is April 15 of the following year. You can contribute to your 2026 Roth IRA any time between January 1, 2026, and April 15, 2027.

Roth IRA Income Phase-Out: How to Calculate Your Reduced Limit

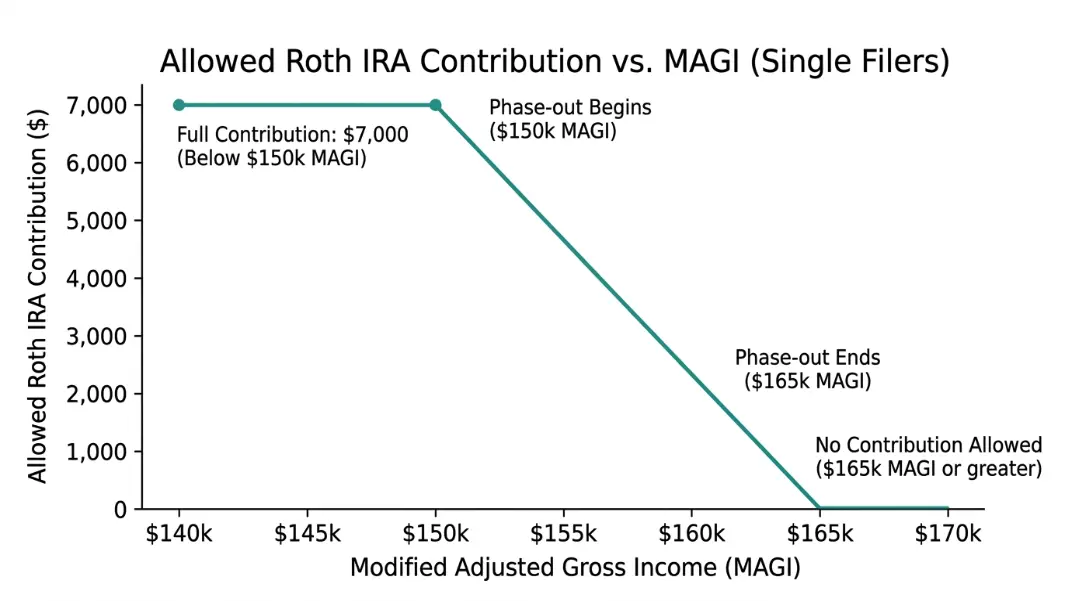

The Roth IRA phase-out reduces your allowed contribution proportionally as your modified adjusted gross income (MAGI) rises through a defined range. Once MAGI clears the top of the range, no direct Roth IRA contribution is allowed.

2026 Roth IRA phase-out ranges:

| Filing Status | Phase-Out Begins | Phase-Out Ends |

|---|---|---|

| Single / Head of Household | $150,000 | $165,000 |

| Married Filing Jointly | $236,000 | $246,000 |

| Married Filing Separately | $0 | $10,000 |

Phase-out formula:

Phase-Out % = (MAGI - Phase-Out Floor) ÷ Phase-Out Range Width

Reduced Limit = Full Limit × (1 - Phase-Out %)

Round down to nearest $10, minimum $200

For single filers the range width is $15,000. For married filing jointly it is $10,000. The narrower MFJ window means joint filers can go from full eligibility to none in just $10,000 of additional income.

Worked example — single filer, age 38, MAGI $158,000:

Phase-Out % = ($158,000 - $150,000) ÷ $15,000 = 53.3%

Reduced Limit = $7,000 × (1 - 0.533) = $3,269

Rounded down to nearest $10: $3,260

This taxpayer can contribute $3,260 for 2026. The $200 IRS minimum applies as long as MAGI stays below $165,000.

Worked example — married filing jointly, age 52, MAGI $241,000:

Phase-Out % = ($241,000 - $236,000) ÷ $10,000 = 50%

Reduced Limit = $8,000 × (1 - 0.50) = $4,000

With the catch-up contribution, this taxpayer can put $4,000 into a Roth IRA for 2026.

Roth IRA Contribution Limit Calculator: Three Worked Scenarios

Scenario 1: Single, age 32, MAGI $95,000

MAGI is well below the $150,000 floor. Full $7,000 contribution allowed with no reduction.

Scenario 2: Single, age 55, MAGI $162,000

Age 55 means the $8,000 catch-up limit applies. MAGI is inside the phase-out range.

Phase-Out % = ($162,000 - $150,000) ÷ $15,000 = 80%

Reduced Limit = $8,000 × (1 - 0.80) = $1,600

Maximum contribution: $1,600. Another $3,000 of MAGI would eliminate direct Roth eligibility entirely.

Scenario 3: Married filing jointly, age 44, MAGI $248,000

MAGI exceeds $246,000 (top of the MFJ range). No direct Roth IRA contribution is allowed. The backdoor Roth strategy, covered below, applies here.

The Roth IRA Contribution Calculator takes your exact MAGI, filing status, and age and returns the precise allowed contribution. It also projects the tax-free growth of that contribution over a chosen time horizon at a specified annual return rate.

Roth IRA vs Traditional IRA: Which to Use First

Roth and traditional IRAs share the same $7,000/$8,000 combined annual limit. Splitting between both is allowed, but the total across both accounts cannot exceed the cap.

Choosing between them:

| Factor | Favor Roth | Favor Traditional |

|---|---|---|

| Current tax bracket | 22% or below | 24% or higher |

| Expected retirement bracket | Higher than today | Lower than today |

| Need for early access | Yes (contributions withdraw penalty-free) | No |

| Required minimum distributions | No RMDs from Roth | RMDs begin at age 73 |

| State tax situation | Low or no state income tax | High current state tax, low in retirement |

The Roth vs Traditional 401k Calculator illustrates the breakeven tax rate between both structures. The same logic applies to IRA comparisons: Roth wins when your current marginal rate is lower than your expected retirement rate, and traditional wins when the reverse is true.

For high earners who can contribute to both a 401k and a Roth IRA, the standard priority is: contribute enough to the 401k to capture the full employer match, then max the Roth IRA if income is under the limit, then return to the 401k for additional pre-tax contributions. The 401k Match Calculator shows the real dollar value of capturing every dollar of employer match before allocating money elsewhere.

Backdoor Roth IRA: Contributing Past the Income Limit

Taxpayers above the Roth IRA income limit can still get money into a Roth account using a two-step process:

Step 1 — Non-deductible traditional IRA contribution. There is no income limit on traditional IRA contributions, only on deductibility. Contribute up to $7,000 ($8,000 if 50+) on an after-tax, non-deductible basis.

Step 2 — Roth conversion. Convert the traditional IRA balance to a Roth IRA. The conversion is a taxable event, but if you contribute and convert promptly before any earnings accumulate, the tax owed is close to zero on the contributed amount.

The pro-rata rule — the main complication:

If you hold pre-tax money in any traditional IRA (from prior deductible contributions or rollover accounts), the IRS treats all traditional IRAs as one pool. You cannot convert only the after-tax dollars. The taxable portion of any conversion is:

Taxable % = Pre-Tax IRA Balance ÷ Total Traditional IRA Balance

A taxpayer with $100,000 in a rollover IRA and a $7,000 new after-tax contribution has a $107,000 total balance. Only 6.5% of any conversion is after-tax. Converting $7,000 means $6,545 is taxable.

The cleanest backdoor Roth execution starts with zero pre-tax IRA balances. Taxpayers with large rollover IRAs often roll those assets into a current employer's 401k first to clear the pro-rata issue, then execute the backdoor conversion. Consistent annual Roth contributions — whether direct or backdoor — are a core component of partial early retirement strategies like Barista FIRE, where tax-free Roth withdrawals reduce the income needed from taxable accounts. The Barista FIRE Calculator models this alongside part-time income scenarios.

The 2026 Roth IRA contribution limit is $7,000 per year for anyone under 50, and $8,000 for those aged 50 and older. This limit applies across all your traditional and Roth IRAs combined. The limit phases out for single filers with MAGI between $150,000 and $165,000, and for married filing jointly between $236,000 and $246,000. Above those ranges, direct contributions are not allowed, but the backdoor Roth strategy remains available regardless of income.

Subtract the phase-out floor from your MAGI, then divide by the range width ($15,000 for single filers, $10,000 for married filing jointly). That gives your phase-out percentage. Multiply your full limit ($7,000 or $8,000) by one minus that percentage, then round down to the nearest $10. The minimum allowed contribution is $200 as long as MAGI stays below the top of the range. The Roth IRA Contribution Calculator runs this calculation automatically.

Yes. The Roth IRA and 401k limits are completely separate. For 2026, you can contribute up to $7,000 to a Roth IRA and the full 401k limit to your employer plan in the same year. One indirect benefit: pre-tax 401k contributions reduce your MAGI, which can keep you under or inside the Roth IRA phase-out threshold if your income is near the limit.

MAGI (modified adjusted gross income) starts with your AGI and adds back certain deductions including student loan interest, IRA deductions, and foreign income exclusions. For most W-2 employees without self-employment income or foreign income, MAGI equals AGI. For self-employed individuals, MAGI excludes the self-employment tax deduction and SEP IRA contributions, which can lower the effective MAGI well below gross revenue.

Excess Roth IRA contributions are subject to a 6% excise tax per year for every year the excess remains in the account. Remove the excess contribution plus any earnings generated on it before the tax filing deadline (including extensions) to avoid the penalty. If you discover the excess after filing, withdraw it and file an amended return using IRS Form 5329 to report and calculate the excise tax.

Yes, indirectly. Traditional 401k contributions are pre-tax and reduce your AGI, which in turn reduces your MAGI. A lower MAGI can keep you below the Roth IRA phase-out threshold or reduce the phase-out amount. For example, a single filer earning $168,000 gross who contributes $23,500 to a traditional 401k has a MAGI of roughly $144,500 — below the $150,000 phase-out floor — making them fully eligible for the $7,000 Roth IRA contribution.

Written by

Hassaan Rasheed

Web Developer & Content Researcher

Hassaan builds calculators and writes research-backed guides on finance, math, payroll, and construction topics. Every number in his articles is sourced from official data and worked through by hand.

View LinkedIn Profile