Ohio Hourly Paycheck Calculator: Overtime, Taxes, and Take-Home Pay (2026)

Ohio hourly paycheck: 0% on first $26,050, then 2.75%. How overtime, SDIT, and city tax affect hourly workers' take-home pay at $15 to $30/hr.

Hourly workers in Ohio have a genuine tax advantage most salary earners never think about. Ohio's zero-rate bracket covers the first $26,050 of taxable income, which means a full-time worker earning $15 an hour pays roughly $122 in Ohio state income tax for the entire year. That is not a rounding error. It is a structural feature of how Ohio taxes income, and hourly workers in the $15 to $25 range sit mostly in that zero bracket or just above it.

The Ohio Paycheck Calculator handles hourly pay directly: enter your hourly rate, hours per week, and pay frequency, and it calculates gross pay, federal withholding, FICA, Ohio state tax, and your local add-ons. This guide explains the mechanics behind those numbers so you know why each line exists and how overtime changes the picture.

Ohio's state income tax is only one of three layers on an Ohio hourly paycheck. The school district income tax (SDIT) and municipal income tax are the two that consistently catch people off guard when they move to Ohio or start a new job.

Converting Ohio Hourly Wages to Gross Pay: Regular Hours and Overtime

Gross pay is the starting point for every tax calculation. For hourly workers, it depends on how many hours you work and whether any of those hours qualify for overtime.

The federal Fair Labor Standards Act (FLSA) requires most employers to pay 1.5 times the regular hourly rate for any hours worked beyond 40 in a single workweek. Ohio follows the federal overtime rule with no state-level additions for most workers.

Regular gross = Hourly rate x Hours worked (up to 40)

Overtime gross = Hourly rate x 1.5 x Hours worked over 40

Weekly gross = Regular gross + Overtime gross

Annual gross = Weekly gross x 52

Worked example at $20/hr with 5 overtime hours in one week:

- Regular: $20 x 40 = $800

- Overtime: $20 x 1.5 x 5 = $150

- Weekly gross: $950

- Annualized (if every week had this pattern): $49,400

Standard annual gross at common Ohio hourly rates (40 hours/week, 52 weeks):

These figures show base annual earnings before any overtime.

| Hourly Rate | Annual Gross (2,080 hrs) | Weekly Gross |

|---|---|---|

| $12 | $24,960 | $480 |

| $15 | $31,200 | $600 |

| $18 | $37,440 | $720 |

| $20 | $41,600 | $800 |

| $25 | $52,000 | $1,000 |

| $30 | $62,400 | $1,200 |

Notice that a $12/hr worker earning $24,960 annually sits entirely within Ohio's zero-rate bracket. They will owe zero Ohio state income tax unless overtime or a second job pushes them above $26,050. The $15/hr worker at $31,200 is just $5,150 above that floor.

Ohio State Tax on an Hourly Paycheck: The Zero-Rate Floor in Practice

Ohio taxes hourly income on the same brackets as salaried income. The zero-rate floor at $26,050 is the most significant factor for hourly workers earning under about $13 to $16 per hour full time.

Ohio state income tax brackets for 2025-26 (single filer):

| Taxable Income | Rate |

|---|---|

| Up to $26,050 | 0% |

| $26,051 to $100,000 | 2.75% |

| Over $100,000 | 3.125% (2025); 2.75% (2026 forward) |

Ohio also applies a personal exemption credit of $20 per taxpayer, subtracted directly from the tax owed after brackets are applied. This is not a deduction from income but a flat credit off the final bill.

Ohio state tax at common hourly rates (annual, single filer, no dependents):

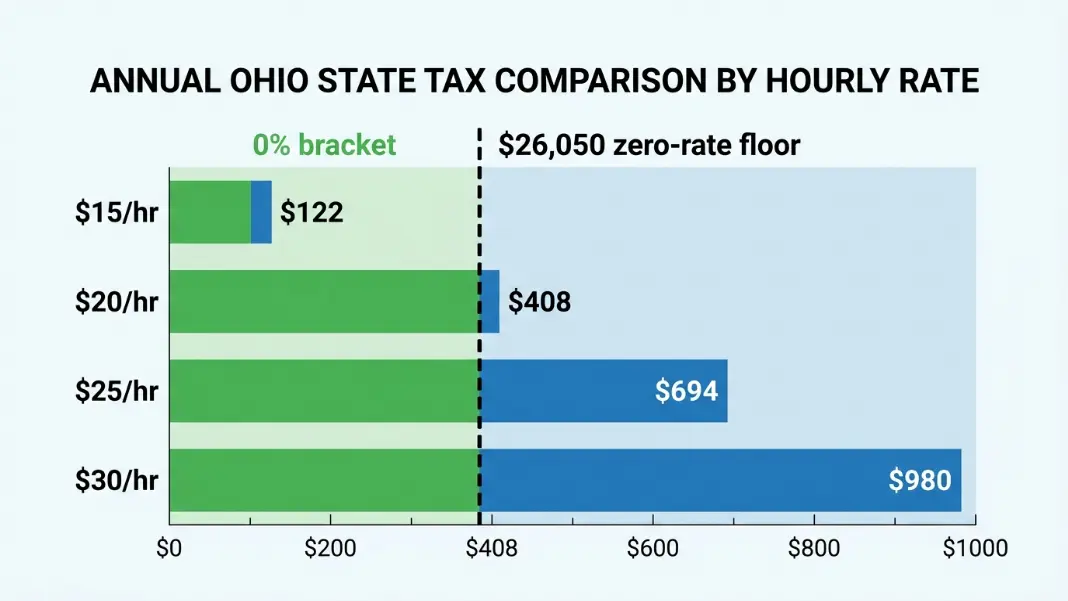

$15/hr ($31,200): 2.75% x ($31,200 - $26,050) = $142; minus $20 credit = $122/year

$20/hr ($41,600): 2.75% x ($41,600 - $26,050) = $428; minus $20 credit = $408/year

$25/hr ($52,000): 2.75% x ($52,000 - $26,050) = $714; minus $20 credit = $694/year

$30/hr ($62,400): 2.75% x ($62,400 - $26,050) = $1,000; minus $20 credit = $980/year

The effective Ohio state rate on a $31,200 salary is 0.39%. On a $52,000 salary it is 1.34%. Ohio's effective rates for hourly workers are among the lowest in the Midwest, and the gap between Ohio and its neighbors (Indiana 3.05% flat, Michigan 4.25% flat) is real money over a full year.

For a detailed breakdown of how Ohio compares to Indiana, Pennsylvania, and Michigan for W-2 workers at common salary levels, the Ohio Paycheck Tax Guide has side-by-side take-home comparisons at $50,000, $75,000, and $100,000.

SDIT and City Tax on an Ohio Hourly Paycheck: The Third and Fourth Lines

State income tax is not the dominant Ohio-specific deduction for most hourly workers. SDIT and city tax often take more combined than Ohio state tax does.

School District Income Tax (SDIT)

Ohio allows individual school districts to levy their own income tax on residents. Over 200 districts do. Rates range from 0.5% to 3.0%, with most falling between 0.75% and 2.0%. SDIT is based on where you live, not where you work. You owe it regardless of which city or county your employer is in.

At $41,600 annual earnings:

| SDIT Rate | Annual SDIT | Per Biweekly Paycheck |

|---|---|---|

| 0.5% | $208 | $8 |

| 1.0% | $416 | $16 |

| 1.5% | $624 | $24 |

| 2.0% | $832 | $32 |

If your employer does not withhold SDIT automatically, you are still on the hook when you file your Ohio state return. This is the line that generates the most surprises when Ohio workers file for the first time. The Ohio School District Income Tax Guide covers how to find your district number and rate, and what to do if your employer missed it.

Municipal Income Tax

Ohio's 900-plus municipalities are permitted to levy their own income tax on wages earned within city limits. The largest cities and their 2025 rates:

| City | Municipal Tax Rate |

|---|---|

| Columbus | 2.5% |

| Cleveland | 2.5% |

| Cincinnati | 1.8% |

| Toledo | 2.25% |

| Akron | 2.5% |

| Dayton | 2.5% |

Unlike SDIT, the municipal tax is based on where you work. A worker living in a Columbus suburb but working in Columbus owes the 2.5% Columbus city tax on wages earned there. Their home suburb may or may not charge its own rate. If it does, a resident credit usually prevents full double taxation.

At $41,600 in Columbus with a 2.5% municipal rate: $41,600 x 2.5% = $1,040 per year, or $40 per biweekly paycheck. That is more than twice the Ohio state income tax for the same worker.

The Ohio City Income Tax Guide covers resident credits, dual-city workers, and how the calculation works when you live in one jurisdiction and work in another.

Ohio Hourly Take-Home Pay at $15, $20, $25, and $30 per Hour

The figures below assume a single filer, no pre-tax deductions, standard W-4, biweekly payroll, and a Columbus location (2.5% city tax, 1.5% SDIT as a representative example). Federal withholding uses 2025 brackets and the $15,000 standard deduction.

Annual take-home with Columbus city and SDIT:

| Hourly Rate | Gross | Federal Tax | FICA | OH State | City+SDIT | Take-Home |

|---|---|---|---|---|---|---|

| $15/hr | $31,200 | $1,620 | $2,387 | $122 | $1,248 | $25,823 |

| $20/hr | $41,600 | $2,954 | $3,182 | $408 | $1,664 | $33,392 |

| $25/hr | $52,000 | $4,202 | $3,978 | $694 | $2,080 | $41,046 |

| $30/hr | $62,400 | $5,450 | $4,774 | $980 | $2,496 | $48,700 |

Annual take-home without city tax (rural Ohio or no municipal tax zone):

For workers whose employer is located in a non-taxing municipality and whose home district has no SDIT, take-home is noticeably higher.

| Hourly Rate | Gross | Federal Tax | FICA | OH State | Take-Home |

|---|---|---|---|---|---|

| $15/hr | $31,200 | $1,620 | $2,387 | $122 | $27,071 |

| $20/hr | $41,600 | $2,954 | $3,182 | $408 | $35,056 |

| $25/hr | $52,000 | $4,202 | $3,978 | $694 | $43,126 |

| $30/hr | $62,400 | $5,450 | $4,774 | $980 | $51,196 |

The gap between the Columbus worker and the rural Ohio worker at $20/hr is $1,664 per year, entirely from local taxes. That is the cost of working in a major Ohio city, and it compounds at higher hourly rates.

What this looks like per biweekly paycheck:

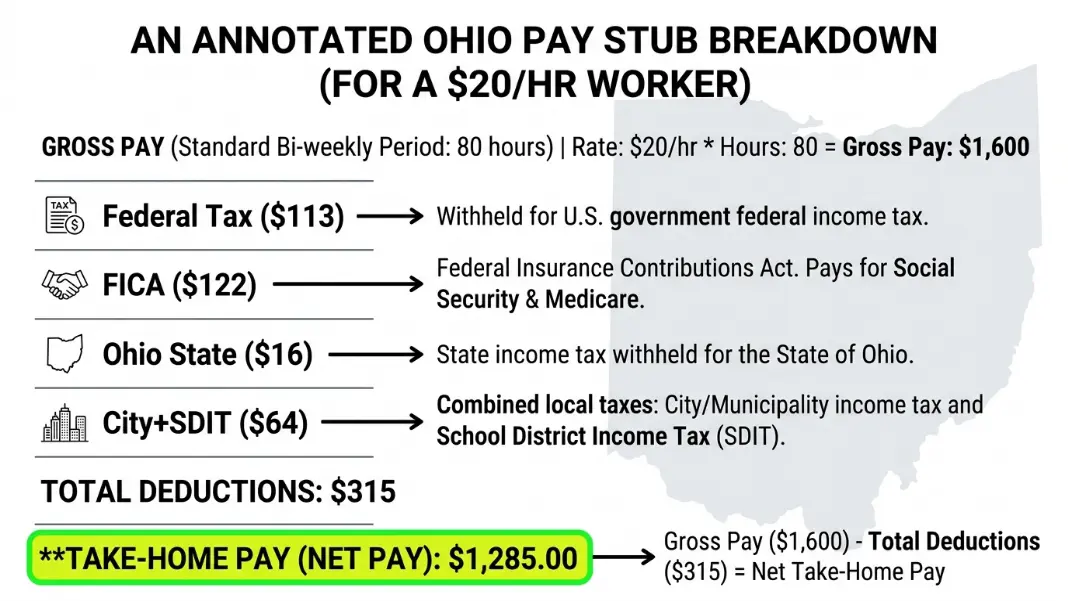

A Columbus worker at $20/hr brings home $33,392 annually, or $1,285 per biweekly paycheck out of $1,600 gross. Just over 20% disappears before they see it, split roughly: 7.1% federal, 7.65% FICA, 1.0% Ohio state, 4.0% local.

Overtime Pay and Withholding: Why Extra Hours Can Feel Disproportionately Taxed

Overtime increases gross pay, which is straightforward. What is less obvious is how withholding responds to an overtime paycheck.

Employers calculate federal income tax withholding by annualizing your paycheck. If your regular biweekly gross is $1,600 ($20/hr, 80 hours), the employer treats that as $41,600 per year and withholds accordingly. When you work overtime and your biweekly gross becomes $1,900 ($20/hr regular + $450 overtime), the employer annualizes $1,900 to $49,400 and applies the higher withholding rate for that annualized income.

At $49,400 annualized, more income falls in the 22% federal bracket compared to the $41,600 base. The result: that overtime paycheck has a noticeably higher percentage withheld for federal taxes than your regular paycheck.

Example: federal withholding on a regular vs. overtime biweekly paycheck at $20/hr:

Regular paycheck: $1,600 gross, annualized to $41,600

Taxable income after $15,000 standard deduction: $26,600

Federal withholding rate at that income: 10-12% range

Approx. biweekly federal withholding: $113

Overtime paycheck: $1,900 gross (5 extra OT hours), annualized to $49,400

Taxable income after standard deduction: $34,400

Federal withholding rate at that income: 12% range

Approx. biweekly federal withholding: $157

The overtime check triggers $44 more in federal withholding than a regular check. The marginal dollars of overtime income are taxed at 12% federally while the regular income is partially taxed at 10%. This is not a withholding error. It is the progressive federal bracket system working as designed. At year end, the total federal withholding reconciles against your actual annual income, so over-withheld overtime pays come back as a refund.

Ohio state, SDIT, and city taxes work similarly on an annualized basis. Because Ohio's rates are low and most hourly workers are well under the bracket thresholds, the overtime effect on Ohio taxes is minimal compared to federal.

If you want to reduce over-withholding from overtime peaks, ask your employer's payroll department about the IRS flat supplemental rate method (22% flat on supplemental wages). Some payroll systems can apply this for overtime pay if requested, though not all employers offer it.

For workers considering whether to increase pre-tax 401k contributions to offset the tax impact of regular overtime, the Roth IRA Contribution Calculator shows how your gross income level affects Roth eligibility, which is relevant if overtime is pushing your annual gross above the Roth phase-out thresholds.

Ohio state income tax on an hourly paycheck depends on your annual gross. The first $26,050 of taxable income is taxed at 0%, so a $15/hr full-time worker earning $31,200 pays approximately $122 per year in Ohio state income tax, just 0.39% effective rate. A $25/hr worker earning $52,000 pays approximately $694 per year, an effective rate of 1.34%. Ohio also deducts a $20 personal exemption credit directly from the tax owed. The Ohio Paycheck Calculator shows exact per-paycheck withholding.

Ohio taxes overtime pay at the same rates as regular pay. The first $26,050 of total annual income (including overtime) is exempt, and wages above that are taxed at 2.75%. Federal withholding on overtime may appear higher on individual paychecks because employers annualize each check to determine the withholding rate. A large overtime check gets treated as if that income level continued all year, pushing more into higher federal brackets temporarily. The excess withholding is reconciled when you file your annual return.

Ohio's school district income tax (SDIT) is levied by individual school districts on residents. Over 200 Ohio districts charge SDIT, with rates from 0.5% to 3.0%. Hourly workers owe SDIT on all wages, including overtime, if they live in a district that levies it. It applies regardless of where you work. Your employer should withhold it if you provided your school district number on the Ohio IT-4 form. If they did not withhold, you still owe the amount when filing your Ohio return.

Yes. Columbus charges a 2.5% municipal income tax on wages earned within city limits. At $20/hr ($41,600 annual), that is $1,040 per year, or $40 per biweekly paycheck. Workers who live in a Columbus suburb may also owe their suburb's resident rate, though Columbus allows a partial resident credit that reduces double taxation. The Columbus city tax alone exceeds Ohio state income tax for most hourly workers earning under $30/hr.

A $20/hr Ohio worker on a biweekly schedule earns $1,600 gross per paycheck. In Columbus with typical SDIT, take-home is approximately $1,285 per biweekly paycheck after federal income tax ($113), FICA ($122), Ohio state tax ($16), and city plus SDIT ($64). Without city or SDIT taxes, such as a rural Ohio worker, take-home rises to approximately $1,348 per biweekly paycheck. The exact amount varies with filing status, dependents, and pre-tax deductions.

Ohio's state minimum wage for 2025 is $10.45 per hour for non-tipped employees (updated annually based on the Consumer Price Index). At $10.45/hr working 2,080 hours per year, gross annual earnings are $21,736, which falls entirely within Ohio's zero-rate income tax bracket. Minimum wage workers in Ohio owe no Ohio state income tax on those earnings. They may still owe SDIT and municipal tax depending on where they live and work.

Written by

Hassaan Rasheed

Web Developer & Content Researcher

Hassaan builds calculators and writes research-backed guides on finance, math, payroll, and construction topics. Every number in his articles is sourced from official data and worked through by hand.

View LinkedIn Profile