Ohio School District Income Tax (SDIT): Rates, Types, and How to Find Yours (2025-26)

Ohio SDIT explained: 210+ districts levy 0.5% to 2.5% based on where you live. Traditional vs. Earned Income types, top district rates, and what to do if not withheld.

Most people moving to Ohio expect to deal with federal taxes and state income tax. The line that surprises them is the third one on their first Ohio paystub: School District. It is not a rounding error. Ohio is one of a small number of states that lets individual school districts levy their own income tax on residents, and more than 210 districts do exactly that.

The school district income tax (SDIT) is entirely separate from Ohio state income tax and from any municipal tax your city charges. It can add anywhere from 0.5% to 2.5% to your annual tax bill, and because it is based on where you live rather than where you work, your employer may not automatically withhold it. If they do not, you still owe it when you file your Ohio return. Use the Ohio Paycheck Calculator to see how SDIT stacks with state and city taxes in your specific situation.

What Ohio School District Income Tax Is and Why It Exists

Ohio school districts are funded through a combination of property taxes and, in districts that vote to levy it, the SDIT. The tax requires voter approval to implement, which is why not every Ohio school district charges it. Once approved, it applies to all residents within the district boundaries regardless of whether they have children in the school system.

The SDIT is administered by the Ohio Department of Taxation, not by the school district itself. Employers remit SDIT withholding to the state, which then distributes it to the appropriate districts. This means you use your school district number on the Ohio IT-4 withholding form, not the district name.

Three things make SDIT different from every other Ohio tax:

- Residence-based: SDIT applies where you live, not where you work. A Columbus city employee living in a Westerville school district owes Westerville's SDIT, not Columbus's.

- Applies to non-wage income in many districts: Depending on district type, SDIT can reach investment income, interest, dividends, and pension distributions, not just wages.

- Easy to miss: If your IT-4 does not include your school district number, some employers will not withhold it. The liability exists either way.

Traditional SDIT vs. Earned Income SDIT: Which Type Does Your District Use

This distinction is the part that catches the most people off guard, and no paycheck calculator tool covers it in detail. Ohio school districts use one of two tax base types, and they produce very different results for people with investment income, pensions, or retirement distributions.

Traditional SDIT (most common)

Traditional SDIT applies to Ohio taxable income, which is the same income base used for Ohio state income tax. This includes:

- Wages, salaries, and tips

- Self-employment income

- Interest and dividends

- Capital gains

- Pension distributions

- IRA and 401(k) withdrawals

- Rental income

For W-2 workers with no other income, traditional SDIT functions like a simple percentage of wages. For retirees drawing pensions or investment income, it applies to all of it.

Earned Income Tax (EIT)

The Earned Income Tax base is narrower. It applies only to:

- Wages and salaries

- Net self-employment income

It excludes pensions, Social Security, investment income, interest, dividends, and capital gains entirely.

Why this matters in practice:

A retiree living in a Traditional SDIT district at 1.5% with $60,000 in pension income owes $900 in SDIT that year. The same retiree in an Earned Income Tax district at the same rate owes $0 on that pension income, since pensions are excluded from the EIT base.

For W-2 workers, the distinction rarely changes the outcome. Both types tax wages. The difference only surfaces when income comes from sources other than employment.

To check which type your district uses, look up your school district in the Ohio Department of Taxation's SDIT rate table, which lists each district and its tax type alongside its rate. Because SDIT stacks directly on top of city income tax, the Ohio city income tax guide covers the municipal layer that runs alongside your school district obligation.

How to Find Your School District Number and Rate

Ohio assigns a 4-digit code to each school district. You need this code to complete the Ohio IT-4 form so your employer withholds correctly, and to file the Ohio SD 100 return separately from your IT 1040.

How to find your district:

The Ohio Department of Taxation maintains a searchable lookup at tax.ohio.gov. Enter your address and it returns your school district name, code number, tax rate, and whether it uses the Traditional or Earned Income Tax base.

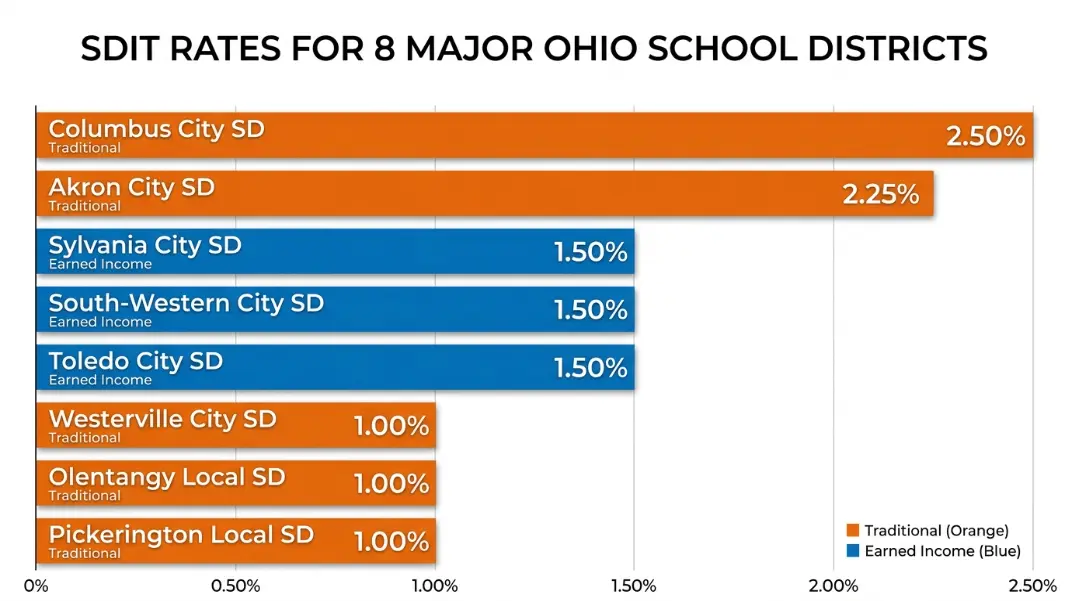

The following table lists the largest Ohio school districts that levy SDIT, with their 2025-26 rates:

| School District | District Code | Type | Rate |

|---|---|---|---|

| Columbus City SD | 2503 | Traditional | 2.50% |

| Cleveland Municipal SD | 1803 | Earned Income | 1.50% |

| Cincinnati City SD | 3103 | Traditional | 0.00% (no SDIT) |

| South-Western City SD (Columbus suburbs) | 2511 | Traditional | 1.50% |

| Hilliard City SD | 2510 | Traditional | 0.75% |

| Dublin City SD | 2506 | Traditional | 0.00% (no SDIT) |

| Westerville City SD | 2514 | Traditional | 1.00% |

| Olentangy Local SD | 2104 | Traditional | 1.00% |

| Pickerington Local SD | 2307 | Traditional | 1.00% |

| Toledo City SD | 4807 | Earned Income | 1.50% |

| Akron City SD | 7703 | Earned Income | 2.25% |

| Dayton City SD | 5703 | Earned Income | 0.50% |

| Strongsville City SD | 1830 | Traditional | 0.00% (no SDIT) |

| Lakota Local SD (Cincinnati suburbs) | 8306 | Earned Income | 1.00% |

| Sylvania City SD (Toledo suburbs) | 4811 | Earned Income | 1.50% |

A few things the table shows: Cincinnati's major city school district charges no SDIT, while Columbus at 2.5% is among the highest. Suburban districts around Columbus like Olentangy and Pickerington charge 1.0%. Akron's district charges 2.25% on earned income only, which is high but does not touch retirement income.

What Happens If Your Employer Does Not Withhold SDIT

Employers are only required to withhold SDIT if the employee has provided their school district number on the Ohio IT-4 form. If you omit the code or fill out a federal W-4 but not an Ohio IT-4, your employer has no basis to withhold.

The tax obligation does not go away. Ohio requires residents in SDIT districts to file a separate SD 100 return alongside their IT 1040. The SD 100 calculates the SDIT owed and any credit for amounts already withheld.

When you might owe SDIT at filing and not expect it:

- You moved to Ohio mid-year from another state and did not update your IT-4

- You changed addresses within Ohio and your new address is in a different school district

- You started a new job and submitted a federal W-4 but not an Ohio IT-4

- Your employer is not set up to withhold for your specific district (some smaller employers)

- You are self-employed or a 1099 contractor with no employer withholding at all

Penalties for not paying:

Underpayment of SDIT is subject to interest and penalties in the same way as Ohio state income tax. The rate tracks Ohio's quarterly interest rate. For most workers, the risk is an unexpected bill at filing plus interest; it is not usually large enough to trigger major penalties unless years of non-filing accumulate.

The fix is straightforward: file an Ohio IT-4 with your employer that includes your school district number. If you are self-employed, make estimated SDIT payments using the Ohio SD 100-ES form on the same quarterly schedule as your state income tax estimates. The Federal Income Tax Calculator helps you model your total combined federal, state, and local burden when planning estimated payments.

How SDIT Stacks with State and City Tax: Full Burden at $60,000 and $90,000

SDIT is the third layer in Ohio's income tax structure. State tax, municipal tax, and SDIT each run independently and stack directly. The Ohio paycheck calculator guide covers the state and city layers in detail; this section shows how SDIT changes the combined picture.

These scenarios use a single W-2 employee with no pre-tax deductions, standard exemptions, and no investment income.

Columbus resident in Columbus City School District (code 2503, 2.5% Traditional SDIT):

Annual salary $60,000:

| Tax Component | Calculation | Amount |

|---|---|---|

| Federal income tax | Approx. standard W-4 withholding | $6,494 |

| FICA (SS + Medicare) | $60,000 × 7.65% | $4,590 |

| Ohio state tax (2025) | ($60,000 - $26,050) × 2.75% - $20 | $914 |

| Columbus city tax | $60,000 × 2.50% | $1,500 |

| Columbus City SD SDIT | $60,000 × 2.50% | $1,500 |

| Total withheld | $14,998 | |

| Take-home | $45,002 | |

| Combined state/local effective rate | ($914 + $1,500 + $1,500) / $60,000 | 6.52% |

Annual salary $90,000:

| Tax Component | Calculation | Amount |

|---|---|---|

| Federal income tax | Approx. standard W-4 withholding | $11,894 |

| FICA | $90,000 × 7.65% | $6,885 |

| Ohio state tax (2025) | ($90,000 - $26,050) × 2.75% - $20 | $1,739 |

| Columbus city tax | $90,000 × 2.50% | $2,250 |

| Columbus City SD SDIT | $90,000 × 2.50% | $2,250 |

| Total withheld | $25,018 | |

| Take-home | $64,982 | |

| Combined state/local effective rate | ($1,739 + $2,250 + $2,250) / $90,000 | 6.93% |

Same salary, suburban Columbus (Olentangy SD, 1.0% Traditional, no city tax):

At $60,000: Ohio state $914 + no city tax + $600 SDIT = $1,514 combined state/local (2.52%) At $90,000: Ohio state $1,739 + no city tax + $900 SDIT = $2,639 combined state/local (2.93%)

The SDIT and city tax together account for most of the difference between living in Columbus proper versus the suburbs. A Columbus city resident at $90,000 pays roughly $4,500 more per year in combined state and local taxes than a suburban Olentangy resident at the same salary, driven almost entirely by city and school district taxes rather than the Ohio state rate itself.

Ohio school district income tax (SDIT) is a local tax levied by individual school districts on people who live within their boundaries. Over 210 Ohio school districts charge SDIT in 2025-26, with rates ranging from 0.5% to 2.5%. It is separate from Ohio state income tax and from any municipal tax your city charges. SDIT applies based on where you live, not where you work, and some employers only withhold it if you provide your district number on the Ohio IT-4 form.

Traditional SDIT applies to all Ohio taxable income, including wages, pensions, investment income, and capital gains. Earned Income Tax applies only to wages and net self-employment income, exempting pensions, Social Security, dividends, and investment income. For W-2 workers, both types produce similar results. For retirees with pension or investment income, the distinction is significant: a Traditional SDIT district at 1.5% taxes a $60,000 pension for $900, while an Earned Income Tax district at the same rate charges nothing on that pension.

Use the address lookup tool on the Ohio Department of Taxation website at tax.ohio.gov. Enter your home address and it returns your school district name, 4-digit code number, current tax rate, and the tax type (Traditional or Earned Income). You need this 4-digit code to complete the Ohio IT-4 withholding form and to file the SD 100 return. Your district code is tied to your home address, so update it any time you move within Ohio.

You still owe the tax. Employers withhold SDIT only if you have provided your school district number on the Ohio IT-4. If you did not, your employer has no code to withhold against, but your liability as a resident of the district exists regardless. File the Ohio SD 100 return with your annual Ohio return to calculate and pay any SDIT owed. Underpayment accrues interest at Ohio's standard rate. If you expect to owe more than $500 in SDIT, you should make quarterly estimated payments using the SD 100-ES to avoid interest charges.

Columbus City School District (code 2503) charges 2.5% Traditional SDIT, one of the highest rates in the state. Akron City School District charges 2.25% Earned Income Tax. Several urban and suburban districts around Columbus, Cleveland, and Toledo charge 1.5% to 2.0%. Many suburban and rural districts either charge lower rates (0.5% to 1.0%) or have no SDIT at all. Cincinnati City School District, Dublin City School District, and Strongsville City School District levy no SDIT.

SDIT is based on where you live, not where you work. If you work from home, you owe SDIT to your home school district regardless of where your employer is located or which city you would otherwise commute to. This is different from Ohio city income tax, where remote work can shift the tax obligation from the employer's city to your home municipality. For SDIT purposes, your home address is the only address that matters.

Written by

Hassaan Rasheed

Web Developer & Content Researcher

Hassaan builds calculators and writes research-backed guides on finance, math, payroll, and construction topics. Every number in his articles is sourced from official data and worked through by hand.

View LinkedIn Profile