Ohio City Income Tax: Dual-City Workers, Resident Credits, and JEDD Zones (2025-26)

Ohio city income tax guide: rates for Columbus, Cleveland, Cincinnati, Toledo. How the resident credit works when you live in one city and work in another.

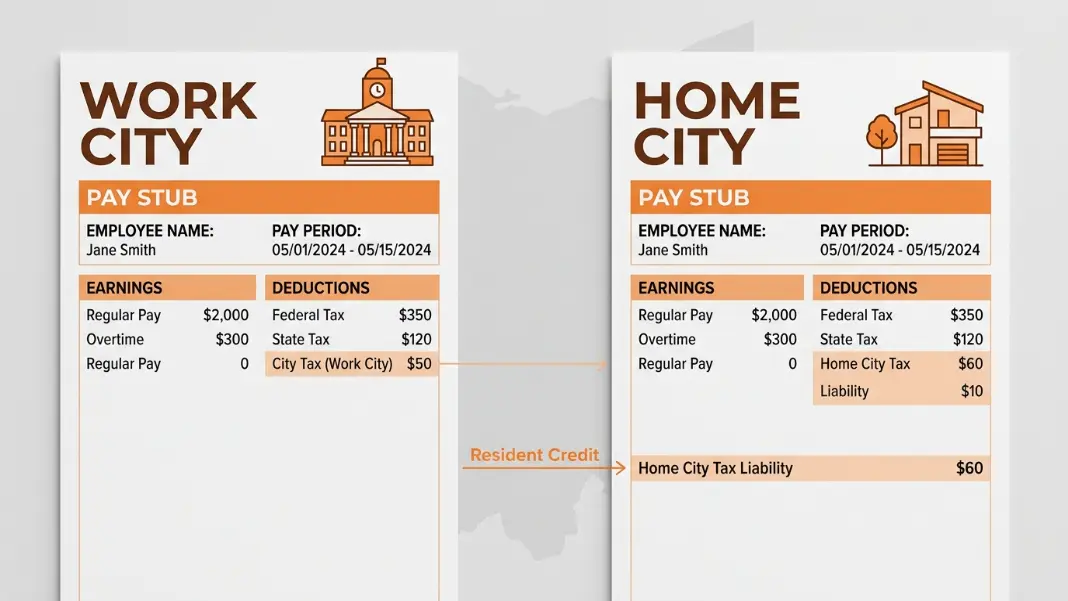

Here is something Ohio does not explain clearly when you take a new job: if you live in a city that charges 2.5% income tax and your office is in a suburb that charges 1%, your tax bill is not 1%. It is 2.5%. The suburb withholds 1% from your paycheck. Your home city wants the other 1.5% when you file your return. The resident credit only works in one direction, and most new Ohio workers learn this when they get an unexpected balance due.

Ohio has more than 600 municipalities that levy a local income tax. Rates range from 0.5% to 3%. Unlike most states, Ohio runs this system in parallel with both state income tax and school district income tax, meaning a Columbus resident working downtown can be paying three separate Ohio income taxes simultaneously. The Ohio Paycheck Calculator handles the full stacking calculation for any salary, city, and district combination. This guide covers how the city tax mechanics actually work, the resident credit rules that most paycheck tools skip over, and the JEDD zones that can add tax at a worksite address nobody expects.

How Ohio Municipal Income Tax Works

Ohio cities levy income tax on wages earned within city limits, regardless of where the employee lives. This is the work city tax. Separately, most cities also levy a tax on their residents, regardless of where those residents work. This is the home city tax.

The employer always withholds for the work city. What you owe your home city depends on the rate difference and the resident credit your home city allows.

Key rules:

- Work city tax is withheld by your employer and applies to wages earned at that location

- Home city tax applies to all income earned by residents, including income earned in other cities

- The resident credit is the mechanism that prevents double taxation; it reduces what you owe your home city by some or all of what you already paid the work city

- Most Ohio municipalities provide a 100% resident credit up to their own tax rate

- Some smaller municipalities cap the credit at a rate lower than their own tax rate; check your specific city ordinance

Major Ohio City Tax Rates for 2025-26

Ohio cities set their own rates through local ordinances. The following covers the major cities and their current rates:

| City | Tax Rate | Credit for Taxes Paid to Work City |

|---|---|---|

| Columbus | 2.50% | 100% up to 2.50% |

| Cleveland | 2.00% | 100% up to 2.00% |

| Cincinnati | 1.80% | 100% up to 1.80% |

| Toledo | 2.25% | 100% up to 2.25% |

| Akron | 2.25% | 100% up to 2.25% |

| Dayton | 2.50% | 100% up to 2.50% |

| Parma | 2.50% | 100% up to 2.50% |

| Canton | 2.50% | 100% up to 2.50% |

| Lorain | 2.50% | 100% up to 2.50% |

| Hamilton | 2.00% | 100% up to 2.00% |

| Youngstown | 2.75% | 100% up to 2.75% |

| Mansfield | 2.00% | 100% up to 2.00% |

Suburbs and smaller municipalities typically charge 1% to 2%. Some charge nothing. The rate for any specific address is verifiable using the Ohio Department of Taxation's Finder tool at tax.ohio.gov. Most Ohio residents also owe a school district income tax on top of city tax; the Ohio school district income tax guide covers which districts charge it and how the two layers stack.

The Resident Credit: How to Avoid Paying Tax to Two Cities

The resident credit is the most misunderstood part of Ohio city taxation. Understanding it correctly determines whether you have a surprise bill at filing or a clean return.

Scenario 1: Live in lower-rate city, work in higher-rate city

You live in Westerville (1.0% rate) and work in Columbus (2.5% rate).

- Your employer withholds 2.5% for Columbus on all wages earned in Columbus

- Westerville allows a 100% credit for taxes paid to Columbus, up to Westerville's own 1.0% rate

- You owe Westerville 1.0%, but you receive a credit for 1.0% already paid to Columbus

- Net owed to Westerville: $0

- Total city tax paid: 2.5% to Columbus only

This is the scenario most people assume always applies. It does, when the work city rate is higher than the home city rate.

Scenario 2: Live in higher-rate city, work in lower-rate city

You live in Columbus (2.5% rate) and work in a suburb with a 1.0% rate.

- Your employer withholds 1.0% for the suburb

- Columbus allows a credit for taxes paid to the suburb, up to 2.5%

- The credit is 1.0% (what you paid the suburb)

- You still owe Columbus the remaining 1.5% on that income

- Net city tax paid: 1.0% (suburb) + 1.5% (Columbus) = 2.5% total

Columbus residents working in lower-rate suburbs always pay Columbus's full 2.5% rate. The suburb gets 1.0% via employer withholding; Columbus gets the rest when you file. Many Columbus residents working in Dublin, Westerville, or other suburbs discover this when they file their first Columbus city return.

Scenario 3: Work city has no income tax

You live in Columbus (2.5%) and work remotely from home or in a municipality with no income tax.

- No employer withholding for a work city

- Columbus taxes all wages at 2.5%

- Your employer should be withholding Columbus tax directly since your work location is Columbus

This changed significantly after 2020. Ohio ruled in 2021 that municipalities can only tax employees for days actually worked within city limits, not days worked remotely from home in a different municipality. Columbus residents working remotely owe Columbus for their remote days, not their employer's city.

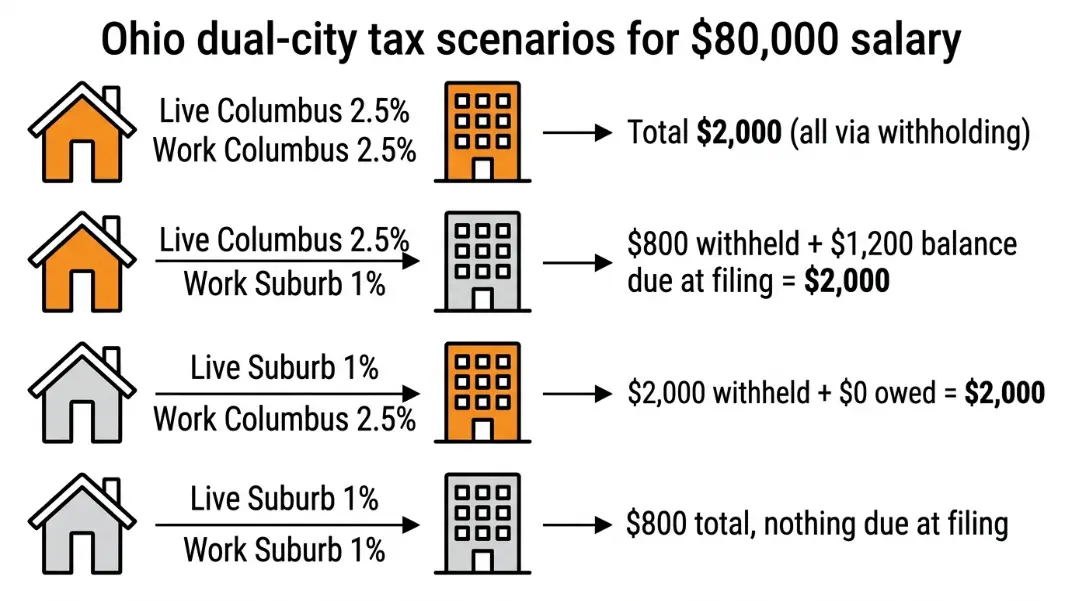

Worked example at $80,000:

| Scenario | Work City Tax | Home City Tax | Total |

|---|---|---|---|

| Live Columbus (2.5%), work Columbus | $2,000 | $0 (all paid) | $2,000 |

| Live Columbus (2.5%), work suburb (1%) | $800 | $1,200 (balance due) | $2,000 |

| Live suburb (1%), work Columbus (2.5%) | $2,000 | $0 (credit covers) | $2,000 |

| Live suburb (1%), work suburb (same) | $800 | $0 | $800 |

The total city tax only differs when both home and work city have different rates. Living in a 1% suburb and working in Columbus still costs the same as living in Columbus and working in Columbus: 2.5% either way.

JEDD and JEDZ Zones: The Ohio Tax Layer Nobody Explains

Joint Economic Development Districts (JEDD) and Joint Economic Development Zones (JEDZ) are a tax structure unique to Ohio that almost no payroll guide mentions. If your office is inside a JEDD zone, you may be paying a municipal-style income tax to a zone that is technically outside any city, and neither you nor your employer may have realized it.

What a JEDD is:

A JEDD is an agreement between a township (which normally cannot levy income tax) and an adjacent municipality. The township contributes land, the municipality contributes taxing authority, and both share the resulting revenue. The result is that employment within the JEDD boundary is subject to income tax at the JEDD rate, even though the worksite address might appear to be in an unincorporated township.

The tax is collected by the partner municipality and remitted to both parties according to the revenue-sharing formula in the JEDD agreement.

What this means for your paycheck:

If your employer is located in a JEDD, you pay the JEDD rate just as you would pay a city tax. The JEDD rate is typically set at the partner municipality's rate (often 2.0% to 2.5%). This means a worker in a suburban Ohio office park might owe 2.0% to a JEDD without any indication from their address that they are in a taxing jurisdiction.

JEDZ (Joint Economic Development Zone) is a similar but slightly different structure involving two adjacent townships rather than a township and a municipality.

How to check if your worksite is in a JEDD:

Use Ohio's Finder tool at tax.ohio.gov. Enter the worksite address. If it is in a JEDD, the tool identifies it and shows the applicable tax rate and the collecting municipality. Your employer's payroll system should have this configured, but if you suspect your paystub is not reflecting a JEDD rate, verify the address directly.

Why this matters:

Workers who look up the city tax rate for their suburb and find "no municipal tax" sometimes overlook that their specific office park address is inside a JEDD with a 2.0% rate. The discrepancy only surfaces when the SD 100 or city return shows a balance due that the employee cannot explain.

For employers running payroll for Ohio locations, JEDD membership changes withholding obligations. The Ohio Paycheck Calculator applies JEDD rates when you enter the employer's exact tax jurisdiction code.

Remote Work in Ohio: Which Municipality Gets Your Tax Post-2020

Ohio's Hicks v. Testa litigation and the resulting 2021 municipal income tax reform changed how remote work is taxed. The pre-2020 system allowed cities to tax employees for all days paid, even days worked at home in a different municipality. That is no longer valid.

Current rules for remote workers:

- Tax owed to a municipality is based on days worked physically within that municipality

- Remote days worked from home are taxed by the home municipality, not the employer's city

- Employers are required to track and allocate wages by actual work location

- Some employers use a proportional method based on logged days; others require employees to document remote vs. in-office days on an annual allocation

Practical example:

You work 3 days per week in Columbus (2.5%) and 2 days per week remotely from your home in Hilliard (no municipal income tax). Your salary is $75,000.

- Days worked in Columbus: 60% of working days

- Days worked in Hilliard: 40%

- Wages allocated to Columbus: $75,000 × 60% = $45,000; city tax = $1,125

- Wages allocated to Hilliard: $75,000 × 40% = $30,000; city tax = $0

- Total city tax: $1,125

Under the pre-2021 rule, Columbus would have claimed all $75,000 and collected $1,875. The shift saves $750 per year for this employee.

Workers in this situation should keep a log of in-office versus remote days throughout the year to support the allocation at filing. The Columbus city return and the RITA (Regional Income Tax Agency) filing for multi-municipality workers both support the day-count allocation method.

RITA administers municipal taxes for more than 350 Ohio municipalities. If you work in multiple RITA municipalities, a single RITA return covers all of them instead of separate filings. Non-RITA cities like Columbus require their own separate return.

The New York, New Jersey, Indiana, and Michigan Paycheck Guide shows how Ohio's multi-layer local tax structure compares to flat-rate states where local taxes are simpler or absent entirely.

Ohio cities levy income tax on wages earned within city limits. Employers withhold city tax based on the work location. If you also live in a city with income tax, your home city may want a portion of your wages as well. The resident credit reduces double taxation: your home city credits taxes already paid to your work city up to the home city's own rate. If your work city rate is lower than your home city rate, you owe your home city the difference at filing.

Columbus charges a 2.5% income tax on wages earned within city limits and on all income of Columbus residents. Columbus provides a 100% resident credit for income taxes paid to other Ohio municipalities, up to 2.5%. A Columbus resident working in a suburb with a 1% rate owes Columbus the remaining 1.5% at filing. A Columbus resident working in Columbus pays the full 2.5% through employer withholding with no additional filing required.

A JEDD (Joint Economic Development District) is a tax zone formed between an Ohio township and an adjacent municipality. Because townships cannot independently levy income tax, they partner with a city to share taxing authority over employment within the JEDD boundary. Workers inside a JEDD pay the JEDD income tax rate, which is typically set at the partner municipality's rate. JEDD zones often cover commercial and industrial areas that look like unincorporated suburbs but carry a municipal-level income tax obligation.

Yes, but to your home municipality, not your employer's city. Since Ohio's 2021 municipal tax reform, cities can only tax workers for days physically worked within their boundaries. Remote days worked from home shift the tax obligation to your home municipality. If your home municipality charges income tax, that rate applies to your remote days. If it charges no income tax, those remote days carry no local tax obligation. Keep a log of in-office versus remote days to support any allocation at filing.

You do not avoid the total tax, but you avoid true double taxation through the resident credit. If you pay city tax to your work city, your home city credits that payment against your home city liability up to the home city's own rate. The result is that you pay whichever rate is higher, not both rates added together. The only situation where you owe both cities is when your work city rate is lower than your home city rate; in that case, you pay the work city's rate through withholding and your home city's excess at filing.

RITA (Regional Income Tax Agency) is a centralized tax agency that administers municipal income taxes for more than 350 Ohio municipalities. If you work or live in RITA-member cities, you can file a single RITA return that covers all of them instead of separate returns to each municipality. RITA handles withholding administration, audits, and collections for its member cities. Non-RITA cities like Columbus administer their own returns. Check RITA's website at ritaohio.com to see if your city is a member.

Written by

Hassaan Rasheed

Web Developer & Content Researcher

Hassaan builds calculators and writes research-backed guides on finance, math, payroll, and construction topics. Every number in his articles is sourced from official data and worked through by hand.

View LinkedIn Profile