FERS Supplement Calculator: What You Get Before Age 62 (2025-26)

FERS supplement calculator guide: who qualifies, how to calculate the amount, earned income test, sick leave credit, and when the supplement stops at 62.

Most federal employees spend the last few years of their career wondering how to replace Social Security income before they turn 62. The FERS supplement calculator answers that question with a concrete monthly number. Running those numbers before you finalize your retirement date gives you enough lead time to adjust your savings plan, manage part-time work carefully, and avoid the earned income trap that catches many retirees off guard.

The FERS supplement is a monthly payment from OPM that approximates what you would receive from Social Security at age 62. It starts when you retire and stops the month you turn 62. Not every FERS employee qualifies, and the amount depends on two factors you can control: your years of creditable service and how long you accumulate sick leave. Use the FERS Supplement Calculator to get a fast estimate while you read through the details below.

What the FERS Supplement Is and Who Qualifies

The FERS supplement, officially called the Special Retirement Supplement (SRS), is a separate monthly payment that bridges the income gap between your FERS retirement date and age 62, when Social Security benefits become available. OPM pays it directly alongside your regular annuity check. The supplement is not Social Security and does not affect your future Social Security benefit amount.

Qualification requires an immediate, unreduced FERS annuity before age 62. There are four paths:

- MRA (age 57 for employees born in 1970 or later, age 56 for those born 1953-1964) with 30 or more years of creditable service

- Age 60 with 20 or more years of creditable service

- VERA (Voluntary Early Retirement Authority, offered by your agency): age 50 with 20 years, or any age with 25 years of service

- Employees who retire due to discontinued service (involuntary separation)

The following groups are not eligible, regardless of years of service:

- MRA+10 retirees (retirement at MRA with 10-29 years)

- Disability retirees

- Deferred retirees (those who separated before reaching retirement age)

- Retirees who postpone their annuity start date to avoid the MRA+10 penalty

The distinction between a full-MRA retirement and an MRA+10 retirement matters more than most employees realize. Both happen at the same age, but the service requirement determines which bucket you fall into. Thirty years at MRA means you get the supplement. Twenty years at MRA means you qualify for MRA+10 only, and there is no supplement.

How to Calculate Your FERS Supplement Amount

The FERS supplement is calculated using a prorated Social Security formula. OPM estimates what your Social Security benefit would be at age 62 based on your full earnings history, then multiplies that figure by the ratio of your FERS civilian service to 40 years.

The formula:

FERS Supplement = (Years of Creditable Service / 40) x Estimated SS Benefit at Age 62

Your estimated Social Security benefit at 62 comes from your Social Security Statement, available at ssa.gov. Use the age-62 figure specifically, not the age-67 or age-70 figure.

Worked example 1:

An employee retires at MRA with 30 years of creditable service. Their Social Security statement shows an estimated benefit of $1,600/month at age 62.

FERS Supplement = (30 / 40) x $1,600

= 0.75 x $1,600

= $1,200/month

Worked example 2:

An employee retires at age 60 with 35 years of service. Their estimated SS benefit at 62 is $1,900/month.

FERS Supplement = (35 / 40) x $1,900

= 0.875 x $1,900

= $1,663/month

The table below shows estimated supplement amounts across common service lengths and Social Security benefit levels. These figures assume no sick leave credit additions and no earned income reduction.

| Years of Service | SS Benefit $1,400/mo | SS Benefit $1,800/mo | SS Benefit $2,200/mo |

|---|---|---|---|

| 25 years | $875/month | $1,125/month | $1,375/month |

| 28 years | $980/month | $1,260/month | $1,540/month |

| 30 years | $1,050/month | $1,350/month | $1,650/month |

| 33 years | $1,155/month | $1,485/month | $1,815/month |

| 35 years | $1,225/month | $1,575/month | $1,925/month |

Most employees aiming for an MRA retirement at 57 will land in the 30-33 year service range. At a $1,800 estimated SS benefit, that produces a supplement between $1,350 and $1,485 per month before any earned income reduction applies.

For a complete retirement income picture that includes both your annuity and supplement, the FERS Retirement Calculator lets you model all three income streams together.

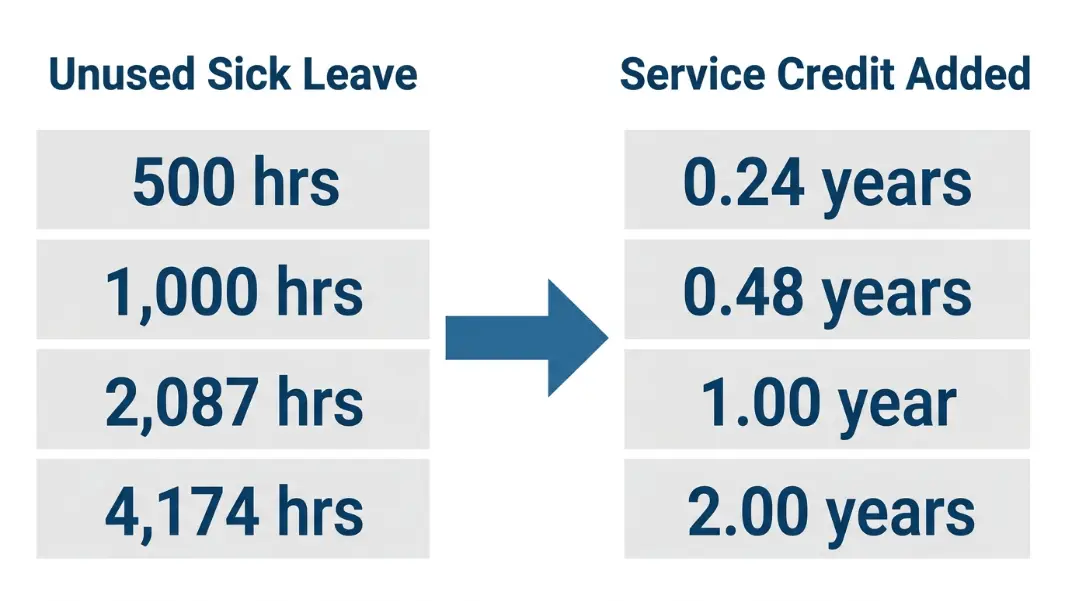

How Sick Leave Converts to Service Credit in FERS

Unused sick leave adds directly to your years of creditable service when OPM calculates your FERS supplement. Since January 1, 2014, FERS employees receive 100% credit for unused sick leave, not the 50% that applied previously. Every hour you did not use becomes part of your service calculation.

OPM uses a standard federal work year of 2,087 hours to convert sick leave balances into service credit. Divide your unused hours by 2,087 to get the fractional years to add to your service total.

The conversion table below shows how common sick leave balances translate into service credit.

| Unused Sick Leave Hours | Service Credit Added |

|---|---|

| 500 hours | 0.240 years |

| 1,000 hours | 0.479 years |

| 1,500 hours | 0.719 years |

| 2,000 hours | 0.958 years |

| 2,087 hours | 1.000 year |

Here is how sick leave affects the supplement in practice. Take an employee with 30 years of service, an estimated SS benefit of $1,600/month at 62, and 2,087 hours of unused sick leave at retirement.

Before sick leave credit:

(30 / 40) x $1,600 = $1,200/month

After sick leave credit (30 + 1 year = 31 effective years):

(31 / 40) x $1,600 = $1,240/month

The sick leave adds $40/month to the supplement. Over a five-year bridge period to age 62, that is $2,400 in total additional income from sick leave you chose not to use. The math compounds further if your sick leave balance is higher. An employee with 4,174 hours (exactly two years) would gain $80/month, or $4,800 over five years.

One important boundary: sick leave credit does count toward the service total used in the supplement formula, but it does not count toward the years needed to qualify for retirement in the first place. You cannot use sick leave to reach the 30-year or 20-year service thresholds for eligibility. You must already be eligible before the sick leave credit applies.

To see how your leave balance affects both your annuity and supplement simultaneously, visit How to Calculate FERS Retirement for a step-by-step walkthrough that covers the annuity formula alongside sick leave credit.

The Earned Income Test: How Outside Work Reduces Your Supplement

The earned income test reduces your FERS supplement by $1 for every $2 you earn above a threshold. In 2025, that threshold is $22,320 per year. If your earned income stays below that number, the supplement is not reduced at all.

This rule mirrors how Social Security handles benefits for people who claim early while still working. OPM applies it to the FERS supplement starting in the calendar year after the one in which you retired. The first year of retirement is exempt from the test.

What counts as earned income:

- Wages and salaries from an employer

- Net income from self-employment

What does not count:

- FERS annuity payments

- Investment income, dividends, or capital gains

- Rental income

- Social Security benefits

- Pension income from other sources

- IRA or TSP distributions

Worked example:

An employee retires with a FERS supplement of $1,200/month ($14,400/year). In the following calendar year, they take a part-time consulting job and earn $35,000.

Earned income: $35,000

Threshold: $22,320

Excess: $35,000 - $22,320 = $12,680

Reduction: $12,680 / 2 = $6,340/year = $528/month

New supplement: $1,200 - $528 = $672/month

The part-time work reduced the supplement by 44 percent. If the consulting income had been $22,319, the supplement would remain at $1,200/month untouched.

This threshold adjusts annually alongside Social Security cost-of-living changes, so check the current year's figure each January. For 2025, the official figure is $22,320.

The earned income test creates a marginal tax situation worth planning around. If you earn $30,000 in wages, only $7,680 exceeds the threshold, producing a $3,840 annual reduction. But you also owe federal income tax on the supplement itself. The FERS supplement is fully taxable as ordinary income. Use the Federal Income Tax Rate Calculator to estimate how your combined annuity, supplement, and earned income will be taxed before you commit to a consulting arrangement.

OPM requires you to report earned income annually. If you do not report it and OPM later discovers excess earnings, they will recover the overpayment. Staying proactive with annual reporting prevents an unexpected bill.

FERS MRA+10 Retirement: Why the Supplement Does Not Apply

MRA+10 is a retirement option available to FERS employees who have reached their Minimum Retirement Age with between 10 and 29 years of service. It provides an immediate annuity, but that annuity comes with a significant permanent reduction and no FERS supplement.

How the MRA+10 penalty works:

The annuity is reduced by 5% for each year the employee is under age 62 at the time the annuity begins. Months count proportionally.

Reduction = (62 - age at annuity start) x 5%

Example: Retire at age 57 with 15 years of service

Reduction = (62 - 57) x 5% = 25%

If the base annuity (before reduction) is calculated as:

$85,000 High-3 x 15 years x 1.0% = $12,750/year

After the 25% MRA+10 penalty:

$12,750 x 0.75 = $9,563/year ($797/month)

That reduction is permanent. It does not disappear at age 62. It applies for the life of the annuity.

And critically, there is no FERS supplement alongside it. The combination of a reduced annuity and no supplement makes MRA+10 one of the more financially damaging retirement paths available to FERS employees. The only reason to choose it is if you need income immediately and cannot wait until 60 with 20 years or MRA with 30 years.

The postponed annuity alternative:

Employees who separate at their MRA under MRA+10 rules can postpone the annuity start date to reduce or eliminate the penalty. If you postpone to age 62, the 5% per year reduction disappears entirely. But postponement means no income from OPM during the gap years, and it still means no FERS supplement regardless of when the annuity begins.

Deferred retirement is a related option for employees who separate before reaching MRA. They can wait and claim the annuity at the appropriate age with no reduction if they have at least 5 years of service. But again, no FERS supplement applies to deferred retirees.

The no-supplement rule for MRA+10 and deferred retirees reflects the design intent of the supplement: it exists specifically to replace Social Security income for employees who retire early with a full unreduced annuity and who therefore have the longest gap before Social Security eligibility begins.

When the FERS Supplement Stops

OPM stops the FERS supplement automatically the month the retiree turns 62. This happens regardless of whether you have filed for Social Security, regardless of your employment status, and regardless of how much supplement income you were receiving.

The stop is automatic and does not require any action on your part. OPM tracks your birth date in their records and adjusts payments accordingly.

You must apply for Social Security separately. OPM does not trigger a Social Security application when the supplement ends. Many retirees assume the transition is automatic, but it is not. File with the Social Security Administration three months before you want benefits to begin, which for most people means filing around age 61 and 9 months if you intend to claim at 62.

Planning for the income gap:

The end of the supplement at 62 represents a real monthly income drop unless you either claim Social Security at 62 or have other income sources to cover the gap. The strategy of delaying Social Security to age 67 or 70 for a larger benefit means living without both the supplement and Social Security for several years. Model this carefully before committing to a delayed claim.

One approach is to partially fund the gap with TSP withdrawals. TSP penalty-free withdrawals begin at age 55 for separating employees (not age 59.5 like a traditional IRA), which gives you a useful tool for the bridge period. Coordinate TSP drawdown timing with your supplement end date and Social Security start date to avoid large tax spikes in any single year.

The FERS supplement is taxable income in every year it is received. Budget for estimated quarterly tax payments if your withholding does not automatically cover the supplement amount.

To receive the FERS supplement, you must retire with an immediate, unreduced FERS annuity before age 62. The qualifying paths are: MRA (age 56-57 depending on birth year) with 30 or more years of service; age 60 with 20 or more years; VERA at age 50 with 20 years or any age with 25 years; and involuntary/discontinued service retirement. MRA+10 retirees, disability retirees, and deferred retirees do not qualify.

The formula is: FERS Supplement = (Years of Creditable Service / 40) x Estimated SS Benefit at Age 62. Get your estimated SS benefit at 62 from your Social Security Statement at ssa.gov. For example, 30 years of service with a $1,600 estimated SS benefit produces: (30/40) x $1,600 = $1,200/month. Unused sick leave hours add to your creditable service total before you apply the formula.

The 2025 earned income threshold is $22,320 per year. If your wages or self-employment net income exceed this amount, your supplement is reduced by $1 for every $2 over the limit. For example, earning $35,000 produces excess earnings of $12,680, which reduces the supplement by $6,340 per year ($528/month). Investment income, pension payments, rental income, and Social Security do not count toward the threshold.

Yes. OPM converts unused sick leave hours into additional service credit at a rate of 2,087 hours per year. That credit is added to your years of creditable service before applying the supplement formula. For example, 2,087 hours of sick leave adds one full year, raising a 30-year calculation to 31 years. On a $1,600 estimated SS benefit, that adds $40/month to the supplement, worth $2,400 over a five-year bridge period.

The FERS supplement stops the month you turn 62. OPM ends it automatically based on your birth date on file. The cutoff is not affected by whether you claim Social Security at 62 or delay it to a later age. You must apply to the Social Security Administration separately, typically three months before you want benefits to begin. Budget for the income drop at 62 if you plan to delay Social Security.

No. MRA+10 retirement does not include the FERS supplement under any circumstances. MRA+10 applies to employees who retire at their Minimum Retirement Age with 10 to 29 years of service. In addition to receiving no supplement, MRA+10 retirees face a permanent 5% per year reduction for each year under age 62 unless they postpone the annuity start date. Postponing the annuity eliminates the penalty but still does not add the supplement.

Written by

Hassaan Rasheed

Web Developer & Content Researcher

Hassaan builds calculators and writes research-backed guides on finance, math, payroll, and construction topics. Every number in his articles is sourced from official data and worked through by hand.

View LinkedIn Profile