Illinois, Pennsylvania, Maryland, and Washington Paycheck Tax Guide (2025-26)

Illinois paycheck calculator guide: PA 3.07% flat tax, Maryland county taxes, and Washington state's no-income-tax rules. Take-home pay 2025-26.

Pennsylvania's 3.07% state income tax rate looks like the clear winner of these four states on paper. It is the lowest flat rate in this group. But workers in Philadelphia pay a combined 6.82% in city and state wage taxes before federal, and workers anywhere in Pennsylvania pay a local earned income tax on top of the state rate. The headline rate is only part of the number.

The same gap between rate and reality applies across all four states here. Illinois has no city income tax, which is a genuine advantage over most large-state peers. Maryland stacks a mandatory county piggyback tax on top of its state brackets. Washington eliminated income tax entirely but added two new mandatory payroll deductions since 2023 that most people moving there have not heard of.

The Illinois Paycheck Calculator runs exact take-home numbers for Illinois. This guide covers how each state's system actually works, where the surprises are, and how take-home pay compares at $60,000 and $90,000 across all four states.

How Illinois Taxes Your Paycheck

Illinois uses a flat state income tax rate of 4.95% applied to all taxable income. There are no brackets. A worker earning $45,000 pays the same 4.95% rate as someone earning $145,000.

Illinois provides a personal exemption of $2,425 for the filer, with an additional $2,425 allowed for a spouse and $2,425 per dependent. For a single filer with no dependents, taxable income is gross wages minus $2,425.

How the deductions work at $75,000 gross salary:

- Federal income tax: approximately $8,820 (2025 brackets, standard deduction)

- FICA: $5,738 (6.2% Social Security + 1.45% Medicare)

- Illinois state tax: ($75,000 - $2,425) × 4.95% = $3,592

- Total annual deductions: approximately $18,150

- Annual take-home: approximately $56,850

Illinois does not have a local income tax applicable to most workers. Chicago does not levy a city income tax on wages, which is unusual for a major US city. New York City, Philadelphia, and Columbus all charge additional city-level income tax. Illinois workers in Chicago or the suburbs generally pay only state and federal, with no city layer.

There are a small number of Illinois municipalities with modest local taxes, but they apply to a fraction of the workforce. For the overwhelming majority of Illinois workers, the tax calculation is federal + 4.95% state with the $2,425 exemption.

Illinois also withholds nothing for state unemployment from employee paychecks. The Illinois unemployment tax is paid entirely by employers. That means no SUI line item on an Illinois paystub.

For the complete Illinois tax calculation with your specific income and withholding situation, use the Illinois Paycheck Calculator.

Pennsylvania's 3.07% Rate: Simple on Paper, Complex With Local Tax

Pennsylvania's flat income tax rate of 3.07% applies to all taxable wages with no deductions, no exemptions, and no standard deduction at the state level. Gross wages are taxed directly.

State tax at $75,000: $75,000 × 3.07% = $2,303

Pennsylvania employees also pay a state unemployment (SUI) contribution of 0.07% on the first $10,000 of wages. That is $7 per year, a trivial amount, but it does appear as a line on the paystub.

The part that changes the number significantly is Local Earned Income Tax (EIT). Every Pennsylvania municipality levies an EIT, and unlike the state tax, rates vary widely by location:

| Location | Combined Local EIT Rate |

|---|---|

| Philadelphia (resident) | 3.75% |

| Philadelphia (non-resident, working in city) | 3.44% |

| Pittsburgh (resident) | 3.00% |

| Harrisburg | 1.00% |

| Typical suburban townships | 1.00% |

| Some rural boroughs | 0.50-1.00% |

The 1% local EIT in most suburbs is split between the municipality and school district: typically 0.5% each. Workers pay whichever is higher: their resident rate or the rate of the municipality where they work, depending on which jurisdiction the employer remits to.

Total PA tax at $75,000 in a typical 1% EIT area:

- State: $2,303

- Employee SUI: $7

- Local EIT (1%): $750

- Total state-level: $3,060

In Philadelphia at $75,000:

- State: $2,303

- Employee SUI: $7

- Philadelphia City Wage Tax (resident): $75,000 × 3.75% = $2,813

- Total state-level: $5,123

The Pennsylvania Paycheck Calculator calculates EIT based on your specific location. If your municipality is not listed, use 1% as the standard assumption for suburban areas.

Maryland Paychecks: State Tax Plus County Piggyback on Every Dollar

Maryland uses a progressive state income tax combined with a mandatory county income tax that applies to the same taxable income. Every Maryland resident pays both. The combined rates are among the highest effective rates for middle-income workers in the mid-Atlantic region.

Maryland state income tax brackets (2025, single filer):

| Taxable Income | State Rate |

|---|---|

| Up to $1,000 | 2.0% |

| $1,001 to $2,000 | 3.0% |

| $2,001 to $3,000 | 4.0% |

| $3,001 to $100,000 | 4.75% |

| $100,001 to $125,000 | 5.0% |

| $125,001 to $150,000 | 5.25% |

| $150,001 to $250,000 | 5.5% |

| Over $250,000 | 5.75% |

The standard deduction is 15% of adjusted gross income, with a floor of $1,600 and a cap of $2,450 for single filers.

On top of state tax, every Maryland county and Baltimore City charges an additional income tax on the same taxable income. This is not a separate form or filing: the county tax appears alongside the state tax on your paystub and is calculated on the same base.

County income tax rates (select jurisdictions, 2025):

| County / City | County Rate |

|---|---|

| Baltimore City | 3.20% |

| Montgomery County | 3.20% |

| Prince George's County | 3.20% |

| Howard County | 3.20% |

| Anne Arundel County | 2.81% |

| Baltimore County | 2.83% |

| Frederick County | 2.96% |

| Harford County | 3.06% |

| Cecil County | 2.25% |

The lowest county rate in Maryland is 2.25% (Cecil County). The highest is 3.20% (Baltimore City and several large counties). There is no option to opt out of the county tax as a resident.

Total Maryland tax at $75,000 in a 3.20% county:

- Taxable income: $75,000 - $2,450 deduction = $72,550

- State tax: approximately $3,220 (working through the brackets)

- County tax (3.20%): $72,550 × 3.20% = $2,322

- Total state + county: $5,542

At an effective combined rate of roughly 7.6%, Maryland's income taxes are noticeably heavier than either Illinois (4.95%) or Pennsylvania (3.07% + typical 1% local = ~4.1%). For the precise calculation with your county rate and filing status, the Maryland Paycheck Calculator handles the full bracket math.

Washington State: No Income Tax, but New Mandatory Deductions Since 2023

Washington state has never had a personal income tax, and the state constitution has been interpreted to effectively prohibit a general income tax on wages. Workers moving from Illinois, Pennsylvania, or Maryland to Washington typically see a significant increase in take-home pay for that reason.

What most people do not account for are two newer mandatory payroll deductions that Washington phased in starting in 2023:

1. WA Paid Family and Medical Leave (PFML)

Washington's PFML program provides paid leave for qualifying family and medical events. The total premium is approximately 0.74% of gross wages. For employees at employers with 50 or more workers, the employee pays 71.43% of the premium, or about 0.529% of gross wages. The wage base is tied to the Social Security taxable maximum ($176,100 in 2025).

At $75,000: $75,000 × 0.529% = $397/year

2. WA Cares Fund (Long-Term Care Insurance)

The WA Cares Fund deducts 0.58% of all gross wages with no income cap. Employees pay the full amount. The program provides a lifetime long-term care benefit of $36,500 (indexed for inflation) for eligible residents.

At $75,000: $75,000 × 0.58% = $435/year

Workers who purchased qualifying private long-term care insurance before November 2022 and filed for an exemption before the deadline are not subject to the WA Cares deduction. That exemption deadline has passed; new Washington workers today pay the 0.58% rate.

Total mandatory Washington state deductions at $75,000:

- PFML: $397

- WA Cares: $435

- Total: $832/year, or about $69/month

Compare that to Illinois at $75,000 ($3,592 state tax) or Maryland ($5,542 state + county). Washington's deductions are $2,760 to $4,710 less per year at $75,000. That gap narrows slightly at higher income levels because the WA Cares fund has no wage cap, but it never closes.

Use the Washington State Paycheck Calculator to see the PFML and WA Cares deductions for your specific wage level alongside federal taxes.

Take-Home Pay at $60,000 and $90,000: All Four States Side by Side

These figures use 2025-26 rates, single filing status, no pre-tax retirement deductions, standard deductions where applicable, and typical local tax rates (1% EIT for PA, 3.2% county for MD, no local for IL and WA). Federal income tax and FICA are the same across all four states and are not included in the state-level columns below.

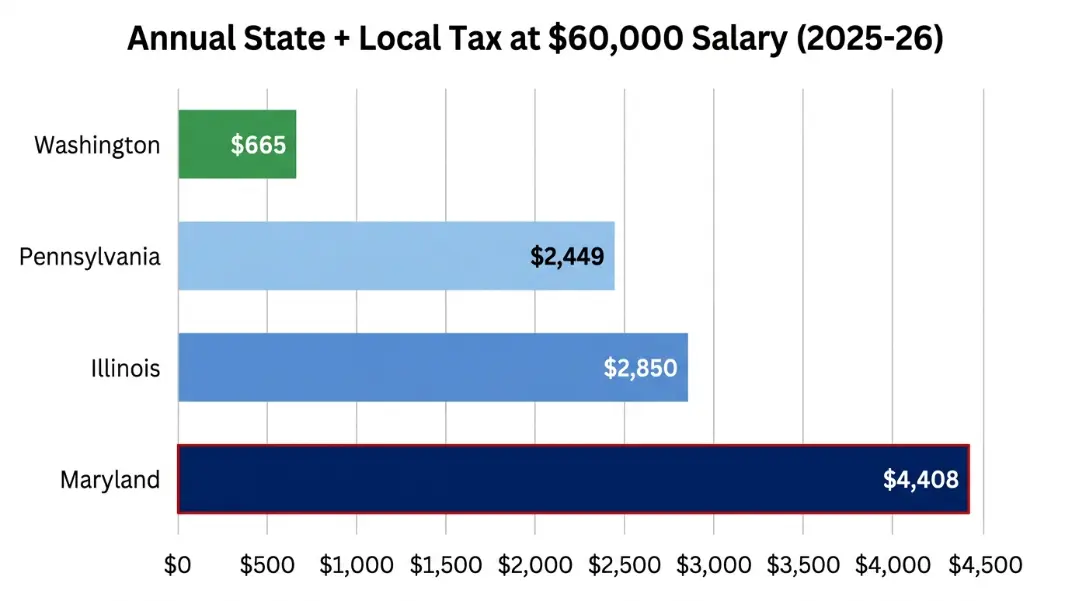

Annual state-level tax at $60,000 gross salary:

| State | Annual State Tax | Annual Local Tax | Total State + Local | Effective Combined Rate |

|---|---|---|---|---|

| Washington | $665 | $0 | $665 | 1.1% |

| Pennsylvania | $1,842 | $600 | $2,449 | 4.1% |

| Illinois | $2,850 | $0 | $2,850 | 4.75% |

| Maryland | $2,681 + county $1,727 | -- | $4,408 | 7.3% |

Annual state-level tax at $90,000 gross salary:

| State | Annual State Tax | Annual Local Tax | Total State + Local | Effective Combined Rate |

|---|---|---|---|---|

| Washington | $998 | $0 | $998 | 1.1% |

| Pennsylvania | $2,763 | $900 | $3,670 | 4.1% |

| Illinois | $4,335 | $0 | $4,335 | 4.82% |

| Maryland | $4,106 + county $2,627 | -- | $6,733 | 7.5% |

A few things the tables confirm:

Washington's advantage holds regardless of income level because the PFML and WA Cares deductions are a nearly flat percentage with no brackets. The benefit of no income tax does not phase out at higher income.

Maryland's rate accelerates with income because the state brackets step up through 4.75% toward 5.75%. Workers earning $150,000+ in a 3.2% county face a combined state + county effective rate above 8.5%.

Pennsylvania's advantage depends heavily on location. The 3.07% state rate genuinely is low. But a Philadelphia resident at $90,000 faces a city wage tax of $3,375 on top of $2,763 in state tax, pushing the combined rate to 6.8%, higher than Illinois for the same income.

Illinois has no bracket risk. The 4.95% flat rate is fixed by the state constitution. A constitutional amendment would be required to add brackets or raise the rate, and voters rejected a graduated income tax amendment in 2020. For workers expecting income growth, that predictability is real.

Illinois withholds 4.95% of taxable wages as state income tax, with a personal exemption of $2,425 for the filer. At $60,000 gross salary, state tax is approximately $2,850 per year ($238/month). FICA (Social Security + Medicare) adds 7.65%, or $4,590 per year. Federal income tax depends on filing status and withholding elections. Most Illinois workers in suburban areas pay no local income tax beyond state and federal.

Pennsylvania's state income tax rate is 3.07%, applied to all gross wages with no deductions or exemptions. The rate has been flat since 2004. In addition to the state tax, every Pennsylvania municipality charges a local Earned Income Tax ranging from 0.5% to 3.75% (Philadelphia residents). Employees also pay a 0.07% state unemployment contribution on the first $10,000 of wages. Total state-level withholding for most PA workers is 4.07-4.5% depending on location.

Yes. Every Maryland county and Baltimore City charges a county income tax on the same taxable income as the state tax. County rates range from 2.25% (Cecil County) to 3.20% (Baltimore City and several large counties including Montgomery, Prince George's, and Howard). A worker in a 3.2% county at $75,000 income pays roughly 4.75% state plus 3.2% county, for a combined effective rate near 7.6% before federal.

Washington has no state income tax, so there is no state income tax withholding. However, Washington does deduct two mandatory amounts: the Paid Family and Medical Leave premium (employee pays approximately 0.529% of wages up to $176,100) and the WA Cares Fund long-term care premium (0.58% of all wages, no cap). At $75,000 salary, these two deductions total approximately $832 per year combined.

At $60,000 income, Illinois and Pennsylvania produce similar take-home pay: Illinois charges about $2,850 in state tax (4.75% effective), while Pennsylvania charges $2,449 combined state and typical local EIT. At $90,000, the gap widens slightly in Pennsylvania's favor if you live in a standard 1% EIT area: PA takes about $3,670 versus Illinois at $4,335. Philadelphia residents at any income level pay more total state+local tax than Illinois workers.

Yes, significantly so for most income levels. At $75,000, Maryland workers in a 3.2% county pay approximately $5,542 combined state and county income tax. Illinois workers at $75,000 pay approximately $3,592 in state tax with no local layer in most areas. The difference is about $1,950 per year. Maryland's higher combined rate reflects both its progressive state brackets and the mandatory county piggyback tax that all Maryland residents pay.

Written by

Hassaan Rasheed

Web Developer & Content Researcher

Hassaan builds calculators and writes research-backed guides on finance, math, payroll, and construction topics. Every number in his articles is sourced from official data and worked through by hand.

View LinkedIn Profile