California Paycheck Tax: How Much Is Deducted From Every Check (2026)

California paycheck tax breakdown: CA income tax 1%–13.3%, SDI 1.1% no cap, federal withholding, and take-home at $50K, $75K, and $100K for single filers.

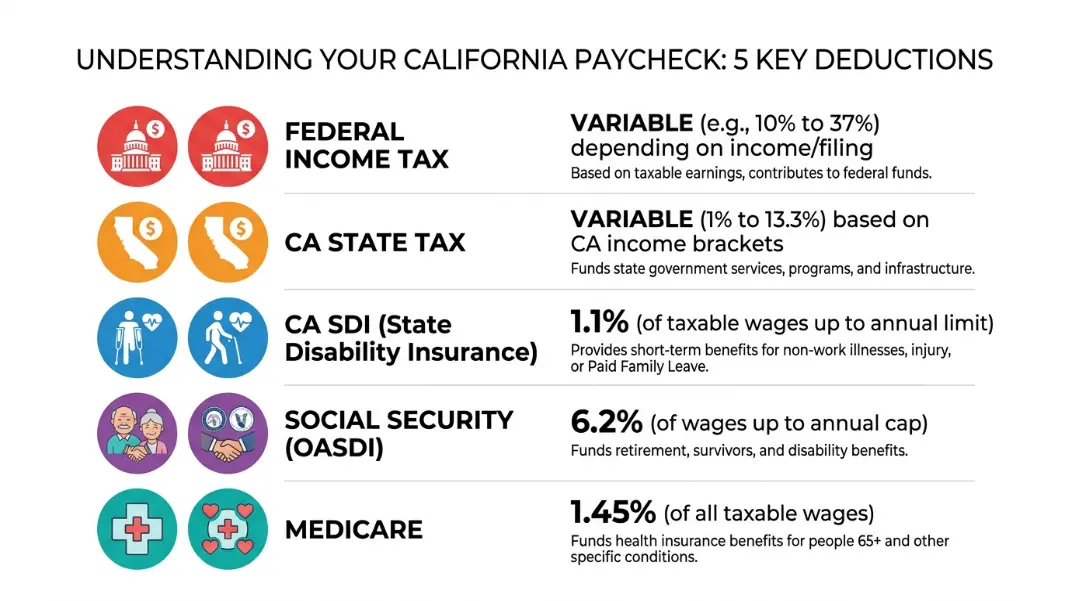

California is the highest-tax state in the country for W-2 earners above a certain income, and the gap between gross and net pay can be genuinely shocking the first time you see a pay stub. A $100,000 salary in California does not produce $8,333 per month in your bank account. After federal withholding, California state income tax, SDI, Social Security, and Medicare, you are closer to $5,900. That 29% difference between what your employer pays you and what you actually receive is not an accident or a withholding error. It is the compounded effect of five separate mandatory deductions, each governed by its own rules and rate structure.

The California Paycheck Calculator lets you run the exact numbers for your salary, filing status, and pay frequency in seconds. This guide breaks down each deduction layer in detail, explains why California's standard deduction is so much smaller than the federal one, and covers the 401(k) and HSA trap that catches many California employees off guard at tax time.

California's Five Mandatory Paycheck Deductions and What Each One Actually Costs

Every California W-2 paycheck has five lines that pull money out before you see it. Understanding what each one is and how it is calculated prevents the confusion that comes from staring at a pay stub and wondering where 30% of your salary went.

1. Federal Income Tax

Federal income tax withholding is based on your W-4 form, your filing status, and the IRS tax tables. The 2026 federal tax brackets are progressive. A single filer reaches the 22% bracket at $47,150 and the 24% bracket at $100,525. The effective federal rate for most California middle-income earners falls between 12% and 22%, depending on deductions.

2. California State Income Tax

California has the steepest top marginal income tax rate of any state at 13.3%. The state uses 10 progressive brackets starting at 1% and reaching that 13.3% rate above $1,000,000. Most Californians earning between $50,000 and $150,000 pay effective state income tax rates between 3% and 7%. The calculation section below walks through the bracket math in detail.

3. California SDI (State Disability Insurance)

SDI is a flat 1.1% of all gross wages with no annual wage cap since January 1, 2024. Every dollar you earn is subject to SDI. On a $100,000 salary, that is $1,100 per year taken as $42.31 per biweekly paycheck.

4. Social Security (OASDI)

Social Security is a federal FICA tax at 6.2% of wages up to the 2026 wage base of $176,100. Once your year-to-date earnings cross $176,100, Social Security withholding stops for the rest of the calendar year. A California employee earning $200,000 pays Social Security on only the first $176,100, for a maximum annual contribution of $10,918.

5. Medicare (HI)

Medicare is 1.45% of all wages with no cap. An additional 0.9% Additional Medicare Tax applies to wages above $200,000 for single filers. Unlike Social Security, Medicare never stops regardless of how high your wages go.

How California State Income Tax Is Calculated on Your Gross Pay

California's income tax calculation starts with a key number that surprises most people: the California standard deduction for 2026 is only $5,202 for single filers and $10,404 for married filing jointly. Compare that to the federal standard deduction of $14,600 (single) and $29,200 (married filing jointly) and the gap is obvious.

That $9,398 difference in standard deductions for a single filer means $9,398 more of your income is taxable at the California level than at the federal level. The impact compounds as income rises. This is not a quirk of the system. It is a deliberate design feature of California tax law.

California income tax brackets for single filers (2026):

| Taxable Income | Rate |

|---|---|

| $0 to $10,756 | 1% |

| $10,757 to $25,499 | 2% |

| $25,500 to $40,245 | 4% |

| $40,246 to $55,866 | 6% |

| $55,867 to $70,606 | 8% |

| $70,607 to $360,659 | 9.3% |

| $360,660 to $432,787 | 10.3% |

| $432,788 to $721,314 | 11.3% |

| $721,315 to $999,999 | 12.3% |

| $1,000,000 and above | 13.3% (includes 1% Mental Health Services Tax) |

Example: California state income tax on a $75,000 salary (single filer)

Gross income: $75,000

Less California standard deduction: -$5,202

California taxable income: $69,798

Tax at 1% on first $10,756: $107.56

Tax at 2% on $10,757-$25,499 ($14,743): $294.86

Tax at 4% on $25,500-$40,245 ($14,746): $589.84

Tax at 6% on $40,246-$55,866 ($15,621): $937.26

Tax at 8% on $55,867-$69,798 ($13,932): $1,114.56

Total California income tax: approximately $3,044

Notice how quickly the brackets stack. At $75,000, roughly the last $14,000 of California taxable income is taxed at 8%. By the time a single filer earns above $70,607, the next dollar of California taxable income immediately hits 9.3%. Most employees earning between $70,000 and $150,000 see their marginal California rate sit at 9.3% for the bulk of their income. That is the bracket doing the most work for the majority of California's professional workforce.

The federal calculation follows a different path entirely. The Federal Income Tax Rate Calculator shows how federal brackets apply after the $14,600 standard deduction, which produces a noticeably lower taxable income base than the California calculation allows.

California SDI: The 1.1% Tax With No Wage Cap Since 2024

California's State Disability Insurance program changed in a way that many employees did not notice when it happened. Senate Bill 951 (SB 951) removed the SDI taxable wage cap starting January 1, 2024. Before 2024, SDI applied only up to a wage ceiling, and once you crossed it, withholding stopped. Today, there is no ceiling.

This change has the largest impact on higher earners. A California employee making $250,000 now pays $2,750 per year in SDI. Previously, they would have paid around $1,378. The rate itself stayed at 1.1%, but applying it to all wages rather than capped wages effectively doubled the SDI cost for high earners.

SDI contribution examples at the 1.1% uncapped rate:

| Annual Gross Wages | Annual SDI | Per Biweekly Paycheck |

|---|---|---|

| $50,000 | $550 | $21.15 |

| $75,000 | $825 | $31.73 |

| $100,000 | $1,100 | $42.31 |

| $150,000 | $1,650 | $63.46 |

| $250,000 | $2,750 | $105.77 |

What does SDI provide in return? California's SDI program funds short-term disability payments when you cannot work due to a non-work-related illness or injury, and it funds Paid Family Leave (PFL) when you take time off to bond with a new child or care for a seriously ill family member. The maximum SDI benefit in 2026 is approximately 70% to 90% of your base weekly wages, depending on your income level. Lower earners get the higher replacement rate. The benefit period is up to 52 weeks for disability and up to eight weeks for PFL in California.

Unlike Social Security and Medicare, SDI is a California-only deduction. Employees who move out of California mid-year stop having SDI withheld once their employment in California ends. If you are a California employer operating a voluntary plan that the state approves as an alternative to SDI, employees contribute to the voluntary plan instead at a rate no higher than the state plan rate.

One detail that trips people up: California SDI contributions are not deductible on your federal tax return. In years when the old wage cap existed and was later eliminated, some taxpayers had taken a deduction for SDI under an earlier interpretation. Under current rules, SDI withholding is not deductible as a state income tax for federal purposes on most returns. Consult a tax preparer if you have SDI showing in Box 14 of your W-2 and you are unsure how to treat it.

Take-Home Pay at $50,000, $75,000, and $100,000 in California (2026)

The table below shows approximate annual and monthly take-home for a single filer with no pre-tax deductions (no 401k, no health insurance, no FSA) on standard biweekly payroll. Federal withholding assumes one allowance and standard W-4 settings.

| Gross Salary | Federal Tax | CA State Tax | CA SDI | Social Security | Medicare | Net Annual | Net Monthly |

|---|---|---|---|---|---|---|---|

| $50,000 | $3,781 | $1,073 | $550 | $3,100 | $725 | $40,771 | $3,398 |

| $75,000 | $8,683 | $2,986 | $825 | $4,650 | $1,088 | $56,768 | $4,731 |

| $100,000 | $14,401 | $5,507 | $1,100 | $6,200 | $1,450 | $71,342 | $5,945 |

A few observations from these numbers worth noting.

At $50,000, the total tax burden (federal plus California plus FICA) is about $9,229, or 18.5% of gross. Many people are surprised this number is not higher. The federal standard deduction of $14,600 at this income level shelters a meaningful portion of gross wages from federal tax, keeping federal liability relatively low.

At $75,000, total taxes jump to $18,232, or about 24.3% of gross. The shift from the $50K scenario to the $75K scenario is sharper than many expect because the incremental $25,000 is taxed at higher marginal rates on both the federal and California sides simultaneously.

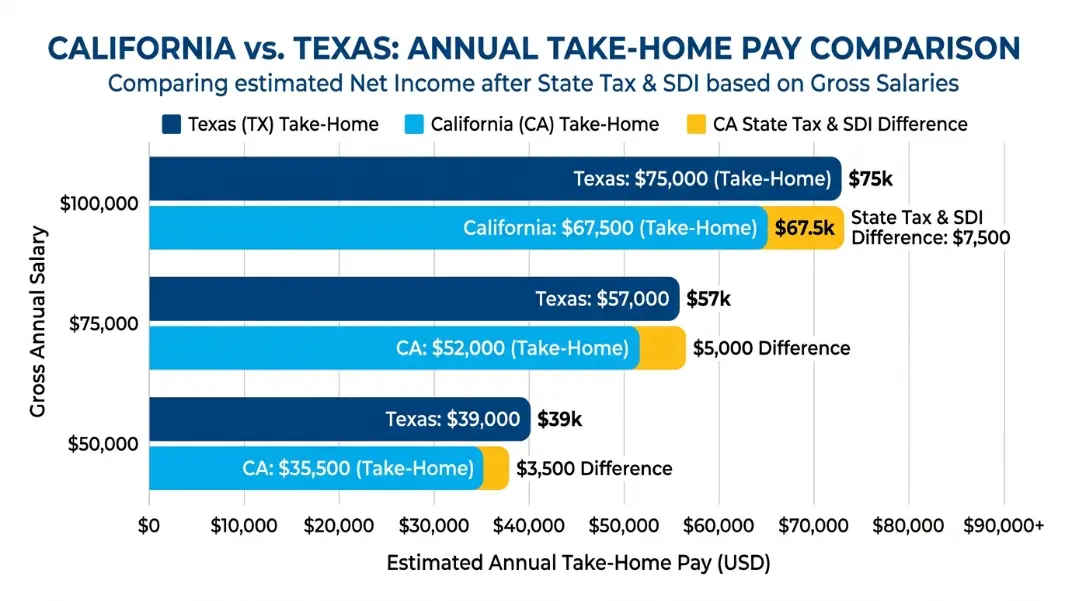

At $100,000, total taxes reach $28,658, just under 29% of gross. This is where the California income tax starts showing its teeth: $5,507 in state tax on $100,000 gross, versus zero state income tax for the same employee in Texas or Florida. The SDI cap removal also means the full $1,100 applies regardless of income.

These figures do not account for pre-tax deductions, which can meaningfully reduce both federal and California tax. The next section explains exactly what reduces your California taxes and what does not, which is one of the most misunderstood areas of California payroll.

Pre-Tax Deductions in California: What Reduces Your Taxes and What Does Not

California is different from every other state in the country on two specific pre-tax deductions: 401(k) contributions and HSA contributions. Getting this wrong does not cause paycheck problems immediately, but it creates state tax surprises at filing time.

401(k) Traditional Contributions: Federal Yes, California No

When you contribute to a traditional 401(k), your contribution reduces your federal taxable income. That is the core benefit of pre-tax retirement saving. If you earn $100,000 and contribute $10,000 to a traditional 401(k), your federal taxable income drops to $90,000, and your federal withholding decreases accordingly.

California does not recognize this deduction.

Your California taxable income remains at $100,000 regardless of how much you put into a traditional 401(k). The state of California will tax your full gross wages at the California bracket rates, as if the 401(k) contribution never happened. This is not a withholding glitch. It is written into California law. California conforms to many federal tax provisions but specifically does not conform to the pre-tax treatment of 401(k) contributions.

The practical consequence: if you contribute $20,500 to a traditional 401(k) in California, you save federal income tax on all $20,500. You save zero California income tax. When you eventually withdraw from that 401(k) in retirement, California will tax the withdrawals. If you retire in California, you pay California income tax on both your contributions (which were never deducted) and your earnings, resulting in partial double taxation. If you retire in a no-income-tax state, you escape California tax on those withdrawals entirely, which is one reason why California retirees frequently move to Nevada, Arizona, or Texas.

The Roth vs. Traditional 401(k) Calculator is particularly relevant for California employees. Because California provides no state tax deduction for traditional contributions, the traditional vs. Roth decision looks different here than it does in states that do recognize the deduction. For many California earners in the 9.3% state bracket, contributing to a Roth 401(k) makes more sense than in most other states: you pay California tax either way, so you might as well lock in after-tax status federally and pay nothing on qualified withdrawals.

HSA Contributions: Federal Yes, California No

Health Savings Accounts (HSAs) are triple-tax-advantaged at the federal level: contributions are pre-tax, growth is tax-free, and qualified withdrawals for medical expenses are tax-free. This is arguably the most powerful savings vehicle in the federal tax code for people with high-deductible health plans.

California does not recognize HSA tax-exempt status. At all.

In California, HSA contributions are not deductible from state income. HSA investment earnings are subject to California state income tax each year. Withdrawals for qualified medical expenses, which are tax-free federally, are taxable at the California level unless you can document they are for qualified medical purposes and even then the state handles the treatment differently than the federal treatment in certain cases.

This matters practically because many California employees see HSA contributions on their W-2 reflected in a way that reduces their apparent federal wages but their California wages remain at the full gross. If you are not expecting this, your California return at filing time will show more state taxable income than you anticipated.

Health Insurance Premiums: The One That Works in California

If your employer offers health insurance through an IRC Section 125 cafeteria plan, and most large employers do, your employee premium share is withheld on a pre-tax basis. This reduces both your federal taxable income and your California taxable income. Unlike 401(k) and HSA contributions, California fully recognizes cafeteria plan health insurance premium deductions.

For a California employee paying $300 per month in health insurance premiums through a Section 125 plan, that $3,600 per year is excluded from both federal and California wages. At a 9.3% California marginal rate, that saves $334.80 in California state tax. At a 22% federal rate, it saves $792. Combined, the $3,600 in premiums generates about $1,127 in tax savings, which is a 31% effective discount on the cost of coverage.

FSA Contributions: Work in California

Flexible Spending Account (FSA) contributions through a Section 125 plan also reduce both federal and California taxable income, similar to health insurance premiums. This is another area where California aligns with federal treatment. Employees contributing to a healthcare FSA or dependent care FSA through their employer's cafeteria plan get both the federal and California tax benefit.

Commuter Benefits: Partially Recognized

California recognizes the federal exclusion for employer-provided commuter benefits through payroll (transit passes and qualified parking) up to the federal monthly limits. These reduce both federal and California taxable income when provided through a qualified plan.

If you want to see your exact take-home number after entering your 401(k) contribution, health insurance premiums, and any other pre-tax elections, run the California Paycheck Calculator with your current pay stub details. The calculator applies California-specific rules for each deduction type so you are not working from approximations.

For employees who have recently left a job or are managing a separation, the California Final Paycheck Law covers the legal timing rules for when your last check must be issued, what must be included, and what happens when an employer misses the deadline.

For a single filer earning $75,000 per year with no pre-tax deductions, the combined deductions from a California paycheck in 2026 are approximately $18,232 annually: roughly $8,683 in federal income tax, $2,986 in California state income tax, $825 in SDI, $4,650 in Social Security, and $1,088 in Medicare. That leaves about $56,768 take-home per year, or $4,731 per month. The effective total tax rate at that income is around 24.3% of gross pay. The California Paycheck Calculator computes exact withholding for any salary and pay frequency.

California uses 10 progressive income tax brackets ranging from 1% at the lowest income levels to 13.3% on income above $1,000,000. The 13.3% rate includes the 1% Mental Health Services Tax that kicks in above seven figures. Most single filers earning between $70,607 and $360,659 face a 9.3% marginal California rate on the top portion of their income. The California standard deduction is only $5,202 for single filers in 2026, which means most of your gross wages are exposed to state tax from the first dollar earned above that small deduction.

California SDI (State Disability Insurance) funds short-term disability benefits and Paid Family Leave for California workers. The 2026 rate is 1.1% of all gross wages with no wage cap, following the changes from SB 951 effective January 1, 2024. On a $75,000 annual salary, SDI totals $825 per year, or about $31.73 per biweekly paycheck. Unlike states that cap this type of contribution, California now applies the 1.1% rate to every dollar earned regardless of how high wages go. SDI contributions are not deductible on your federal return.

Yes, California taxes traditional 401(k) contributions. While federal law allows you to deduct traditional 401(k) contributions from your federal taxable income, California does not conform to this treatment. Your California taxable wages include the full gross pay before any 401(k) contribution. A $10,000 traditional 401(k) contribution saves federal income tax but saves zero California state income tax. California also taxes HSA contributions and investment earnings within HSAs, making HSA accounts less tax-advantaged for California residents than for residents in conforming states.

Texas and Florida have no state income tax and no equivalent of California's SDI. A single California resident earning $100,000 pays approximately $5,507 in California state income tax and $1,100 in SDI that a Texas or Florida resident at the same gross pay does not owe. Over a career, that difference compounds significantly. At $100,000 gross, the California employee nets about $71,342 annually versus roughly $77,949 for the equivalent Texas employee, a gap of over $6,600 per year from state-level taxes alone, before any cost of living differences.

The California standard deduction for 2026 is $5,202 for single filers and $10,404 for married filing jointly. This is dramatically lower than the federal standard deduction of $14,600 (single) and $29,200 (married filing jointly). The $9,398 gap for single filers means California taxes roughly $9,400 more of your income than the federal government does before any brackets even apply. This structural difference is one of the primary reasons why California's effective state income tax rate feels higher than the published bracket rates would suggest for middle-income earners.

Written by

Hassaan Rasheed

Web Developer & Content Researcher

Hassaan builds calculators and writes research-backed guides on finance, math, payroll, and construction topics. Every number in his articles is sourced from official data and worked through by hand.

View LinkedIn Profile