Nebraska Paycheck Tax Guide: Rate Cuts, SS Exemption, and Take-Home Pay (2026)

Nebraska income tax: 4-bracket system with a top rate dropping to 3.99% by 2027. Social Security now fully exempt. Take-home at $50K, $75K, $100K.

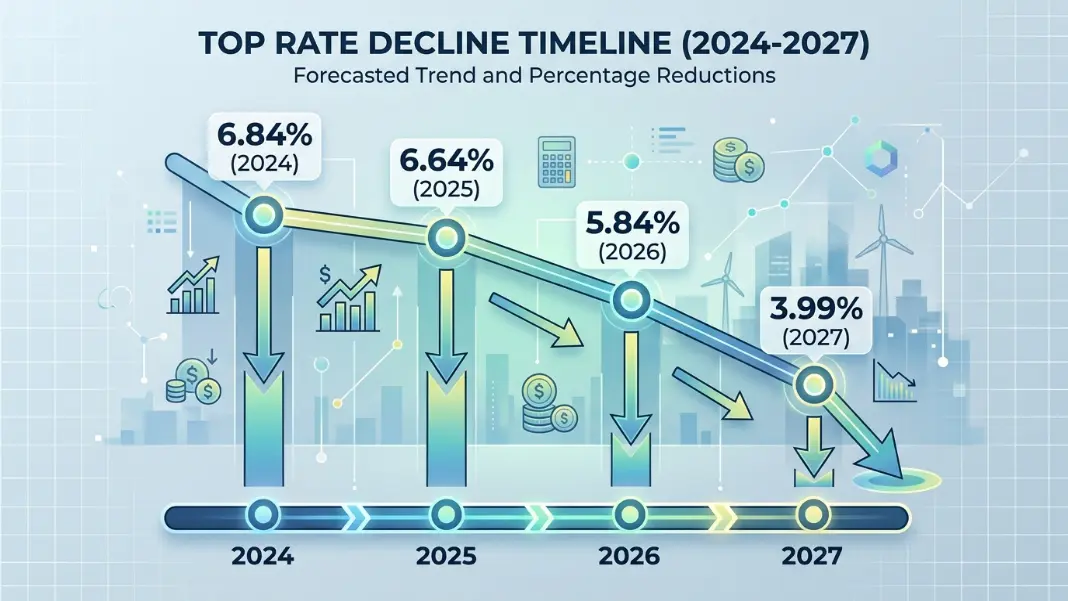

Nebraska workers are getting a tax cut every year through at least 2027, and unlike most tax relief that requires a new bill each legislative session, this one is already written into law. The top state income tax rate dropped from 6.84% in 2024 to 6.64% in 2025. It falls again to 5.84% in 2026, then targets 3.99% in 2027 if state revenue conditions are met. No annual vote, no last-minute uncertainty. The schedule was locked in under LB 754 passed in 2023.

The Nebraska Paycheck Calculator applies the current 2025 brackets and standard deduction to your salary and shows exact take-home pay per paycheck. If you are comparing a job offer or budgeting a move, this guide covers how the brackets actually work, what changed for retirement income, and how Nebraska compares to Iowa, Kansas, and Missouri.

Nebraska Income Tax Brackets for 2025: A Top Rate on Its Way Down

Nebraska uses four progressive brackets for state income tax. These rates apply to taxable income after subtracting the standard deduction: $7,900 for single filers and $15,750 for married filing jointly in 2025.

| Taxable Income (Single) | 2025 Rate |

|---|---|

| $0 to $3,700 | 2.46% |

| $3,701 to $22,170 | 3.51% |

| $22,171 to $35,730 | 5.01% |

| Over $35,730 | 6.64% |

The brackets are not especially wide at the lower end. A single filer earning $50,000 reaches the top 6.64% bracket on roughly $6,000 of income after the standard deduction. That means most of the paycheck for a middle-income earner is already in the 5.01% or 6.64% range, making the top rate more consequential than it might appear in states with wider middle brackets.

What makes Nebraska's structure different right now is the scheduled reduction. Here is where the top rate has been and where it is headed:

| Tax Year | Top Rate |

|---|---|

| 2024 | 6.84% |

| 2025 | 6.64% |

| 2026 | 5.84% (planned) |

| 2027 | 3.99% (if revenue triggers met) |

The 2027 rate is conditional on Nebraska's general fund revenues hitting specified thresholds. But the 2026 reduction to 5.84% is already scheduled. For someone earning $100,000, the drop from 6.64% to 5.84% on the top-bracket portion of income is roughly $450 in annual state tax savings. The drop to 3.99% in 2027 would be substantially larger.

Nebraska has no local income tax. No city or county adds a line to your paycheck. Omaha, Lincoln, and every other Nebraska city leave local income entirely to the state.

Social Security and Retirement Income: What Nebraska No Longer Taxes

This is the most significant recent change to Nebraska's tax code for anyone over 60, and it is not well publicized. Starting with tax year 2025, Social Security income is fully exempt from Nebraska income tax.

That was not always the case. For years, Nebraska taxed Social Security benefits above a certain threshold, which put retirees in the position of owing state income tax on federal benefits that most states do not touch. LB 873 (2022) and LB 754 (2023) phased out and then fully eliminated that taxation. As of 2025, there is no income limit, no partial inclusion, and no phase-in percentage. Social Security income is simply out of the Nebraska tax calculation.

For a retiree drawing $24,000 in Social Security and $30,000 from an IRA, this means the $24,000 in Social Security is completely off the table for state income tax purposes. Only the $30,000 IRA distribution factors into the bracket calculation after the standard deduction. That could reduce Nebraska taxable income by $24,000 compared to what it would have been two years ago.

Pension income from private sector plans and IRA distributions remain taxable as ordinary income in Nebraska. The Social Security exemption is specific to Social Security benefits and Railroad Retirement Board benefits, not all retirement income. Nebraska teachers and public employees should verify whether their specific pension type qualifies under the current exemption rules.

The Nebraska, Minnesota, Utah, and Montana Paycheck Guide has more on how Nebraska's retirement income treatment compares to neighboring states, which matters if you are choosing where to retire on a fixed income.

Federal Withholding on a Nebraska Paycheck

For most Nebraska workers, federal income tax and FICA take far more from each paycheck than Nebraska state tax does, even at the current 6.64% top rate. Federal withholding is based on your W-4 elections and the IRS graduated brackets.

2025 federal income tax brackets for single filers:

| Taxable Income | Federal Rate |

|---|---|

| Up to $11,925 | 10% |

| $11,926 to $48,475 | 12% |

| $48,476 to $103,350 | 22% |

| $103,351 to $197,300 | 24% |

| Over $197,300 | 32% |

FICA comes out before the federal bracket calculation affects your refund. Social Security tax is 6.2% on wages up to $176,100 in 2025. Medicare is 1.45% on all wages, plus an additional 0.9% surcharge on wages over $200,000.

At $75,000, a single Nebraska filer with no pre-tax deductions and a standard W-4 pays approximately:

Federal income tax: $10,294

Social Security: $75,000 × 6.2% = $4,650

Medicare: $75,000 × 1.45% = $1,088

Total FICA: $5,738

Nebraska state income tax: $3,501

Total deductions: $19,533

Nebraska state share of total: 17.9%

Federal share: 82.1%

Nebraska's state income tax accounts for less than one-fifth of the total withholding burden even at $75,000. The W-4 is the document that controls the single largest variable. Workers who have not updated their W-4 since before 2020 may want to revisit it using the IRS Tax Withholding Estimator, particularly after marriage, a new dependent, or a significant income change.

Nebraska Take-Home Pay at $50K, $75K, and $100K

The numbers below assume a single filer, no dependents, no pre-tax deductions, standard W-4 elections, and biweekly payroll. Nebraska state tax uses the 2025 brackets and $7,900 standard deduction.

State tax calculation detail:

For $50,000 (taxable income = $42,100):

$3,700 × 2.46% = $91

$18,470 × 3.51% = $648

$13,560 × 5.01% = $679

$6,370 × 6.64% = $423

Nebraska state tax: $1,841 (effective rate: 3.68%)

For $75,000 (taxable income = $67,100):

$3,700 × 2.46% = $91

$18,470 × 3.51% = $648

$13,560 × 5.01% = $679

$31,370 × 6.64% = $2,083

Nebraska state tax: $3,501 (effective rate: 4.67%)

For $100,000 (taxable income = $92,100):

$3,700 × 2.46% = $91

$18,470 × 3.51% = $648

$13,560 × 5.01% = $679

$56,370 × 6.64% = $3,743

Nebraska state tax: $5,161 (effective rate: 5.16%)

Annual take-home summary:

| Gross Salary | Federal Tax | FICA | NE State Tax | Take-Home | Effective Total Rate |

|---|---|---|---|---|---|

| $50,000 | $5,294 | $3,825 | $1,841 | $39,040 | 21.9% |

| $75,000 | $10,294 | $5,738 | $3,501 | $55,467 | 26.0% |

| $100,000 | $16,244 | $7,650 | $5,161 | $70,945 | 29.1% |

These figures will shift meaningfully once the 2026 rate reduction takes effect. At $100,000, the move from 6.64% to 5.84% on the top bracket portion shaves roughly $450 off the annual state tax bill. The potential 2027 drop to 3.99% would save several hundred more. Pre-tax 401k contributions reduce Nebraska taxable income as well as federal taxable income, giving workers an above-the-line tool to manage their effective rate right now without waiting for the legislature.

Nebraska vs Iowa, Kansas, and Missouri

Nebraska's current 6.64% top rate is not low by regional standards. But no other neighboring state is delivering a scheduled multi-year rate cut at the same pace. Here is how the states compare at the $75,000 income level:

| State | Structure | Top Rate | Effective Rate at $75K | Local Tax |

|---|---|---|---|---|

| Nebraska | Progressive, 4 brackets, scheduled reductions | 6.64% (2025), targeting 3.99% (2027) | ~4.67% | None |

| Iowa | Flat rate transitioning | 5.70% flat (2025) | ~4.2% | None |

| Kansas | Progressive | 5.58% top | ~4.5% | None |

| Missouri | Progressive | 4.95% top | ~3.9% | St. Louis and Kansas City 1% each |

Iowa moved to a 5.70% flat rate in 2025 as part of its own multi-year reduction plan, making the Iowa and Nebraska effective rates close for workers in the $50,000 to $100,000 range. Iowa's rate applies with no local income tax additions, which keeps the comparison simple.

Kansas uses a two-bracket progressive system with a 5.58% top rate on income over $30,000. The effective rate at $75,000 is around 4.5%, slightly below Nebraska's current 4.67%.

Missouri looks the most competitive on paper at $75,000 with about 3.9% effective, but that comparison requires a caveat. Missouri allows local income taxes in two cities: St. Louis and Kansas City each charge 1% on earned income. Workers in those cities pay the Missouri state rate plus the 1% local, which shifts the comparison considerably. Nebraska has no equivalent local tax exposure anywhere in the state.

The more important comparison for Nebraska workers is what happens in 2027 if the revenue triggers are met. At a 3.99% flat rate, Nebraska would be the most tax-competitive state in this group for middle-income earners, below Iowa's current trajectory and well below Kansas. Even without the 2027 reduction, the 2026 rate at 5.84% narrows the gap with Iowa substantially.

For retirement planning context, the Roth IRA Contribution Calculator can show whether pre-tax 401k deferrals make more sense than Roth contributions at your current Nebraska income level, factoring in what your bracket will likely look like after the 2026 and 2027 reductions.

Nebraska has four brackets for 2025. After subtracting the $7,900 standard deduction for single filers, the rates are: 2.46% on the first $3,700; 3.51% on income from $3,701 to $22,170; 5.01% on income from $22,171 to $35,730; and 6.64% on income above $35,730. For married filing jointly, the standard deduction is $15,750 and the bracket thresholds are wider. The top rate is scheduled to drop to 5.84% in 2026 and potentially 3.99% in 2027 under LB 754.

No. Starting with tax year 2025, Nebraska fully exempts Social Security income from state income tax. This change was phased in through LB 873 (2022) and LB 754 (2023). Before these laws, Nebraska taxed Social Security benefits above certain thresholds. The exemption applies to Social Security retirement benefits and Railroad Retirement Board benefits. IRA distributions and private pension income are still subject to Nebraska income tax as ordinary income.

A single filer earning $75,000 in Nebraska pays approximately $3,501 in annual state income tax, an effective rate of 4.67%. After subtracting the $7,900 standard deduction, taxable income is $67,100. The tax is calculated across all four brackets, with most income falling in the 5.01% and 6.64% tiers. On a biweekly paycheck, that is roughly $135 per pay period in Nebraska state withholding. The Nebraska Paycheck Calculator shows exact per-paycheck figures for any salary.

No. Nebraska does not allow cities or counties to impose a local income tax. Workers in Omaha, Lincoln, Bellevue, or any other Nebraska city pay only the state income tax rate. There is no city tax line on a Nebraska pay stub. This is a genuine advantage over Missouri, which allows Kansas City and St. Louis each to charge 1% on earned income, and over Indiana, where every county levies its own income tax rate.

Under LB 754, Nebraska's top income tax rate drops from 6.64% in 2025 to 5.84% in 2026. A further reduction to 3.99% is targeted for 2027, but that step is conditional on Nebraska's general fund revenues meeting specific thresholds set in the legislation. The 2026 reduction is already scheduled without any additional revenue conditions. The lower bracket rates are also scheduled to decrease alongside the top rate over the same period.

At $75,000, Nebraska's effective state income tax rate is approximately 4.67% and Iowa's is approximately 4.2% in 2025. Iowa moved to a 5.70% flat rate in 2025 as part of its own phased reduction plan. Neither state has a local income tax. Nebraska's advantage depends on how far the LB 754 reductions proceed: if the 2027 target of 3.99% is reached, Nebraska would be below Iowa's current rate trajectory for most income levels between $50,000 and $150,000.

Written by

Hassaan Rasheed

Web Developer & Content Researcher

Hassaan builds calculators and writes research-backed guides on finance, math, payroll, and construction topics. Every number in his articles is sourced from official data and worked through by hand.

View LinkedIn Profile